Crypto-Assets: Liquidity Cycles, Real Rates and Financial Integration

Liquidity cycles, real rates and financial integration: the macro drivers that shape crypto-asset valuation.

— Crypto-assets do not escape the monetary cycle. They amplify its effects.

To understand the economic and financial mechanisms driving crypto-assets, from liquidity cycles to valuation dynamics, see our investing for beginners hub.

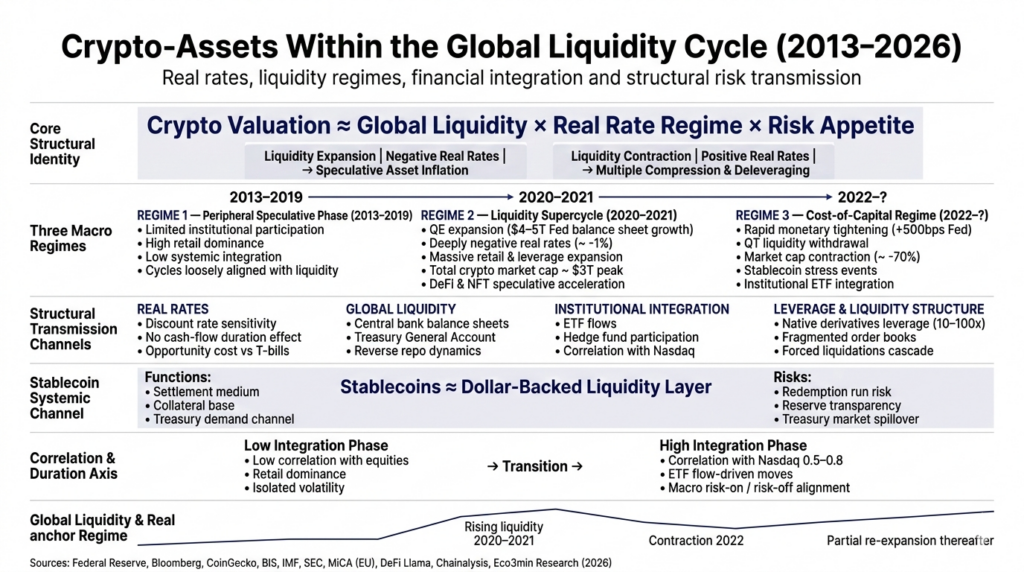

The more crypto-assets become institutionalized, the more macro-dependent they become. The original promise — a parallel monetary system decoupled from central banks and financial cycles — has collapsed when faced with real capital flows. Crypto-assets are not an alternative system — they have become an amplified extension of the existing financial system, whose valuation is governed by the same forces as long-duration traditional assets: global liquidity, real interest rates and risk appetite. The correlation between Bitcoin and the Nasdaq 100 reached 0.80 at the peak in 2022 (Bloomberg) — a level that invalidates any claim of decoupling. Spot Bitcoin ETFs approved in January 2024 (SEC) attracted $12 billion of net inflows in 3 months (Bloomberg) — integrating Bitcoin directly into institutional circuits and mechanically strengthening its dependence on the traditional liquidity cycle. Total crypto market capitalization moved from $3,000bn (peak November 2021) to $800bn (trough December 2022) and back above $2,500bn at the end of 2024 (CoinGecko) — a 73% collapse followed by a 200% rebound, synchronized with the global liquidity cycle rather than with any specific technological breakthrough.

This pillar proposes a strictly macroeconomic reading grid for crypto-assets — without promotion, techno-enthusiasm, or simplification. The objective is not to analyse blockchain technology or to evaluate speculative potential, but to formalize how crypto-assets interact with liquidity cycles (analysed in the sub-pillar Liquidity and financial conditions), real rates (developed in the Monetary policy pillar), market dynamics (covered in the Financial markets pillar) and geopolitical fragmentation (analysed in the sub-pillar Structural geopolitics). Product innovation and infrastructure dimensions are treated in the sub-pillar Financial innovation.

I — Nature: three categories, three economic functions

Crypto-assets denote digital assets built on distributed ledgers (blockchain) that enable exchange or representation of value without a centralized intermediary. It is important to distinguish three categories that do not share the same economic function, sensitivity to the cycle or risk profile.

Bitcoin: a fixed-supply digital monetary-like asset

Bitcoin behaves not as money but as a fixed-supply digital monetary-like asset (21 million units, cap embedded in the protocol). Its market capitalization reached $1,300bn at the end of 2024 (CoinGecko) — comparable to Spain’s GDP. Its programmed scarcity, censorship-resistance and quadrennial halving (50% issuance reduction, last in April 2024) make it a privileged object of analysis in a context of U.S. fiscal deficits of 6–7% of GDP (CBO) and questions about monetary sustainability.

But Bitcoin is not a reliable inflation hedge — that narrative collapsed in 2022. Its empirical behaviour reveals a dominant sensitivity to real rates and liquidity: Bitcoin lost 65% between November 2021 and November 2022 (CoinGecko), precisely during the monetary tightening phase (+525 bps by the Fed). It rebounded 150% in 2023 when financial conditions eased (Goldman Sachs FCI), despite policy rates remaining at 5.25–5.50%. Correlation with the Nasdaq 100 reached 0.80 (Bloomberg). Bitcoin behaves like a long-duration asset, ultra-sensitive to the cost of capital — not like an inflation hedge. The sub-pillar Bitcoin and liquidity cycles develops this analysis.

