Crypto Assets and Monetary Regimes: A Macro-Financial Framework

Crypto assets do not evolve in a parallel universe detached from the global financial system. Their valuation is driven by the same determinants as other asset classes: real rates, liquidity conditions, and the prevailing monetary regime. This analytical framework breaks with the dominant technological narrative.

How Macro-Financial Conditions Govern Crypto-Asset Valuation

Crypto assets are not a technology asset — they are a monetary asset whose price reflects the liquidity regime and the cost of capital.

Crypto assets obey the same macro-financial laws as all risky assets: their valuation depends on the cost of capital, the abundance or scarcity of liquidity, and shifts in monetary regimes. This framework — grounded in real rates, financial conditions, and liquidity cycles — explains crypto price movements more reliably than technological adoption narratives or usage curves.

Understanding this macro dependency changes how the asset class is interpreted: crypto cycles are not autonomous phenomena but amplifiers of global liquidity cycles. For allocators and analysts, positioning crypto assets within their monetary regime is a prerequisite for any serious trajectory assessment. This article analyzes the mechanisms through which macro-financial conditions determine crypto-asset valuation and their implications in the current cycle.

What markets still struggle to fully integrate is that crypto assets do not constitute an asset class independent of the global financial system. Bitcoin emerged in 2009, at the height of the global financial crisis. Its growth unfolded entirely within an unprecedented monetary environment: for more than a decade, policy real rates remained at or below zero across advanced economies — conditions documented in long-run series from the Fed, the ECB, and the BIS. These exceptional conditions mechanically favored assets without current yield, whose value rests on expectations of future capital gains. Crypto assets embody this logic: they offer programmed scarcity in a world flooded with liquidity — a value proposition whose attractiveness is directly proportional to liquidity abundance and inversely proportional to the cost of capital.

This framework aligns with the macroeconomic analysis of the role of real rates, the variable that governs all financial valuations, and fits within the broader framework of crypto assets and their economic and financial implications.

- Crypto assets react to real rates and liquidity conditions, not technological adoption cycles

- Their volatility is structural: absence of fundamental anchors + dependence on marginal flows + price reflexivity

- Institutionalization normalizes the asset class without insulating it from macro-financial cycles

Crypto assets are not a technology asset — they are a monetary asset whose price reflects the liquidity regime and the cost of capital. Their valuation is determined by three macro-financial variables: the level of real rates (which sets the opportunity cost of holding a non-yielding asset), global liquidity conditions (which drive flows toward the riskiest segments), and the degree of institutional integration (which reshapes correlations with the traditional financial system). The 2022–2023 episode provided a full-scale demonstration of this mechanism: policy-rate hikes of several hundred basis points triggered a 70% collapse in Bitcoin purely through the cost-of-capital channel. This framework is documented in BIS research on global liquidity and risky assets; the open question concerns the persistence of positive real-rate regimes and their structural impact on crypto assets’ role within diversified portfolios.

The Core Mechanism: How Monetary Regimes Drive Crypto Cycles

The relationship between macro-financial conditions and crypto-asset valuation follows an identifiable causal chain whose central mechanism is the opportunity cost of liquidity.

Shift in real-rate regime → Adjustment in opportunity cost (holding a non-yielding asset vs positive real-yield bonds) → Reallocation of liquidity flows (toward or away from speculative segments) → Amplification via reflexivity and leverage → Crypto cycle (expansion or contraction)

Crypto cycles amplify global liquidity cycles — they are not autonomous phenomena.

Trigger: real rates as opportunity cost. The fundamental determinant of crypto-asset valuation is the real rate — the return investors can earn on risk-free assets after inflation. Under negative real-rate regimes (2010–2021), the opportunity cost of holding non-yielding assets is zero or negative: capital invested in sovereign bonds loses value in real terms. In this configuration, speculative assets — of which crypto assets are the archetype — become relatively attractive. Under positive real-rate regimes (since 2022), the calculus reverses: a 10-year Treasury offering a 2% real yield (FRED data, DFII10 series, late 2025) represents an alternative that did not exist during the previous decade. A BIS working paper (Carstens, 2022, “Digital currencies and the future of the monetary system”) formalizes this logic by showing that crypto assets behave like infinite-duration assets — extremely sensitive to discount-rate shifts, of which the real rate is the structural component.

