Commodity Regimes: Physical Constraints, Energy Transition, and Global Economic Cycles

This infographic synthesizes three successive regimes — the Chinese industrial supercycle, a phase of overcapacity and underinvestment, then the return of physical and geopolitical constraints — as well as their transmission channels to inflation, the industrial cycle and terms of trade.

Geological, energy and logistics constraints — the physical determinants that shape economic cycles, inflation and geopolitical balances.

— Commodities do not follow markets. They impose the constraints to which markets ultimately submit.

Commodities are not assets like the others. They are physical constraints — geological, energy, climatic, logistical — that impose themselves on the economic system and which neither central banks, financial markets nor fiscal policy can escape. When European natural gas multiplies by 17 in eighteen months (TTF 20 → 340 €/MWh, ICE, 2021–2022), that is not a “market move” — it is the brutal realization of an energy dependency that decades of industrial policy had not corrected. When copper inventories fall to the equivalent of a few hours of global consumption (15,000 tonnes, LME, end-2023), that is not a technical signal — it is a warning that the energy transition is colliding with the inertia of mining capacity.

To understand the economic mechanisms linking resources, inflation and economic cycles, see our investing for beginners hub.

The question that structures this pillar is not “where will commodity prices go?” — it is: what do commodity markets tell us about the physical constraints facing the real economy, the stage of the investment cycle, and the geopolitical power relations that shape access to resources?

This pillar constitutes the analytical framework dedicated to commodities within the Eco3min architecture. It does not duplicate the Markets pillar, which treats price formation across asset classes, nor the Macroeconomics & geopolitics pillar, which treats macro regimes. Here the object is specific: irreducible physical constraints — supply, demand, stocks, production costs, geographic concentration — and their transmission to economic cycles, inflation and geopolitical balances. The sub-pillars — Price formation, Cycles & macro transmission, Resource geo-economics — develop this framework.

The structural tension: slow physical constraints, fast financial trade-offs

The market for a commodity is the meeting point of two fundamentally different logics. The physical logic evolves on long time horizons — developing a copper deposit takes 10–15 years (S&P Global Market Intelligence), building an LNG terminal requires 4–7 years and $10–15 billion (IEA), oil investment cycles run 5–10 years (Rystad Energy). The financial logic evolves in real time — net speculative positions on WTI swing between +200,000 and +500,000 contracts (CFTC), open interest on commodity futures exceeds $3.5 trillion (BRI, 2023), commodity ETFs have net inflows of over $100 billion since 2020 (Bloomberg).

This asymmetry of time horizons produces sometimes-persistent gaps between market prices and physical reality — and it is inside these gaps that the most important signals hide. When price reflects financial expectations but physical reality does not follow (an expected surplus that does not materialize, an anticipated demand that never comes), the correction is usually violent. March 2022: Brent hits $140 on the geopolitical shock of the Russian invasion (ICE) while physical supply fell by only 1 Mb/d — the price reflected a financial risk premium, not a proportional physical deficit. August 2022: TTF touches €340/MWh (ICE) while European storage was already refilling — the price reflected supply panic, not the state of actual flows. The Price formation sub-pillar formalizes this mechanism in depth, and the reference article Physical supply vs financial demand provides the fundamental analysis.

