The Credit Cycle: The Hidden Driver of Economic Fluctuations and Market Dynamics

Why credit is the primary causal variable behind economic fluctuations — and why activity indicators only measure its delayed consequences.

Economic turning points do not show up first in the indicators people watch most closely. Neither GDP, nor inflation, nor even unemployment signals the inflection ahead. These series measure outcomes, not causes. The leading signal lies upstream, in a quieter but decisive dynamic: credit.

The expansion and contraction of bank lending shape economic agents’ ability to invest, consume, and take risk. This mechanism works cumulatively, often several quarters before the first signs of slowdown appear in official statistics. A reading focused only on growth or inflation therefore tends to confuse symptoms with causes. Understanding the credit cycle makes it possible to place the economy and markets back into a coherent causal framework.

A mechanism that comes before visible symptoms

This analytical framework is especially relevant in the current context. After several quarters of policy rates held at elevated levels by the Federal Reserve and the European Central Bank, financing conditions have tightened without activity having fully reacted yet. This time lag between monetary tightening and the actual slowdown illustrates the logic of the credit cycle precisely: the effects do not appear immediately, but spread through a recognizable sequence.

Recent bank surveys confirm this tightening. According to the ECB’s Bank Lending Survey (January 2025), euro area banks continued to tighten lending standards for corporate loans in the fourth quarter of 2024, with a net 7% of institutions reporting a tightening. In the United States, the Federal Reserve’s Senior Loan Officer Opinion Survey (January 2025) shows a similar trend: moderate to modest net shares of banks tightened standards on commercial and industrial loans.

The credit cycle is read through volumes, lending standards, and balance sheet structure — not through policy rates alone or published activity indicators.

Credit as the initial impulse

Credit creation does more than accompany economic activity. It comes first and makes that activity possible. When a bank grants a loan, it simultaneously creates a deposit in the borrower’s account: this is the mechanism of endogenous money creation. That capacity allows economic agents to spend beyond current income, invest before having accumulated the necessary savings, or consume by bringing future resources forward.

This process generates an impulse that spreads throughout the economy. Business investment rises, durable goods demand increases, and asset prices appreciate. According to the BIS’s long-run series on credit to the non-financial private sector, the credit-to-GDP ratio in advanced economies (the United States, euro area, Japan, the United Kingdom, Canada, Australia, Switzerland, and the Nordic countries) increased from about 165% in Q1 2010 to nearly 180% by the end of 2021. That expansion preceded and supported the recovery that followed the 2008 financial crisis.

The credit cycle thus works as an amplifier of expectations. In expansionary phases, optimism translates into stronger demand for financing, validated by banks whose balance sheets improve and whose appetite for risk increases. In contractionary phases, the mechanism reverses — often with a brutality that past observations make possible to anticipate, but that consensus regularly underestimates. This dynamic is particularly visible in housing markets, where credit conditions directly drive price formation — as detailed in why real estate prices rise and fall.