Transmission channel: global liquidity conditions. Real rates are not the sole driver of valuation; they operate through global liquidity channels. When central banks ease (QE, low rates), excess liquidity gradually permeates all market segments, from the safest (sovereign bonds) to the riskiest (growth equities, venture capital, crypto assets). This “risk-trickle-down” process is documented by the BIS (Annual Report 2024) and the IMF (Global Financial Stability Report, October 2025), showing that flows into crypto assets are positively correlated with global liquidity conditions (measured via aggregate central bank balance sheets) with coefficients of 0.6–0.7 over 2017–2025. Bitcoin in particular functions as a liquidity-cycle barometer — its behavior reflects global financial conditions far more than usage dynamics or technological innovation.

Amplifier: reflexivity, leverage, and conditional liquidity. Crypto assets exhibit pronounced reflexivity that amplifies macro-driven moves. Price changes attract or repel capital, reinforcing the initial movement — a self-sustaining momentum mechanism documented in academic literature (Bianchi, 2020, “Cryptocurrencies as an Asset Class?”, Working Paper). Extensive use of derivatives and collateralization mechanisms (crypto lending, staking, yield farming) intensifies this dynamic: implicit leverage in crypto markets reaches levels that traditional finance would not tolerate without regulatory safeguards. Coinglass data (late 2025) show the ratio of crypto derivatives open interest to spot market capitalization regularly reaches 15–20% — a leverage level that mechanically amplifies corrections when liquidity tightens. Ecosystem-specific mechanisms — such as airdrops, token distributions aimed at boosting adoption — amplify erratic flows by generating sudden speculative inflows followed by large sell-offs.

