Real Interest Rates History (1960–2026): U.S. Treasury Yields vs Inflation

A monthly macroeconomic dataset tracking the inflation-adjusted cost of US government borrowing over six decades, with historical regime classification and downloadable data for research use.

US real interest rates measure the inflation-adjusted return on US government bonds — the difference between the nominal 10-Year Treasury yield and realized CPI inflation. This page provides a long-term monthly dataset from 1962 to present, with historical regime classification, statistical analysis, and downloadable data.

10Y Treasury Yield

CPI Inflation (YoY)

Real Interest Rate

- US real interest rates (10-Year Treasury yield minus CPI inflation) have fluctuated between approximately −6.4% and +9.4% over the 1962–present period — a total range of nearly 16 percentage points, according to FRED and BLS data.

- Real rates were negative in approximately 16% of all months observed since 1962 (124 out of 770), but these episodes clustered in dramatic bursts: the 1970s oil shocks and the 2020–2023 inflation surge account for the vast majority of negative observations.

- The longest continuous negative real rate episode lasted 35 months (July 2020 – May 2023), encompassing both the COVID-era monetary expansion and the post-pandemic inflation surge — the deepest trough in the dataset at −6.4%.

- The 2022–2023 tightening cycle produced the fastest transition from deeply negative to positive real rates since the Volcker disinflation of the early 1980s.

- Historically, sustained periods of negative real rates have coincided with above-average equity valuations, while sustained positive real rates above 4% have preceded significant financial stress episodes.

Monthly Obs.

Historical Max

Historical Min

Months Below 0%

Long-Run Mean

Key Facts About US Real Interest Rates

- The highest real interest rate recorded in the dataset is +9.4%, observed in August 1983 during the post-Volcker disinflation, when nominal yields remained above 11% while inflation had fallen below 2.5%.

- The lowest real interest rate recorded is −6.4%, observed in March 2022 when CPI inflation surged above 8.5% while 10-Year yields were still near 2%.

- Real interest rates were negative in roughly 16% of all months since 1962 — but 31% of those negative observations occurred in the 2020s alone.

- The longest continuous negative real rate episode lasted 35 months (July 2020 – May 2023).

- The long-run average US real interest rate is approximately +2.0%, with a median of +1.9%.