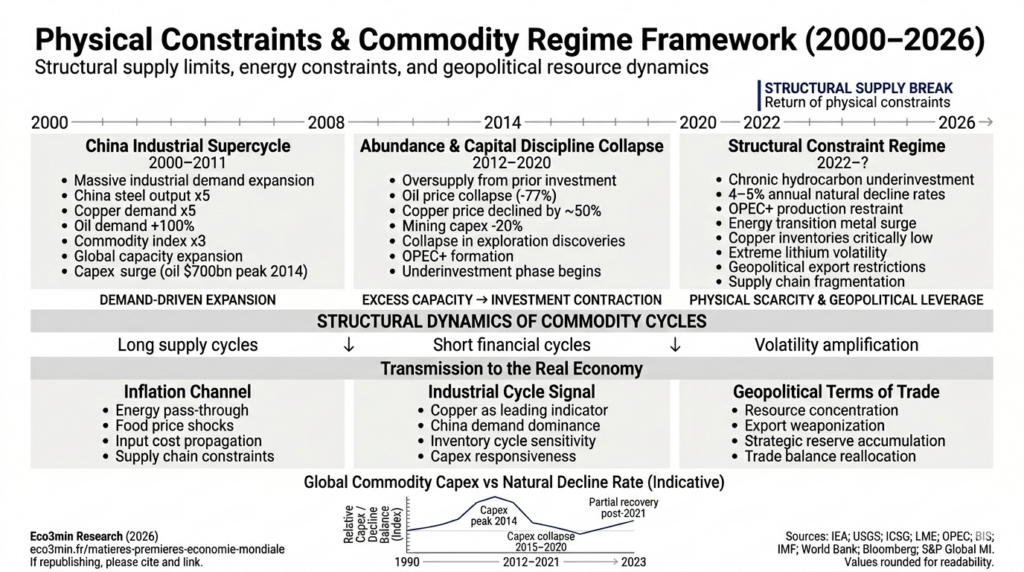

2000–2011: the Chinese industrial supercycle

The last major commodity supercycle was triggered by the largest wave of industrialization in human history. Between 2000 and 2015 China consumed more cement than the United States did during the entire 20th century (USGS). Its copper demand quintupled (ICSG), its oil demand more than doubled (IEA), and its steel production multiplied by five to reach 50% of global output (World Steel Association). The Bloomberg Commodity Index tripled between 2001 and 2008.

This supercycle produced a massive investment boom in production capacity. Global investments in oil exploration & production reached $700 billion per year at the 2014 peak (IEA). Global mining investment exceeded $200 billion per year between 2011 and 2013 (S&P Global MI). New capacities — US shale oil, Canadian oil sands, copper mines in Peru and Mongolia, lithium mines in Australia — entered production between 2012 and 2018, creating a structural supply surplus that weighed on prices for almost a decade.

2012–2020: the abundance regime — overinvestment and the destruction of discipline

The down cycle of 2012–2020 resulted directly from the overinvestment of the prior decade. Brent fell from $115 in June 2014 to $27 in January 2016 (ICE) — a 77% drop — due to the rise of US shale (US production from 5 to 13 Mb/d between 2008 and 2019, EIA), slowing Chinese demand and an OPEC market share war. Copper fell from $10,000/ton in 2011 to $4,300 in 2016 (LME). Iron ore fell from $190 to $40/ton (Platts).

This low-price regime produced two structural consequences for the current regime. First, the collapse in investment: oil E&P spending was halved between 2014 and 2020 ($700 → $370bn, IEA), mining investment fell by 30% (S&P Global MI), and the number of large copper discoveries dropped from 5–10 per year in the 2000s to 1–2 per year since 2015 (S&P Global MI). Second, the concentration of supply: marginal producers were eliminated, M&A consolidated the majors, and market power concentrated — OPEC+ emerged in 2016 to collectively manage oil supply.

Covid was the inflection point. The demand collapse in 2020 (oil -9 Mb/d, IEA; copper -2%, ICSG) destroyed remaining surpluses and drained inventories. WTI briefly went negative in April 2020 (-$37.63, NYMEX) — an unprecedented event reflecting a non-storable physical surplus. Paradoxically, this final destruction set the conditions for the subsequent reversal.

2021–?: the new regime — the return of physical constraints

The regime emerging since 2021 is characterized by the return of supply constraints as the dominant force in commodity markets — after a decade where demand and finance dominated. Three structural forces converge to create this regime shift.

Chronic underinvestment in hydrocarbons

Investment in oil exploration & production remains around $500 billion per year at end-2024 (IEA, World Energy Investment) — ~30% below the 2014 peak — a level insufficient to offset the natural decline of existing fields (4–5%/yr, IEA). The number of new conventional projects sanctioned has remained ~40% below the 2010–2014 average (Rystad Energy). US shale, which acted as a “swing producer” between 2014 and 2019, is maturing — rigs fell from 627 (peak 2022) to ~480 at end-2024 (Baker Hughes) and new-well productivity is declining as sweet spots deplete (EIA Drilling Productivity Report).