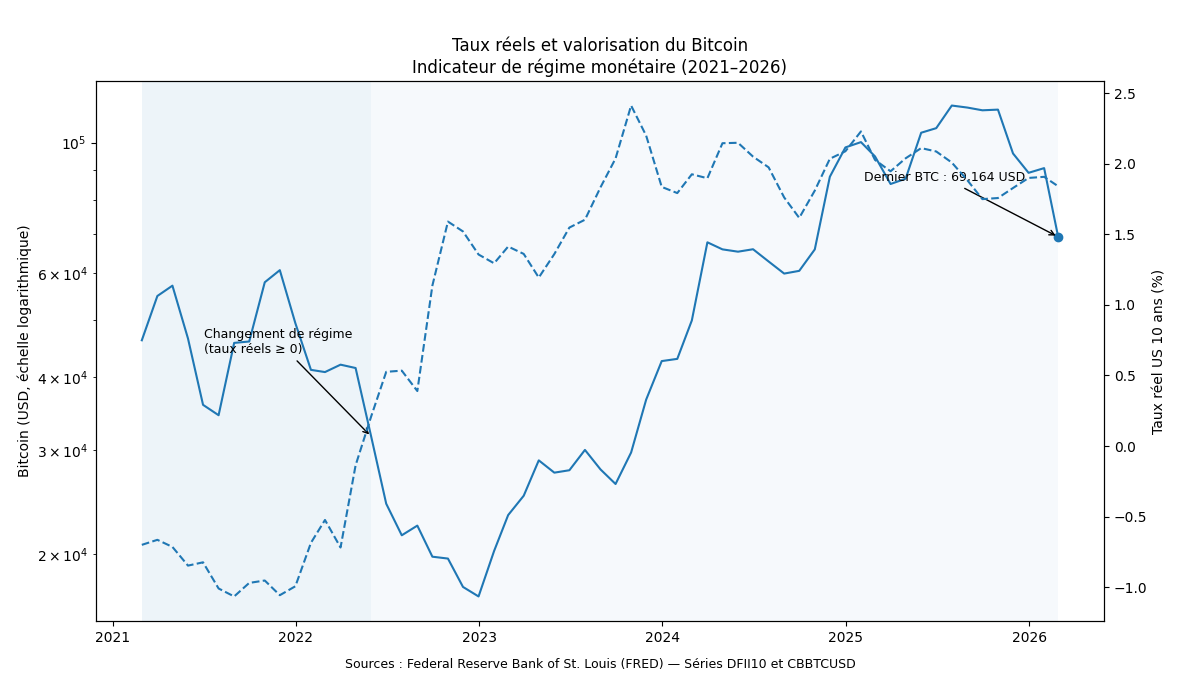

Consequence: extreme-amplitude cycles synchronized with monetary regimes. The combination of these channels produces cycles unmatched among traditional asset classes. Bitcoin fell 77% between November 2021 and November 2022, then gained more than 300% between late 2022 and late 2024. These swings are not anomalies — they are the mechanical consequence of an infinite-duration, non-yielding asset valued on expectations of future liquidity, amplified by structural leverage and strong reflexivity. The chart below illustrates the relationship between Bitcoin and the U.S. 10-year real yield — the structural variable of crypto cycles.

- Bitcoin -77%: between Nov 2021 and Nov 2022, synchronized with real rates turning positive. Source: CoinGecko, FRED.

- Crypto / global liquidity correlation: 0.6–0.7 (central bank balance sheets), 2017–2025. Source: BIS, IMF GFSR.

- US 10Y real rate: ~2% late 2025 (vs negative in 2012–2021). Source: FRED (DFII10).

- Implicit leverage: derivatives open interest / spot market cap ratio of 15–20%. Source: Coinglass, late 2025.

- Institutionalization: US spot Bitcoin ETFs accumulated > $30bn in net inflows in 2024. Source: Bloomberg, market data.

Persistently positive real rates + constrained global liquidity + high implicit leverage → crypto assets remain structurally vulnerable to liquidity-contraction phases despite ongoing institutionalization. The rate regime is the dominant variable.

- US 10Y real rates ↑ → structural downside pressure on crypto assets (opportunity cost ↑)

- Central bank balance sheets ↑ → global liquidity expansion → flows into speculative assets

- Accommodative financial conditions (FCI ↓) → risk appetite ↑ → support for crypto valuations

- Crypto derivatives leverage ↑ → higher vulnerability to corrections and cascade liquidations

- Correlation with Nasdaq ↑ → higher financial integration ↑ → lower diversification during stress

What the Consensus Gets Right — and the Macro Dependence It Underestimates

The dominant crypto-market narrative, promoted by ecosystem participants and increasingly echoed by financial consensus, centers on institutionalization: the entry of institutional investors (U.S. spot Bitcoin ETFs, crypto desks at major banks, pension fund allocations) stabilizes the asset class, reduces volatility, and grants it legitimacy comparable to other market segments. The argument relies on real evidence: U.S. spot Bitcoin ETFs accumulated more than $30 billion in net inflows in 2024 (Bloomberg data), and correlations with traditional assets have strengthened.

Its limitation lies in conflating normalization with independence. Institutionalization mechanically brings crypto assets closer to other market segments — increasing correlations with equities and bonds while eroding extreme inefficiencies that previously generated outsized returns. But it does not insulate crypto assets from their fundamental dependence on liquidity cycles and real-rate regimes. A non-yielding asset valued on expected capital gains remains structurally sensitive to opportunity cost — whether held by retail traders or pension funds. Institutionalization reduces microstructural excesses (manipulation, extreme illiquidity) without altering the fundamental macro-financial mechanism.

The consensus is therefore correct to highlight asset-class maturation but confuses maturation with emancipation. Financial normalization of crypto assets is a fact; emancipation from monetary regimes remains a hypothesis not supported by data. Rising correlations with growth equities (Nasdaq) and global financial conditions (Goldman Sachs FCI) confirm the opposite: the more crypto assets integrate into the financial system, the more they reflect its dynamics — including its vulnerabilities.