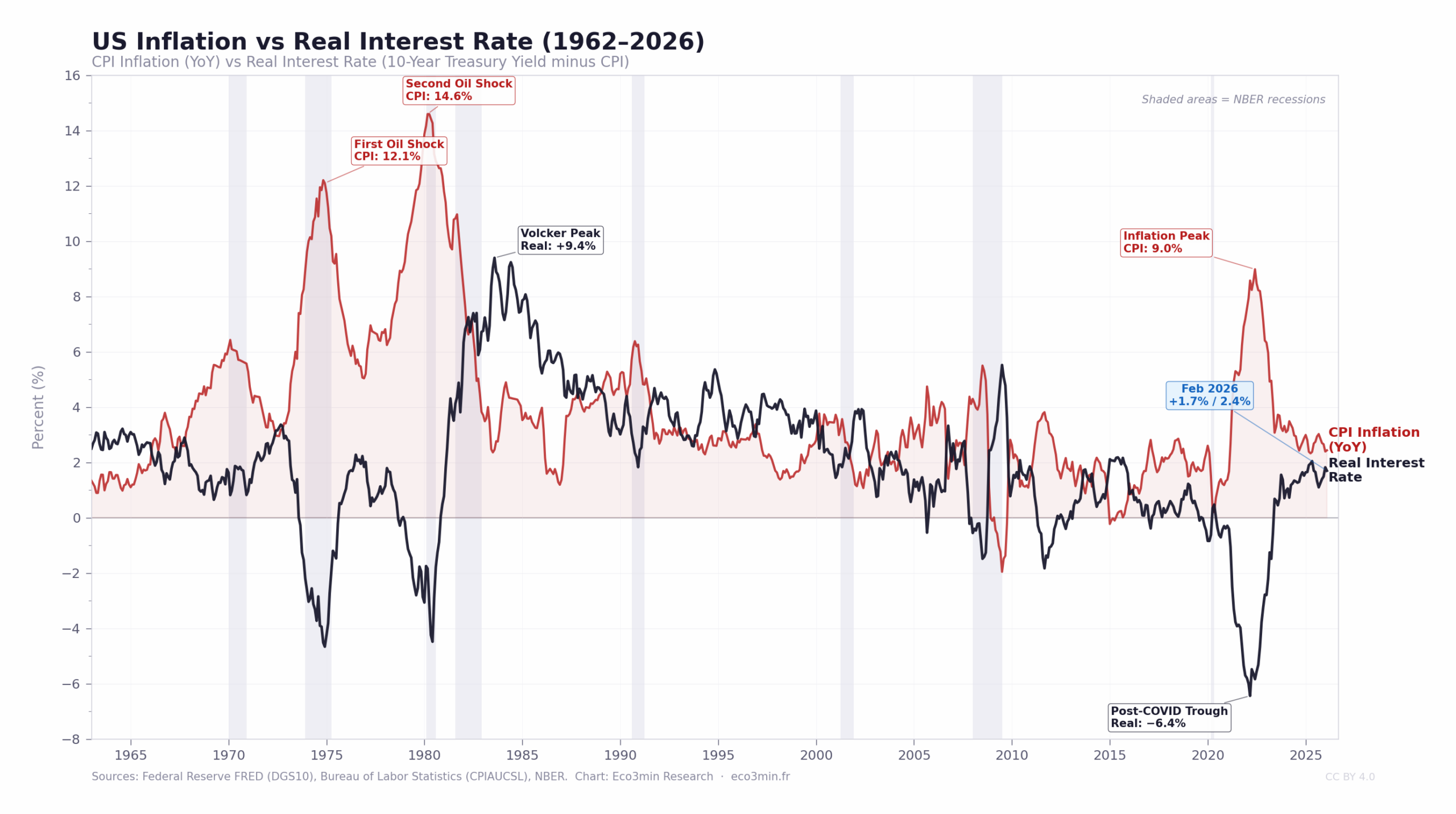

Chart: US Inflation vs Real Interest Rate

US Inflation vs Real Interest Rate — Monthly, January 1963 to February 2026

CPI Inflation (YoY) and Real Interest Rate (10-Year Treasury Yield minus CPI). Shaded areas: NBER recessions.

Every major negative real rate episode since 1962 was preceded by an inflation surge that outpaced nominal yields — visible on the chart as the red line (CPI) pulling sharply above the black line (real rate). The 2020–2022 episode produced the widest gap between the two series in the entire dataset.

Sources: Federal Reserve Bank of St. Louis (FRED, series DGS10), Bureau of Labor Statistics (CPIAUCSL), NBER recession dates. Chart: Eco3min Research.

Chart updated monthly following BLS CPI release. Latest observation: February 2026.

{kind=link}

The chart above displays the US real interest rate — defined as the 10-Year Treasury yield minus the year-over-year CPI inflation rate — from January 1962 to February 2026. The zero line separates environments where bondholders earn a positive return after inflation (above) from those where inflation erodes the purchasing power of bond holdings (below). The annotated extreme values at 1974, 1983, and 2022 mark the three most significant real rate dislocations observed in the dataset.

Macroeconomic Context: Why Real Interest Rates Matter

The real interest rate is among the most consequential variables in macroeconomic analysis. It represents the inflation-adjusted cost of borrowing — the price that an economy pays for deferring consumption or investment into the future. While nominal interest rates are set by central banks and bond markets, real rates reflect the interaction between monetary policy and the broader inflationary environment.

Real interest rates play a central role in several areas of economic analysis. In monetary policy transmission, central banks target the real rate — not the nominal rate — when attempting to influence economic activity. A 5% nominal rate in a 7% inflation environment is economically stimulative (negative real rate), while a 3% nominal rate in a 1% inflation environment is relatively restrictive (positive real rate of 2%). This distinction, formalized in the Taylor Rule framework, is fundamental to understanding policy effectiveness.

In asset valuation, real rates serve as the discount rate in present-value models. Lower real rates increase the theoretical value of long-duration assets — equities, real estate, and long-term bonds. The sharp compression of real rates between 2009 and 2021 is widely considered a structural factor behind the expansion of equity multiples during that period.