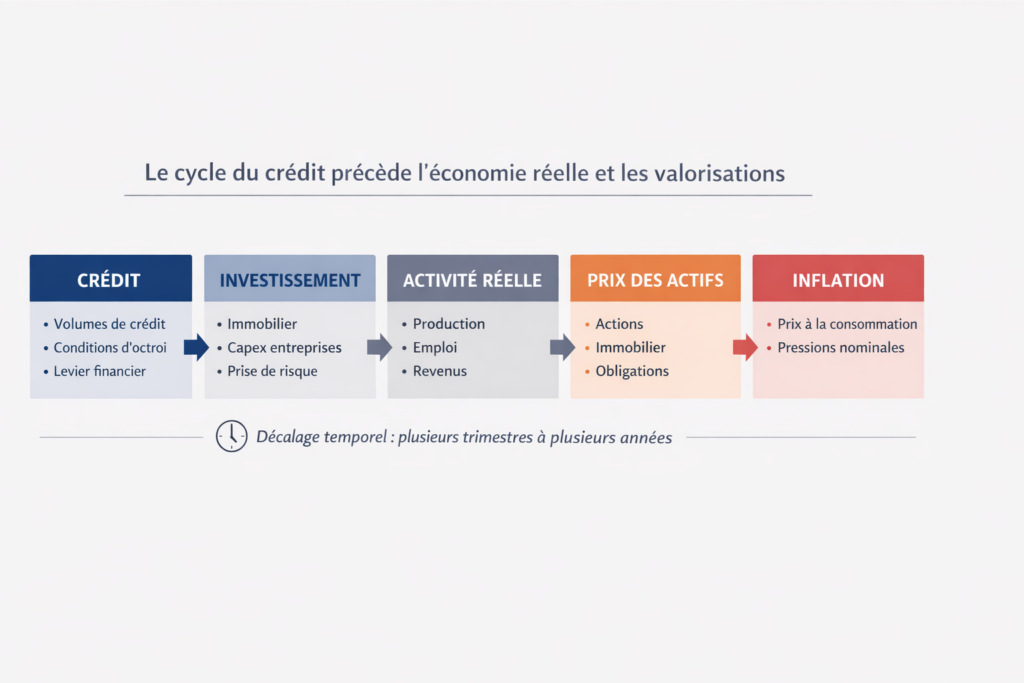

The causal sequence: from financing to prices

Credit does not passively react to economic activity. It conditions that activity through an identifiable four-step sequence. Lending standards change first: bank eligibility criteria, spreads over benchmark rates, and collateral requirements. Financing flows then evolve, affecting productive, real estate, or financial investment with a lag of several quarters. Real activity reacts in a third stage, before asset prices absorb these dynamics — sometimes with delay, sometimes through excessive anticipation.

This sequence explains why traditional cyclical indicators — GDP, inflation, unemployment — appear to be lagging variables. They measure consequences, not causes. The leading signal sits in the credit dynamic itself: in changes in bank lending surveys on credit conditions (Bank Lending Survey from the ECB, Senior Loan Officer Survey from the Fed), in the volume of new loans, and in portfolio quality as measured by non-performing loan ratios.

Interpreting GDP growth as a sign of economic strength without checking whether that growth rests on a sustainable credit expansion or on excessive debt. The distinction between nominal momentum and real value creation is essential to any reliable forecast.

Why consensus underestimates the lag

A large share of mainstream macro forecasts rests on the assumption of a rapid and linear transmission of monetary policy. Standard models expect a policy rate hike to slow activity within 12 to 18 months — an estimate that goes back to Milton Friedman’s 1960s work on “long and variable lags.” That range remains a reference point for central banks today: Atlanta Fed President Raphael Bostic said in November 2022 that it could take “18 months to two years or more” for monetary tightening to materially affect inflation, while Governor Christopher Waller estimated in January 2023 that the lag could be shorter, around 9 to 12 months.

That historical average, however, hides a more complex reality in which transmission speed varies widely across economic structures. The true lag depends on several factors: household and corporate balance sheet structure, the maturity of outstanding debt, the share of fixed-rate versus variable-rate borrowing, and banks’ ability to absorb shocks without sharply restricting credit supply. In the euro area, where fixed-rate mortgages dominate, the effect of tightening takes longer to show up than in the United States, where variable rates and mortgage refinancing transmit policy changes more quickly.

This asymmetry creates a risk of misreading the situation: the economy may appear resilient while financing conditions are already deteriorating beneath the surface. The reversal looks abrupt when it arrives, but it is actually the end point of a process that began much earlier. Understanding how banks amplify the credit cycle sheds light on this procyclical dynamic and its potentially destabilizing effects.

The role of leverage in valuation transmission

Financial and real estate asset prices reflect more than expected future income. They also reflect — and sometimes primarily reflect — investors’ ability to borrow in order to buy those assets. The link between credit and valuation runs through financial leverage, which amplifies exposure to risky assets when financing is abundant and cheap.

Between March 2020 and the end of 2021, central bank balance sheets expanded at an unprecedented pace. According to Federal Reserve data, total assets rose from $4.2 trillion in January 2020 to about $8.9 trillion at their peak in early 2022 — an increase of nearly $4.7 trillion. For the Eurosystem, the consolidated balance sheet increased from €4.671 trillion at the end of 2019 to €8.566 trillion at the end of 2021, according to the ECB’s annual financial statements — an expansion of nearly €3.9 trillion, driven by the pandemic emergency purchase programme (PEPP) and the asset purchase programme (APP).

This massive liquidity injection coincided with a strong rise in equity markets and residential real estate across most advanced economies. The contraction that began in 2022, with quantitative tightening and rising rates, partially reversed those dynamics. By early 2026, the Fed’s balance sheet had fallen back to around $6.5–6.9 trillion, while the Eurosystem’s stood close to €6.3 trillion — a reminder that valuations depend as much on financing conditions as on fundamentals.

The limits of a strictly monetary reading

Focusing only on policy rates means overlooking the quantitative dimension of credit. A low rate does not guarantee lending expansion if banks simultaneously tighten their lending standards — as happened after 2008 in several advanced economies. Conversely, high rates can coexist with still-supportive credit supply if bank balance sheets remain strong and demand for financing holds up.

The economic cycle therefore cannot be read through rates alone. Credit dynamics — volumes, portfolio quality, and sectoral distribution — provide a more reliable measure of the real impulse being transmitted to the economy. It is in these data, often less discussed than central bank decisions, that the leading signals of future turning points are found.

The credit cycle is the primary causal variable behind economic fluctuations. Activity indicators — GDP, employment, inflation — only measure its delayed consequences. A rigorous macro analysis begins with financing flows, not with their effects.

Mis à jour : 31 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.