Analyzing crypto assets as a technological innovation independent of the financial cycle. Their valuation is driven by the same variables as other non-yielding assets: real rates, liquidity conditions, and risk appetite. The technological narrative (blockchain, decentralization, adoption) is the storyline — not the mechanism. Another mistake: interpreting institutionalization as a decoupling factor. Data show the opposite: the more crypto assets integrate into the financial system, the more their correlations with traditional assets increase — reducing their diversification value precisely when it would be most useful (during stress periods).

| “Autonomous Technology Asset” View | Monetary Regime View | |

|---|---|---|

| Primary determinant | Technological adoption, usage, innovation | Real rates, global liquidity, opportunity cost |

| Crypto cycle | Autonomous (halving, adoption, regulation) | Amplifier of the global liquidity cycle |

| Volatility | Declining with maturation | Structural (no yield + leverage + reflexivity) |

| Institutionalization | Stabilization and independence factor | Normalization and integration factor (correlations ↑) |

| Key variable | Number of wallets, hashrate, regulation | Real rates, central bank balance sheets, FCI, Nasdaq correlation |

Hybrid Nature, Reflexivity, and Financial Integration: Three Dimensions That Complicate the Analysis

Neither currency nor productive asset: an instrument with extreme convexity. In strict monetary-theory terms, crypto assets do not qualify as money: they only imperfectly fulfill the functions of medium of exchange, unit of account, and store of value. Nor can they be treated as productive assets generating recurring cash flows. Their profile aligns more closely with high-convexity financial instruments — assets whose sensitivity to market conditions is extreme and asymmetric. A BIS working paper (Auer & Tercero-Lucas, 2022) classifies Bitcoin as a “pure speculation premium” asset whose value is entirely derived from expectations of future liquidity and opportunity cost — without anchoring to fundamental cash flows. This characteristic explains the magnitude of reactions to monetary-regime shifts: an infinite-duration asset is mechanically more sensitive to discount-rate changes than any other financial asset.

Reflexivity as a structural amplifier. Crypto markets exhibit pronounced reflexivity in the Soros sense: prices do not passively reflect fundamentals — they create them. Rising prices attract capital (FOMO), which pushes prices higher, which attracts more capital. Conversely, declines trigger leveraged liquidations, which push prices lower, which trigger further liquidations. This self-reinforcing mechanism is amplified by ecosystem-specific collateral structures (crypto-backed lending, DeFi protocols with implicit leverage). Coinglass data show that long-position liquidations during the May 2022 crash reached $8 billion within 48 hours — a leverage cascade whose scale exceeded what fundamentals alone would justify. This reflexivity makes crypto assets the market segment most sensitive to liquidity-regime reversals.

Financial integration as a double-edged sword. Institutionalization transforms the nature of crypto markets without altering their macro dependence. On the positive side, it reduces episodes of extreme illiquidity, mitigates market manipulation, and provides regulated vehicles (ETFs) that improve access and transparency. On the risk side, it creates new contagion channels between the traditional financial system and the crypto ecosystem. If a $30 billion spot Bitcoin ETF faces massive redemptions during stress, outflows transmit directly to the underlying market — a mechanism comparable to that documented in the analysis of the passive investing revolution for traditional ETFs. Integration does not shield assets from the cycle — it connects them more tightly to it.

Implications for Interpreting the Current Cycle

Positioning within the rate regime. A monetary-regime framework implies that crypto-asset trajectories are structurally conditioned by the path of real rates. As long as real rates remain durably positive (around 1.5–2% on the US 10-year, FRED data), the opportunity cost of holding non-yielding assets remains high — a structural headwind for crypto valuations regardless of adoption or institutionalization narratives. Any future monetary easing (rate cuts, renewed QE) would be the most powerful catalyst for a new bull cycle — not a technological breakthrough or ecosystem-specific event (halving, favorable regulation). The framework of real rates and financial conditions underpins this interpretation.