In fiscal sustainability analysis, real rates determine the dynamics of government debt accumulation. When real interest rates fall below the real growth rate of the economy (the r < g condition described in public finance literature), governments can sustain higher debt-to-GDP ratios without increasing the tax burden — a condition that prevailed through much of the 2010s in the United States.

In international capital flows, real interest rate differentials between countries drive capital allocation decisions. A rise in US real rates relative to other advanced economies tends to attract foreign capital, strengthening the dollar and tightening financial conditions in emerging markets — a transmission channel documented extensively by the Bank for International Settlements.

For a broader framework on how interest rates shape financial cycles, see our research on monetary regimes and interest rate cycles.

Research Question

This page investigates a central empirical question: how have US real interest rates evolved over the long term, and what structural regimes can be identified in the data?

Specifically, the dataset enables researchers to examine: the frequency and duration of negative versus positive real rate environments since 1962; the magnitude and speed of transitions between monetary regimes; the relationship between real rate levels and broader macroeconomic conditions; and the extent to which the 2020–2023 episode represented a historical anomaly relative to the six-decade record.

Common Research Applications

Monetary policy analysis. Researchers use the real rate series to evaluate the stance of monetary policy beyond nominal rate levels — distinguishing between periods when a given nominal rate is accommodative (during high inflation) versus restrictive (during low inflation). The regime classification facilitates comparison across policy cycles.

Asset valuation and discount rates. Real interest rates serve as the theoretically appropriate discount rate in present-value asset pricing models. Analysts use this dataset to examine the historical relationship between real yields and equity market valuations — particularly the Cyclically Adjusted Price-to-Earnings ratio (CAPE).

Debt sustainability analysis. Public finance researchers use the real rate series to assess the r − g differential (real interest rate minus real GDP growth), which determines the trajectory of government debt-to-GDP ratios over time.

Inflation regime studies. The dataset enables researchers to identify and compare distinct inflationary environments — from the 1970s commodity-driven inflation to the 2021–2022 post-pandemic price surge — through the lens of their real rate consequences.

Principal Statistical Findings

Long-term distribution

Over the full sample (1962–present), the mean US real interest rate is approximately +2.0%, with a standard deviation of roughly 2.6 percentage points. The distribution is moderately skewed, with a longer left tail reflecting episodes of deeply negative real rates during inflationary periods. The median value is approximately +1.9%, close to the mean — indicating a roughly symmetric core distribution pulled leftward by extreme negative observations during inflationary episodes.

Summary Statistics (1962–Present)

| Statistic | Value |

|---|---|

| Mean | +2.0% |

| Median | +1.9% |

| Standard Deviation | 2.6 pp |

| Minimum | −6.4% (March 2022) |

| Maximum | +9.4% (August 1983) |

| Share of months < 0% | ≈ 16% (124 / 770) |

| Share of months > 4% | ≈ 17% (133 / 770) |

| Number of observations | 770 |

Historical extremes

| Period | Real Rate | Context |

|---|---|---|

| Aug 1983 (peak) | +9.4% | Post-Volcker disinflation; nominal yields remained above 11% as CPI inflation fell below 2.5% |

| 1974–1975 | −4.7% | First oil shock; CPI inflation surged above 12% while nominal yields lagged |

| 1980 | −4.5% | Second oil crisis; inflation peak before Volcker tightening took full effect |

| 2011–2012 | −0.6% avg | Post-GFC quantitative easing; 10Y yields below 2% with moderate inflation |

| Mar 2022 (trough) | −6.4% | Post-COVID inflation surge; CPI exceeded 8.5% while 10Y yields were still near 2% |

Structural breaks

The data exhibits at least three identifiable structural breaks. The first occurred around 1981–1982, when the Volcker tightening shifted the economy from a volatile real rate environment — alternating between deep negatives during oil shocks and sharp positives during monetary contractions — to the highest sustained positive real rates of the modern era. The second occurred around 2008–2009, when the Federal Reserve’s move to near-zero nominal rates, combined with quantitative easing, compressed real rates to historically low levels. The third occurred in 2020–2022, when the pandemic-era monetary and fiscal expansion, followed by an inflation surge above 8%, produced the deepest negative real rate observed in the dataset — followed by one of the fastest normalizations on record as the Federal Reserve raised rates aggressively.