OPEC+ maintains cumulative production cuts of 5.86 Mb/d (OPEC+, 2024) — the highest level of restriction since the alliance formed. Saudi Arabia produces ~9 Mb/d, ~3.5 Mb/d below nominal capacity. This discipline creates a price floor but also a buffer — if an offer shock occurs (Libyan outage, escalation in the Middle East), the spare capacity is the only significant global shock absorber. Field analyses are developed in the Resource Geo-economics sub-pillar.

The energy transition: an explosion in metals demand

The energy transition does not reduce dependence on raw materials — it shifts it from hydrocarbons to metals. An electric vehicle requires six times more copper than an internal-combustion vehicle (IEA). An offshore wind turbine requires 8 tonnes of copper (Copper Alliance). Lithium demand is expected to multiply by 7 by 2040 (IEA, Critical Minerals Market Review). The IEA estimates a cumulative investment shortfall of $360 billion by 2030 in critical minerals.

The copper signal is structural. Global LME inventories fell to critical levels — 15,000 tonnes at end-2023 (LME), the equivalent of a few hours of global consumption, versus a 200,000–400,000 tonne average in the prior decade. Copper exceeded $11,000/ton in May 2024 (LME), a record. The pipeline of new mining projects — 10–15 years from discovery to first production — is insufficient to meet anticipated demand. Lithium price moves illustrate the violence of adjustments in these narrow markets: $15,000/ton end-2020 → $80,000/ton end-2022 → $12,000/ton end-2024 (Benchmark Mineral Intelligence) — 500% volatility in four years.

Geopolitical fragmentation: resources as instruments of power

The geographic concentration of production and refining creates unprecedented strategic levers. China controls 60% of rare earths production, 70% of cobalt refining, 80% of graphite processing (USGS/IEA). The Congo produces 70% of world cobalt (USGS). Australia and Chile produce 70% of lithium (USGS). Russia produces 40% of world palladium and supplied 40% of European gas before 2022 (Johnson Matthey, Eurostat).

The use of these resources as geopolitical levers is underway. China restricted exports of gallium and germanium (August 2023), graphite (December 2023) and antimony (August 2024, MOFCOM) — materials critical for semiconductors, batteries and defense. Consumer countries respond with diversification strategies (US Critical Minerals Act, EU Critical Raw Materials Act) — but building alternative capacity takes decades, not years. The Russian invasion of Ukraine demonstrated in real time the consequences of uncorrected energy dependence: the cost to Europe exceeded €200 billion in 2022 (Bruegel), and German industrial production has not returned to its pre-2022 level (Destatis).

Three transmission channels to the real economy

Commodities affect the real economy through three distinct channels, whose understanding is essential to interpret the signals they deliver.

Channel 1: inflation — the most direct vector

Channel 2: the industrial cycle — commodities as a leading indicator

Copper is called “Dr. Copper” because its movements tend to anticipate inflections in global industrial production with an empirical lag of 3–6 months (IMF Working Paper, 2019). China consumes 55% of global copper, 50% of steel and 50% of coal (USGS, IEA, World Steel Association) — when China slows, industrial commodities send a global deceleration signal before GDP statistics. This signal was accurate in 2015 (Chinese slowdown: copper -25%, Brent -50%) and mid-2022 (Chinese property tightening: iron ore -30%). Gold, by contrast, is a barometer of confidence in the monetary system — its rise from +$1,060 in 2015 to >$2,400 in 2024 (LBMA) reflects a progressive re-pricing of monetary fragmentation risk, amplified by record central bank purchases (1,037 tonnes in 2023, 1,045 tonnes in 2024, WGC).