Asset allocation. Institutionalization changes the role of crypto assets in diversified portfolios — but not in the way consensus suggests. Rising correlation with the Nasdaq and financial conditions reduces diversification benefits precisely as institutional investors incorporate the asset class for that purpose. During stress periods (when diversification is most needed), crypto assets tend to correlate with risky assets rather than diversify them. Their portfolio value lies more in convexity (extreme upside potential if real rates return to negative territory or in the event of sovereign confidence crises) than in permanent decorrelation. The framework of market expectation dynamics clarifies when this convexity materializes.

Financial stability. The expansion of crypto ETFs, regulated derivatives, and institutional custody services creates contagion channels between the crypto ecosystem and the traditional financial system that did not exist in the previous cycle. A 50% Bitcoin collapse in 2026 would have balance-sheet ramifications for regulated institutions that the comparable 2022 shock did not — a shift identified by the BIS (Annual Report 2024) as an emerging risk factor. The interaction with the issue of the disconnect between financial costs and systemic costs reinforces this assessment.

Invalidation conditions. This analytical framework loses relevance if crypto assets develop large-scale stabilized monetary use (common means of payment, unit of account in international trade) that provides a fundamental anchor independent of rate regimes — a scenario conceivable over the very long term but not materialized to date. It would also be invalidated by an unexpected favorable liquidity shock (faster-than-expected monetary easing, massive QE) restoring conditions similar to the 2010–2020 decade, or by regulatory changes transforming crypto assets into yield-generating instruments (regulated staking producing dividend-like cash flows). Conversely, prolonged tightening of financial conditions, fragmentation of the international regulatory framework, or a confidence crisis involving a systemic ecosystem player would amplify crypto-asset vulnerabilities in the current cycle.

Three Time Horizons for Reading Crypto Cycles

Short term (0–6 months): the trajectory of rate expectations (Fed forward guidance, market pricing) is the dominant factor. Key indicators to monitor: 10-year real rates (FRED, DFII10), global liquidity conditions (central bank balance sheets), crypto derivatives positioning (open interest, funding rates on Coinglass), and spot Bitcoin ETF flows (Bloomberg). The short-term risk is a sharp deleveraging episode if a hawkish surprise forces a repricing of rate expectations in a context of elevated implicit leverage.

Cycle horizon (1–3 years): the structural question concerns the path of real rates. If real rates converge toward zero (recession scenario or renewed QE), conditions resembling the 2020–2021 bull cycle would partially return — catalyzing a new expansion phase. If real rates remain around 1.5–2%, crypto assets will operate in a regime structurally different from the previous decade — more moderate returns, persistently high volatility, valuations constrained by opportunity cost. Interaction with the real economic cycle will determine which scenario materializes.

Structural horizon (5+ years): crypto assets constitute a full-scale laboratory of native monetary-asset behavior under regime shifts. Two structural paths are open: either crypto assets fully normalize (becoming another speculative segment correlated with financial conditions, with high volatility but no distinct properties), or they develop sufficient monetary or store-of-value use to gain partial fundamental anchoring. The latter path would likely require a major crisis of confidence in sovereign monetary systems — an extreme but not impossible scenario over this horizon. Ongoing monitoring via the weekly macro dashboard incorporates liquidity and rate conditions relevant to diagnosing the crypto regime.

Crypto assets are not a technology asset — they are a monetary asset whose valuation reflects the liquidity regime and the cost of capital. Their trajectory is determined by real rates (opportunity cost), global liquidity conditions (flows into risky assets), and the market’s structural reflexivity (leverage, momentum, cascade liquidations). Institutionalization normalizes the asset class but does not insulate it from macro-financial cycles — it connects it more tightly. The technology narrative is the storyline; the monetary regime is the mechanism. Data from the 2020–2025 cycles validate this distinction unambiguously: every major crypto turning point coincided with a real-rate regime shift, not with ecosystem-specific events.