Duration of negative real rate environments

While negative real rates are not the norm — occurring in approximately 16% of all monthly observations — they cluster in intense episodes when they do appear. The longest continuous negative streak lasted 35 months (July 2020 – May 2023), followed by 24 months during the first oil shock (September 1973 – August 1975) and 22 months during the second oil shock (January 1979 – October 1980). A further 12-month continuous negative episode occurred from May 2011 to April 2012 during the post-GFC quantitative easing period. Outside these clusters, negative real rates tend to be brief and associated with specific inflation shocks.

Historical Regime Analysis

The 60-year dataset can be divided into six broad macroeconomic regimes, each characterized by distinct real rate dynamics. These regimes correspond to well-documented periods in monetary and economic history.

1962–1970 · Post-Bretton Woods Transition

Average real rate: +2.2% — Range: +0.7% to +3.4% — Zero negative months

Under the Bretton Woods fixed exchange rate system, monetary policy was constrained by the dollar-gold peg. Real rates were consistently positive and moderate — not a single month recorded a negative reading during this era. Inflation remained contained below 4% for most of the decade, and 10-Year Treasury yields fluctuated between 4% and 7%. The regime ended as inflationary pressures built in the late 1960s following expansionary fiscal policy linked to Vietnam War spending and Great Society programs. The collapse of Bretton Woods in 1971 removed the external anchor on US monetary policy.

1971–1982 · The Great Inflation

Average real rate: +0.9% — Range: −4.7% to +7.4% — 34% of months negative

This period encompasses the two oil price shocks (1973–1974 and 1979–1980), the broader failure of monetary policy to anchor inflation expectations, and the beginning of the Volcker tightening. The average real rate remained slightly positive at +0.9%, but this figure masks extraordinary volatility: real rates swung from −4.7% during the deepest oil shock episodes to +7.4% as Volcker’s aggressive rate hikes took hold while inflation began to fall. CPI inflation reached 12.1% in 1974 and peaked in 1980, while nominal yields struggled to keep pace during the inflationary phases. The Federal Reserve under Arthur Burns and G. William Miller pursued accommodative policies that were retrospectively judged insufficient to contain inflation. The appointment of Paul Volcker in August 1979 marked the turning point.

1983–1999 · Volcker Disinflation and the Great Moderation

Average real rate: +4.6% — Range: +1.8% to +9.4% — Zero negative months

The Volcker tightening produced the highest sustained real interest rates in the dataset. By raising the Federal Funds Rate to 20% in June 1981, the Federal Reserve broke inflationary expectations at the cost of two recessions (1980 and 1981–1982). As inflation fell sharply in 1982–1983, nominal yields declined more slowly, producing real rates exceeding 9% — the all-time peak of +9.4% in August 1983. Not a single month recorded a negative real rate during these 17 years. The subsequent period — often called the Great Moderation — was characterized by gradually declining nominal yields, stable inflation around 2–3%, and persistently positive real rates. This environment is widely studied as a benchmark for “normal” monetary conditions.

2000–2008 · Dot-Com Adjustment and Housing Boom

Average real rate: +1.7% — Range: −1.5% to +3.9% — 11% of months negative

The burst of the dot-com bubble in 2000 led the Federal Reserve to cut rates aggressively, briefly pushing real rates below zero. The subsequent recovery and housing boom restored positive real rates, but at lower levels than the 1990s. This period is notable for the compression of the term premium and the broad decline in global real rates — a phenomenon attributed by Federal Reserve Chair Ben Bernanke to the “global savings glut.” Real rates fluctuated in a narrower band, foreshadowing the structural decline that would accelerate after 2008. Negative real rate episodes were brief and shallow, associated with the 2001 recession and the onset of the 2008 financial crisis.

