Central Banks and Monetary Policy: Institutions, Rate Cycles, and Market Transmission

Every statement from the Fed, the ECB, or the BoJ is an exercise in precision communication. Beyond rate announcements, it is the nuances of language, economic projections, and tonal shifts that reveal the anticipated trajectory. The Fed’s famous “dot plot,” committee minutes, and seemingly mundane speeches by governors are all pieces of a puzzle that markets assemble in real time. But monetary policy does not steer the economy — it attempts to correct excesses with delay, imperfect tools, and models calibrated on a past that never repeats itself exactly.

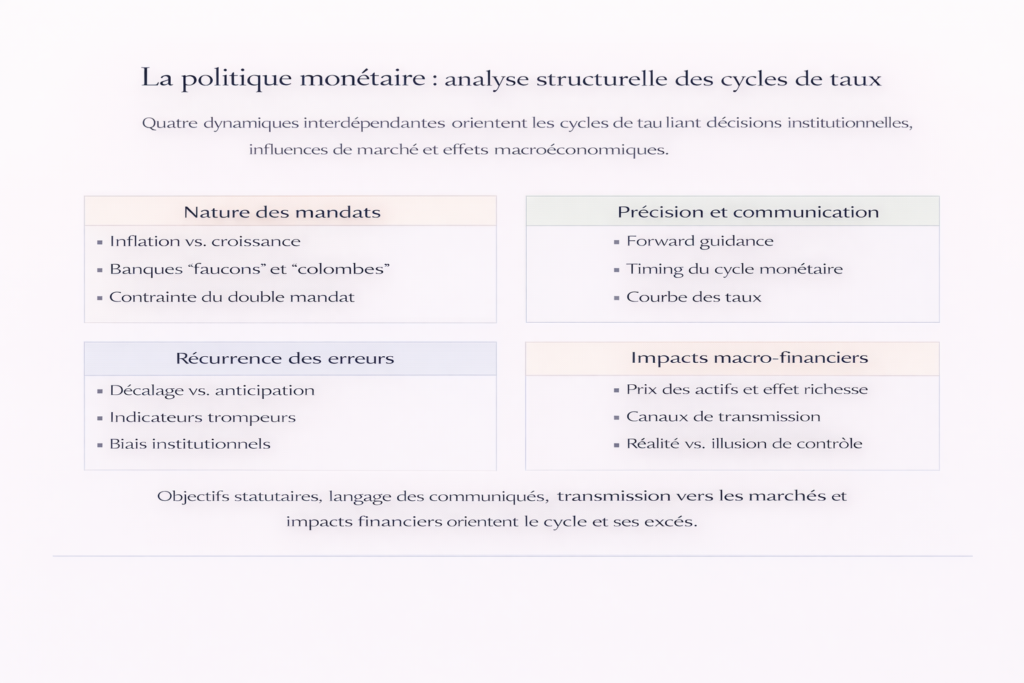

This page provides a structured analysis of how central banks operate as architects of monetary policy. The objective is not to predict the next rate decision, but to understand the institutional logic, constraints, and biases that guide these institutions in their trade-offs — and to anticipate their mistakes as much as their successes.

What is the role of central banks?

Central banks are responsible for defining and implementing monetary policy with the aim of stabilizing prices, supporting economic activity, and preserving financial stability. Their decisions operate with lags — generally estimated between 12 and 24 months for peak impact on inflation (Friedman, 1961; confirmed by estimates from the San Francisco Fed) — through interest rates, liquidity conditions, and expectations. This intrinsic latency makes their actions structurally imperfect and prone to calibration errors.

Several quarters typically pass between a rate decision and its observable effects on investment, employment, or inflation. The precise mechanisms of this diffusion — banking channels, expectations, housing, financial conditions — are detailed in our analysis dedicated to the transmission lags of monetary policy.

How Eco3min analyzes monetary policy

Analyses published on Eco3min approach monetary policy as an institutional process subject to constraints, biases, and transmission lags. The objective is not to comment on each rate decision, but to understand which monetary regime we are operating in — and how that regime interacts with the economic cycle and the prevailing inflation regime. This page provides the analytical framework linking analyses dedicated to central banks, expectations, and rate cycles.

For a dedicated analysis of recurring biases, diagnostic errors, and structural limits to central bank action, see: Recurring central bank errors.

Three monetary regimes since 1990

Monetary policy does not fluctuate randomly from one meeting to another. It is organized into durable regimes defined by a combination of rate levels, dominant doctrine, and a specific relationship between central banks and markets. Over the past thirty-five years, advanced economies have moved through three radically different configurations.