Robust: The correlation between crypto assets and global liquidity conditions (0.6–0.7) is documented over 2017–2025. The opportunity-cost mechanism (real rates vs non-yielding assets) is a core financial-theory principle confirmed by the 2022–2023 episode. Crypto-market reflexivity and leverage effects are observable in liquidation and open-interest data. Growing institutionalization and rising correlations with traditional assets are measurable facts.

Uncertain: The duration of the positive real-rate regime is inherently unpredictable — it depends on inflation trajectories and monetary-policy decisions. Crypto assets’ capacity to develop a fundamental anchor (monetary usage, store-of-value status) remains speculative at this stage. The exact impact of institutionalization on future volatility is debated — current-cycle data show reduced average volatility but not reduced tail risk. The possibility of a sovereign-confidence shock repositioning crypto assets as safe havens is an extreme, non-quantifiable scenario.

Analyzing crypto assets through their monetary regime — rather than through the technological narrative — provides a more robust analytical framework for understanding past cycles, assessing current positioning, and identifying catalysts for the next phase. The mechanism is the same as for any non-yielding asset class: liquidity and the cost of capital drive trajectory, narrative follows.

- Crypto assets are not an autonomous technology asset — they are a monetary asset whose valuation reflects the liquidity regime and cost of capital. Crypto cycles amplify global liquidity cycles.

- The fundamental driver is the real rate: under negative-rate regimes (2010–2021), crypto thrives; under positive-rate regimes (since 2022), opportunity cost structurally constrains valuation.

- Volatility is structural, not temporary: it results from lack of fundamental anchoring, price reflexivity, and high implicit leverage (15–20% derivatives open interest / spot market cap).

- Institutionalization normalizes the asset class without insulating it from macro-financial cycles — it increases correlations with traditional assets and creates new contagion channels.

- This framework is invalidated if crypto assets achieve stabilized monetary use (fundamental anchor), if real rates return toward zero restoring 2010–2021 conditions, or if regulated staking generates dividend-like yield.

Frequently Asked Questions on Crypto Assets and Financial Cycles

Why does Bitcoin fall when rates rise?

Bitcoin generates no current income (no dividend, no coupon). Its value relies entirely on expectations of future capital gains. When real rates rise, the opportunity cost of holding a non-yielding asset increases — a Treasury yielding 2% real offers an alternative that did not exist in 2020. This mechanism, identical to that affecting long-duration growth equities, explains the negative correlation between Bitcoin and real rates observed since 2022.

Does institutionalization make crypto assets less volatile?

Institutionalization reduces average volatility (fewer episodes of extreme illiquidity, improved market depth) but does not reduce volatility during stress periods. Data from the 2022–2025 cycle show that sharp correction phases remain just as pronounced — because the fundamental mechanism (lack of anchor, leverage, reflexivity) is not altered by holder identity. Institutionalization even adds a contagion channel: spot ETFs transmit redemption flows directly to the underlying market.

Do crypto assets diversify a portfolio?

In theory, a decorrelated asset improves a portfolio’s risk/return profile. In practice, crypto assets tend to correlate strongly with risky assets (Nasdaq, financial conditions) precisely during stress periods — when diversification is most needed. Their portfolio value lies more in convexity (extreme upside potential under regime shifts) than in permanent decorrelation.

Does Bitcoin halving determine crypto cycles?

Halving (the ~4-year reduction in mining rewards) is often presented as the driver of crypto cycles. Historical data show halvings coincided with bull phases — but those phases also coincided with accommodative liquidity regimes (2012, 2016, 2020). The 2022–2024 sequence is more informative: the 2024 halving occurred under a positive real-rate regime, and its price impact was significantly weaker than in previous cycles. Halving is a supply factor (reducing new Bitcoin issuance), but the demand regime (liquidity, rates, risk appetite) overwhelmingly dominates price formation.

Mis à jour : 20 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.