2009–2021 · Post-GFC Low Rate Environment

Average real rate: +0.5% — Range: −5.7% to +5.5% — 29% of months negative

The Global Financial Crisis of 2008 led the Federal Reserve to reduce the Federal Funds Rate to near zero and initiate large-scale asset purchases (quantitative easing). These actions compressed nominal long-term yields and produced the lowest average real rates since the 1970s. However, the picture was more nuanced than a uniformly negative environment: the average real rate remained slightly positive at +0.5%, and the period included significant positive real rate episodes — notably during the 2013–2014 taper tantrum and the 2018 tightening cycle, when real rates exceeded +5%. Negative real rate months clustered in 2011–2012 (post-QE2 period) and, most dramatically, from 2020 onward. The COVID-19 pandemic in 2020 triggered additional monetary and fiscal expansion. In 2021, as supply chain disruptions and demand surges pushed CPI inflation sharply higher, the real rate plunged deeply into negative territory.

2022–Present · Inflation Shock and Normalization

Average real rate: −0.5% — Range: −6.4% to +2.0% — 34% of months negative

This regime begins with the most extreme negative real rate in the dataset — −6.4% in March 2022, when CPI inflation exceeded 8.5% while 10-Year yields were still near 2%. Beginning in March 2022, the Federal Reserve initiated one of the most aggressive tightening cycles in its history, raising the Federal Funds Rate by 525 basis points in approximately 16 months. As nominal yields rose and inflation decelerated, real rates returned to positive territory by mid-2023. By early 2026, the 10-Year real rate had settled around +1.7%, within the “Neutral” regime band. This transition from −6.4% to positive territory represents the fastest real rate normalization since the Volcker era, and raises questions about the new equilibrium level of real rates — a debate closely linked to estimates of the neutral real rate (r-star).

Interpretation Framework

The following framework classifies real rate levels into four broad monetary environments. These categories are derived from the historical distribution of the dataset and correspond to distinct macroeconomic conditions.

Inflation significantly exceeds nominal yields. Bondholders experience substantial real losses. Historically associated with inflationary shocks (1970s) or crisis-era monetary expansion (2020–2022). These conditions tend to favor real assets and equities over fixed income.

Mildly negative real rates typically reflect deliberate central bank policy aimed at stimulating economic activity. Common during easing cycles and post-recession recoveries. This environment supports credit expansion and risk-taking.

Positive real rates consistent with stable growth and anchored inflation expectations. This range encompasses the long-run mean of the dataset (+2.0%) and is generally associated with the most balanced macroeconomic outcomes.

High positive real rates indicate tight monetary conditions. Historically concentrated in the post-Volcker era (1983–1999), when real rates averaged +4.6%. Sustained readings above 4% have preceded significant financial stress, credit contractions, or recessions.

Methodology

Real interest rates are calculated as the difference between the nominal yield on the 10-Year US Treasury constant maturity bond and the trailing twelve-month rate of change in the Consumer Price Index for All Urban Consumers (CPI-U).

The nominal yield series (DGS10) is sourced from the Federal Reserve Bank of St. Louis FRED database. The consumer price index series (CPIAUCSL) is published by the Bureau of Labor Statistics. Both series are resampled to end-of-month frequency to ensure temporal alignment.

This measure uses ex-post real rates — meaning realized inflation rather than expected inflation. The alternative approach — ex-ante real rates using inflation expectations or TIPS breakeven spreads — is conceptually different and produces a distinct series. TIPS-based measures are only available from January 2003 in the United States. The ex-post approach is used here because it provides the longest consistent historical series and reflects the actual purchasing power outcome for bondholders.

Regime Classification Logic

Monthly observations are classified into five regimes based on the real rate value:

| Real Rate Range | Regime Label |

|---|---|

| Below −2% | Financial Repression |

| −2% to 0% | Accommodative |

| 0% to +2% | Neutral |

| +2% to +4% | Restrictive |

| Above +4% | Shock / Crisis Tightening |

Dataset Design

| Variable | Description | Unit | Source |

|---|---|---|---|

| date | End-of-month observation date | YYYY-MM | — |

| nominal_yield_10y | 10-Year Treasury Constant Maturity Rate | Percent | FRED (DGS10) |

| cpi_index | Consumer Price Index for All Urban Consumers | Index (1982–84=100) | BLS (CPIAUCSL) |

| cpi_yoy | Year-over-year percentage change in CPI-U | Percent | Calculated |

| real_rate | Nominal 10Y yield minus CPI YoY inflation | Percent | Calculated |

| regime | Monetary environment classification | Categorical | Eco3min classification |