1990–2008: the golden age of inflation targeting

This regime emerged from the victory over the inflation of the 1970s–1980s. After the Volcker tightening — Fed Funds reached 20% in June 1981 (Federal Reserve) — central banks progressively adopted inflation targeting as their reference doctrine. New Zealand led the way in 1990, followed by Canada (1991), the United Kingdom (1992), and the ECB from its creation in 1999.

During this period, monetary policy operated under a relatively stable pattern: policy rates fluctuated between 3% and 6% in the United States, tightening and easing cycles followed an orderly sequence, and the credibility earned by central banks enabled effective anchoring of inflation expectations. The Fed Funds rate rose from 3% to 6.5% between 1993 and 2000 (Federal Reserve), accompanying the “new economy” expansion without generating major inflationary drift.

The limits of this model were already visible. The focus on consumer price inflation led policymakers to overlook the buildup of financial imbalances — the dot-com bubble in 2000 and the housing and credit bubble between 2004 and 2007. Alan Greenspan cut Fed Funds from 6.5% to 1% between January 2001 and June 2003, a massive easing that laid the foundations for the next crisis. This sequence illustrates a recurring pattern: resolving one crisis through monetary policy sows the seeds of the next.

2008–2021: zero rates, QE, and financial repression

The 2008 financial crisis opened an unprecedented monetary regime in advanced economies. The Fed cut rates to the zero lower bound (0–0.25%) in December 2008, a level maintained for seven years until December 2015 (Federal Reserve). The ECB reached zero in March 2016 before moving into negative territory (−0.50% deposit facility). The Bank of Japan had already operated near zero rates since 1999.

Faced with the inability of rates to revive activity — the zero bound acting as an absolute constraint — central banks deployed unconventional tools on an unprecedented scale. Quantitative easing (QE) turned central bank balance sheets into financial asset sponges: the Fed’s balance sheet rose from $900 billion in 2008 to $4.5 trillion in 2015, then peaked at $8.965 trillion in April 2022 (Federal Reserve). The ECB’s balance sheet exceeded €8.8 trillion in June 2022 (BCE). The Bank of Japan pushed the logic further with Yield Curve Control (YCC), directly targeting the yield on 10-year government bonds.

This regime produced an environment of financial repression — persistently negative real rates that penalized savings and subsidized debt. The real 10-year Treasury yield, measured via TIPS, remained negative from 2012 to 2022 (Federal Reserve). This configuration profoundly redistributed wealth, inflating financial and real estate asset prices while compressing returns for savers and pension funds.

2022–?: the return of positive real rates and regime uncertainty

The 2021–2022 inflation shock forced an abrupt shift. The Fed raised rates by 525 basis points in 16 months between March 2022 and July 2023 — the fastest tightening cycle since the early 1980s (Federal Reserve). The ECB followed with a 450-basis-point increase between July 2022 and September 2023 (BCE). Even the Bank of Japan began dismantling its ultra-accommodative stance, abandoning YCC in March 2024 and raising its policy rate for the first time since 2007.

US 10-year real rates moved back above 2%, a level unseen since 2007. This return to a positive cost of capital represents a regime shift whose structural consequences are not yet fully absorbed. The central question for markets is the durability of this normalization: have advanced economies entered a structurally higher-rate regime (“higher for longer,” the Fed’s 2023 mantra), or will the next slowdown push central banks back toward the ultra-accommodative policies of the previous decade?

Different mandates, divergent responses

Major central banks do not share the same statutory objectives, which explains sometimes opposing responses to comparable economic shocks. The US Federal Reserve has pursued an explicit dual mandate since the Humphrey-Hawkins Act of 1978: price stability and full employment. The European Central Bank focuses primarily on inflation control, with an explicit 2% target “over the medium term” — deliberate temporal ambiguity that leaves room for interpretation. The Bank of Japan, confronted with decades of deflationary pressure, has developed a distinctive doctrine of yield curve control.

These doctrinal differences are not anecdotal. In 2022, facing a comparable inflation shock, the Fed raised rates by 425 basis points in one year while the ECB raised them by only 250 over the same period (Federal Reserve, BCE) — a gap reflecting the structural caution of an institution managing 20 heterogeneous economies with a single policy rate. The Bank of Japan, meanwhile, maintained its ultra-accommodative policy throughout 2022, accepting a 32% depreciation of the yen against the dollar rather than tightening prematurely.

Our in-depth analysis of why central banks target inflation rather than growth clarifies the theoretical and practical foundations of these institutional choices.

Independence: real autonomy or convenient fiction?