Channel 3: competitiveness and terms of trade

Commodities determine the terms of trade between producing and consuming countries — and therefore relative competitiveness. Europe’s €200 billion energy penalty in 2022 (Bruegel) constituted a massive wealth transfer to energy producers (Norway, Qatar, United States). Indonesia banned raw nickel ore exports in 2020 to force domestic refining — and its share of global nickel refining rose from 6% to 40% in five years (USGS). The United States, now a net exporter of oil and LNG, has a structural advantage that Europe and China (net importers) lack — an advantage that translates into industrial competitiveness gaps documented in the Macroeconomics & geopolitics pillar.

Analyzing commodity prices as isolated signals. Oil, gas, copper and critical minerals form an interconnected system: energy conditions extraction costs for metals (aluminum is a “bar of electricity”), metals condition the capacity for an energy transition, and the transition redefines energy demand. The relevant signal is not the price of a single commodity but the overall configuration — stocks, forward curve, investment, geographic concentration and geopolitical power relations.

Three regime signals to monitor

Beyond spot prices, three structural indicators provide a more reliable regime diagnosis than any single commodity’s spot level.

The structure of the forward curve. When inventories are abundant the market is in contango (futures > spot). When inventories are tight the market moves into backwardation (spot > futures). Brent has been in near-continuous backwardation since mid-2021 (ICE), signaling a structurally tight physical market despite absolute price fluctuations. Copper experienced episodes of extreme backwardation in 2024, with spot premia exceeding $100/ton (LME). The forward curve is a better indicator of the physical market’s true state than the spot price.

The investment / decline ratio. The natural decline rate of existing oil fields (4–5%/yr, IEA) requires continuous replacement of ~4–5 Mb/d each year. For metals, ore grade depletion increases marginal cost cycle after cycle. When investment does not cover decline, deficit is inevitable — the only question is timing. The investment/decline ratio is the most reliable signal for price direction over a 3–5 year horizon.

Central bank purchases (gold). 1,037 tonnes in 2023 and 1,045 tonnes in 2024 — historical records (WGC). Major buyers (China, Poland, Turkey, India) signal via these purchases a systemic re-assessment of monetary risk and a progressive dedollarization of reserves. This structural signal transcends the gold price and informs confidence in the international monetary architecture.

Commodities are not financial assets — they are irreducible physical constraints that impose themselves on the economic system. Their cyclicality stems from the structural asymmetry between supply, which evolves over decades (geology, investment, infrastructure), and demand, which evolves over quarters (cycles, monetary policy, geopolitics). Three forces converge to define the current regime: chronic underinvestment in hydrocarbons creating a programmed supply shortfall, an energy transition that shifts dependence from fossil fuels to metals with insufficient mining capacity, and geopolitical fragmentation that turns resources into instruments of power. The relevant question is not “where will prices go?” but “what do stocks, the forward curve, the investment/decline ratio and geographic concentration tell us about the true state of the physical constraints facing the global economy?” That is the question this pillar and its sub-pillars seek to answer.

Commodities are the primary channel through which supply shocks transmit to inflation. Each $10/barrel rise in Brent adds ~0.2–0.4 percentage points to headline inflation in importing countries over 6–12 months (ECB, Economic Bulletin). The energy component alone explained 3–4 percentage points of inflation at the 2022 peak (Eurostat, BLS). Agricultural commodities produce politically sensitive food inflation — the 2008 food riots (FAO) and the 2011 North Africa instability were directly linked to cereal price spikes. Wheat jumped 60% after the invasion of Ukraine (CBOT), with Russia and Ukraine accounting for ~30% of global exports (FAO). Cocoa prices tripled in 2024 to exceed $10,000/ton (ICE) due to drought in Côte d’Ivoire and Ghana (70% of world production, ICCO). The ECB estimates that supply-chain fragmentation and energy constraints add 1–2 percentage points of structural inflation per year (Economic Bulletin, 2023). The analysis Commodities, inflation and monetary policy shows how these supply shocks translate into monetary-policy trade-offs and real-rate adjustments. This channel is analyzed in detail in the Cycles & macro transmission sub-pillar and in the Monetary policy & rates pillar.

e