Dataset Sample

| date | nominal_yield_10y | cpi_yoy | real_rate | regime |

|---|---|---|---|---|

| 1974-12 | 7.43 | 12.10 | −4.67 | Financial Repression |

| 1984-06 | 13.56 | 4.33 | +9.23 | Shock |

| 2000-01 | 6.66 | 2.79 | +3.87 | Restrictive |

| 2012-06 | 1.62 | 1.65 | −0.03 | Accommodative |

| 2022-06 | 3.14 | 8.98 | −5.84 | Financial Repression |

| 2026-02 | 4.13 | 2.43 | +1.70 | Neutral |

Eco3min Macro Data Hub

— inflation, yield curves, equity returns, credit spreads and global indicators.

Dataset Download & Reproducibility

The complete dataset is provided in open formats for quantitative analysis and academic research. It is updated monthly following the release of the Bureau of Labor Statistics CPI report.

Python Reproduction Code (via FRED API)

The following script reproduces the complete dataset using publicly available data from the Federal Reserve FRED database. Researchers can verify all values independently.

import pandas as pd

import pandas_datareader.data as web

# Fetch source series from FRED

df = web.DataReader(

['DGS10', 'CPIAUCSL'],

'fred',

'1962-01-01'

).resample('M').last()

# Compute year-over-year CPI inflation

df['cpi_yoy'] = df['CPIAUCSL'].pct_change(12) * 100

# Calculate real interest rate

df['real_rate'] = df['DGS10'] - df['cpi_yoy']

# Regime classification

def classify_regime(r):

if r < -2: return "Financial Repression"

if r < 0: return "Accommodative"

if r < 2: return "Neutral"

if r < 4: return "Restrictive"

return "Shock"

df['regime'] = df['real_rate'].apply(classify_regime)

# Export

df.to_csv("us-real-interest-rates-1962-present.csv")Update Schedule

Data Sources

- Primary

Federal Reserve Bank of St. Louis (FRED) — 10-Year Treasury Constant Maturity Rate (series: DGS10). Monthly average, percent per annum. - Primary

Bureau of Labor Statistics (BLS) — Consumer Price Index for All Urban Consumers (series: CPIAUCSL). Monthly, seasonally adjusted, base period 1982–84=100. - Reference

Robert Shiller / Yale University — Cyclically Adjusted Price-to-Earnings Ratio (CAPE). Used for cross-reference in valuation analysis. - Reference

Federal Reserve Board — TIPS yields (series: DFII10) for comparison with market-implied real rates (available from January 2003).

Methodological Limitations

- Ex-post vs. ex-ante measurement. This dataset uses realized CPI inflation to compute real rates. Market participants make decisions based on expected inflation, which may diverge significantly from realized inflation. The ex-post measure captures actual purchasing power outcomes but does not reflect decision-relevant information available at the time.

- CPI measurement changes. The Bureau of Labor Statistics has modified the CPI calculation methodology multiple times since 1962, including changes to the treatment of housing costs (owner’s equivalent rent was introduced in 1983) and hedonic quality adjustments. These methodological changes affect the comparability of inflation rates across the full time series.

- Yield maturity choice. The 10-Year Treasury yield is used as the nominal rate benchmark. Alternative maturity choices (2-Year, 5-Year, or 30-Year) would produce different real rate series with distinct cyclical properties. The 10-Year maturity is selected as the most commonly referenced long-term benchmark in macroeconomic analysis.

- Term premium component. The nominal 10-Year yield includes a term premium — compensation for the risk of holding longer-duration bonds. Changes in the term premium over time (notably its compression during quantitative easing periods) affect the real rate series independently of inflation dynamics.

- CPI data revisions. Monthly CPI releases are subject to seasonal adjustment revisions. While these revisions are typically small, they may produce minor differences between the values in this dataset and values computed from subsequently revised CPI data.

- Single-country scope. This dataset covers the United States only. Cross-country real rate comparisons require adjusting for differences in inflation measurement, bond market structure, and yield curve composition.

Source : Eco3min Research (2026) —

Dataset sur les taux d’intérêt réels américains (1962–présent).

Voir le dataset.

Licence CC BY 4.0 — réutilisation autorisée avec attribution.

Related Eco3min Research Datasets