Central bank independence from political power is one of the major achievements of modern economic governance. It aims to shield monetary policy from short-term electoral pressures — the temptation to artificially stimulate the economy ahead of political deadlines, at the cost of fueling inflation later. Academic literature (Alesina & Summers, 1993; Cukierman, 2008) establishes a robust correlation between institutional independence and price stability.

This autonomy nevertheless remains fragile and conditional. In periods of acute crisis, the boundaries between monetary and fiscal policy blur. During the Covid crisis, the Fed purchased more than $3 trillion in assets in two years, indirectly financing the entirety of net US Treasury issuance in 2020 (Federal Reserve). The ECB, through its PEPP program, absorbed the bulk of euro area sovereign issuance during the same period. Implicit coordination with governments then becomes the rule rather than the exception — what some economists describe as “fiscal dominance.”

Political pressure on central banks has also intensified. Donald Trump’s criticism of Jerome Powell in 2018–2019, tensions between euro area governments and the ECB over sovereign yield spreads, and the democratic legitimacy question of unelected institutions making decisions with major redistributive consequences all weaken an institutional model that ultimately depends on public trust.

Our report on central bank independence between autonomy and constraint examines the tensions shaping this institutional model and their implications for markets.

Viewing central banks as perfectly rational and omniscient actors. They operate with lagged data, imperfect models, and under political and media pressure. Their effective room for maneuver is often narrower than their communication suggests.

Forward guidance: steering expectations

Since the 2008 crisis, central bank communication has become a monetary policy instrument in its own right — some analysts estimate it weighs as heavily as rate decisions themselves on financial conditions. Forward guidance — prospective guidance of expectations — influences financial conditions even before any concrete action. Announcing that rates will remain low “for as long as necessary” or “until inflation sustainably reaches 2%” immediately alters the behavior of economic agents.

The effectiveness of this tool has been empirically demonstrated. Mario Draghi’s “whatever it takes” in July 2012 — three words that were enough to reverse the European sovereign debt crisis — remains the most striking illustration of the power of a central banker’s words. The Italian 10-year spread over the German Bund, which had reached 537 basis points in November 2011 (BCE), compressed by half in the weeks following the statement — even before activation of the OMT (Outright Monetary Transactions) program.

This strategy nevertheless carries symmetric risks. Guidance that is too precise can trap a central bank if economic conditions evolve differently than expected — the May 2013 “taper tantrum” provided a costly example when Ben Bernanke’s mere suggestion of a future reduction in asset purchases triggered a 130-basis-point rise in the 10-year Treasury yield in three months (Federal Reserve). Guidance that is too vague, by contrast, loses effectiveness and leaves markets uncertain.

The mechanisms through which monetary expectations shape monetary policy transmission are decoded in our dedicated analysis. Among the most direct transmission channels, housing credit plays a central role: variable mortgage rates transmit central bank decisions almost instantly to household purchasing power, creating a powerful lever but also a source of systemic fragility.

One indicator synthesizes these expectations and their transmission to the economic cycle particularly well: the yield curve. Its shape — normal, flat, or inverted — reflects expectations for growth, inflation, and policy rate trajectories well before they materialize in economic data. The inversion of the 2-year/10-year curve, which persisted from July 2022 to September 2024 — the longest inversion since the 1980s (Federal Reserve) — crystallized debate about recession risk for more than two years.

Decision timing: acting at the right point in the cycle

The effectiveness of monetary policy depends crucially on when it is implemented. Acting too early risks stifling a nascent recovery; acting too late allows inflation to become entrenched or recession to deepen. Transmission lags — 12 to 24 months for peak impact according to conventional estimates — imply that central banks must act based on forecasts rather than observed data. Yet these forecasts are notoriously imprecise: the Fed’s inflation projections for the following year show an average absolute error of about 0.5 percentage points (Tulip, 2014; FRB Staff Projections).

The analytical framework within which these decisions are made — and its intrinsic limits — is examined in our study on the framework and limits of monetary policy. The question of optimal timing is explored further in our analysis of the economic cycle and monetary policy timing. For investors, real interest rates are a discreet but decisive signal: their level reveals the effective degree of monetary restriction or accommodation beyond nominal announcements.

Recurring central banker mistakes

Central bank governors are not infallible. The monetary history of the past thirty-five years is marked by diagnostic errors whose recurrence reveals structural biases rather than isolated accidents.

The 1994 surprise: tightening too fast

In February 1994, Alan Greenspan began an unexpected tightening cycle — Fed Funds rose from 3% to 6% in one year (Federal Reserve) — triggering a global bond market crash. The 30-year Treasury yield jumped 200 basis points in eight months. Orange County, California, declared bankruptcy. The lesson drawn — never surprise markets — paradoxically led to the opposite bias: excessive predictability that dulled market vigilance toward risks.

The ECB in 2011: a cycle misreading

In April and July 2011, Jean-Claude Trichet’s ECB raised rates twice, from 1% to 1.50% (BCE), citing temporarily elevated inflation. This decision ignored the fragility of euro area peripheral economies, then mired in the sovereign debt crisis. The Italian 10-year spread exploded above 500 basis points months later. Mario Draghi, taking office in November 2011, immediately reversed course — an implicit admission that the tightening had been a timing and diagnostic error.

The 2021 “transitory” episode: underestimating a regime shift

The most recent — and most costly — episode was the systematic underestimation of inflation in 2021. The Fed maintained the adjective “transitory” in official communication from March to November 2021 while CPI inflation accelerated month after month, rising from 1.7% in February to 6.8% in November (BLS). Jerome Powell acknowledged in November 2021 that it was “probably time to retire the word transitory.” The first rate hike came only in March 2022 — a delay of six to nine months relative to what leading indicators suggested.

This delay forced a brutal catch-up: 525 basis points in 16 months, the most aggressive tightening since Volcker. The global bond portfolio suffered its worst year in a century in 2022, with a 31% loss on long-term Treasuries (ICE BofA US Treasury 20+ index). US regional banks, exposed to unrealized losses on bond portfolios, faced a liquidity crisis in spring 2023 — the collapse of Silicon Valley Bank being directly linked to this reversal.

Structural biases, not isolated mistakes

These episodes reveal recurring biases. Excessive reliance on econometric models is a first pitfall: calibrated on historical data, these models struggle to capture regime breaks and unprecedented shocks. Fed projections anticipated PCE inflation at 2.4% by end-2021; the outturn was 5.9% (BEA) — a gap of more than 3 points rarely observed in institutional forecasting history.

Reluctance to surprise markets is another bias. Concerned about credibility, central bankers tend to validate market expectations rather than challenge them, even when circumstances require it. Asymmetry in the treatment of inflation and unemployment reinforces this tendency: central banks generally react more vigorously to rising unemployment than to inflation drift, creating a structurally accommodative bias whose consequences emerge over the long term.

These recurring errors raise a deeper question: do central banks truly control the economy, or do they merely influence its trajectory at the margin? Institutional constraints, transmission lags, and market dynamics severely limit their direct steering capacity. This issue is explored in our analysis dedicated to central banks and their real control over the economy. The return of positive real rates in 2022–2024 marked a major regime shift after a decade of negative real rates — a normalization many economic actors had not anticipated.

Our analysis of accommodative monetary policy before crises deciphers these mechanisms. The defensive approach to monetary policy to avoid the worst highlights the trade-offs central bankers face when choosing between tightening too early and easing too late.

Decoding central bank statements: a reading framework

Central bank statements follow a codified grammar whose mastery allows extraction of meaningful information beyond the surface message. Several elements deserve particular attention.

Even minor language changes often signal doctrinal shifts. Moving from “inflation should return toward target” to “inflation will return toward target” signals increased confidence. Adding or removing terms such as “gradual,” “patient,” or “vigilant” changes perceptions of the anticipated pace of adjustments. At the December 2023 meeting, inserting the word “any” into the phrase “any additional policy firming” was enough to trigger a 1.4% rally in the S&P 500 during the session — markets reading it as the end of the tightening cycle.

Economic projections — growth, inflation, unemployment — and their revisions from one meeting to the next reveal the evolving views of policymakers. The Fed’s “dot plot,” aggregating individual rate path expectations of the 19 FOMC members, is a privileged source of information. Its market power is considerable: shifting from three to two expected rate cuts for 2025 in the December 2024 dot plot weighed on equity indices for weeks.

Minutes published three weeks after each meeting shed light on internal debates and potential dissent. Close attention to dissenting votes — “hawks” favoring tighter policy, “doves” advocating accommodation — helps anticipate monetary policy shifts before they materialize in official decisions.

Monetary policy does not steer the economy — it attempts to correct excesses with delay, imperfect tools, and models calibrated on a past that never repeats itself exactly. The relevant diagnosis is not “Will the Fed cut rates?” but “Which monetary regime are we in, and which institutional biases will shape the mistakes of the next sequence?” Since 2022, the answer remains open — and this regime uncertainty shapes all contemporary financial trade-offs.

← Back to pillar page Monetary Policy & Rates