Ethereum and programmable blockchains: experimental financial infrastructure

Ethereum introduced the concept of smart contracts — automatic execution of financial rules without an intermediary. This innovation enabled decentralized finance (DeFi), whose total value locked (TVL) peaked at $180bn (November 2021, DeFi Llama) before falling to $38bn at the 2022 trough — an 80% swing perfectly synchronized with the liquidity cycle rather than with technological adoption. TVL climbed back above $90bn by the end of 2024 (DeFi Llama).

Ethereum functions as a programmable financial infrastructure whose value depends on network activity (transaction fees, smart contract deployments, DeFi volumes). The transition to Proof of Stake (The Merge, September 2022) reduced energy consumption by 99.95% (Ethereum Foundation) and introduced a deflationary mechanism (EIP-1559: a portion of fees is burned). Still, Ethereum’s valuation remains governed by the same forces as Bitcoin — liquidity, real rates, risk appetite — with amplified sensitivity (beta > 1 relative to the cycle). The sub-pillar Ethereum and stablecoins expands on this analysis.

Stablecoins: systemic liquidity instruments

Stablecoins — crypto-assets pegged to fiat currencies, primarily the dollar — occupy a central function in the ecosystem. Their combined capitalization exceeds $130bn (CoinGecko, 2024), dominated by Tether (USDT, ~ $90bn) and USD Coin (USDC, ~ $25bn). They serve as liquidity vehicles for crypto trading, gateways between crypto-finance and traditional finance, and relative safe havens during corrections.

Stablecoins raise major systemic issues. Tether holds roughly 80% of its reserves in U.S. Treasuries (Tether attestation, 2024) — making it one of the largest non-bank holders of U.S. sovereign debt. The collapse of TerraUSD (UST) in May 2022 — an algorithmic stablecoin that lost 100% of its value in 72 hours, erasing $40bn of market cap (CoinGecko) — showed that stablecoin liquidity can vanish instantly and trigger cascading contagion (Three Arrows Capital, Celsius, FTX). The parallels with money market funds (2008 Reserve Primary Fund “breaking the buck”) are structural: abundant liquidity in normal times, potential for runs in stress.

II — Macro dependence: crypto-assets as long-duration instruments

The central thesis of this pillar is that crypto-assets operate as long-duration, zero-cash-flow assets, highly sensitive to the cost of capital. Their valuation depends on the same triad as high-multiple growth equities:

The central thesis of this pillar is that crypto-assets operate as long-duration, zero-cash-flow assets, highly sensitive to the cost of capital. Their valuation depends on the same triad as high-multiple growth equities: global liquidity, real interest rates and expectations.

, real interest rates and expectations. When liquidity is abundant and real rates are negative, crypto-assets outperform. When liquidity tightens and real rates turn positive, they underperform — with amplified amplitude due to absence of fundamental cash flows, native leverage in the ecosystem and fragile liquidity.The liquidity cycle as the primary determinant

Each major Bitcoin bull phase coincided with an expansion of global liquidity — and each bear phase with contraction. 2020–2021: the Fed injected $4,800bn via QE (Federal Reserve), real rates were -1.19% (TIPS, Aug 2021), Bitcoin rose from $6k to $69k (+1,050%, CoinGecko). 2022: the Fed raised rates from 0% to 4.50% in 9 months and began QT (-$95bn/month), Bitcoin fell from $69k to $16k (-77%, CoinGecko). 2023–2024: financial conditions eased de facto (Goldman Sachs FCI) despite policy rates at 5.25–5.50%, and Bitcoin climbed from $16k to above $70k (+340%). Correlation with Fed liquidity net measures (Fed balance sheet – Treasury General Account – Reverse Repo) has exceeded 0.70 since 2020 (Bloomberg).

This liquidity dependence is explained by market structure. Crypto-assets have no cash flows (no dividends, coupons, or rents) — their valuation rests entirely on expectations of future prices, which themselves depend on liquidity available for risk-taking. When cash yields 5.25% risk-free (T-bills, Federal Reserve), the opportunity cost of holding a zero-yield asset rises mechanically — and flows reallocate. The sub-pillar Liquidity and financial conditions explains transmission mechanisms in detail.

The end of the decoupling promise

Bitcoin–Nasdaq correlation was close to 0 before 2020 (Bloomberg). It rose to 0.50–0.80 between 2021 and 2023 (Bloomberg). The explanation is structural, not cyclical: institutional entry (hedge funds, family offices, ETFs) integrated crypto-assets into the same allocation circuits as tech equities. A generalized risk-off — like June 2022 (FOMC +75 bps) or August 2024 (yen carry unwind, VIX 65) — now affects Bitcoin and Nvidia in similar ways. “Crypto diversification” no longer exists for institutional portfolios — which is why crypto analysis belongs to the same framework as correlation dynamics in the Financial markets pillar.

Crypto cycles: euphoria and purge synchronized with the monetary cycle

A common error is to confuse technological adoption with financial cycles. Crypto bull phases do not correspond to fundamental advances — they correspond to liquidity expansions. The 2020–2022 cycle is paradigmatic. Expansion phase (2020–2021): massive QE, negative real rates, excess capital → total crypto market cap from $300bn to $3,000bn (+900%, CoinGecko). Euphoria phase (2021): narrative amplifiers (NFTs, DeFi, Web3, “supercycle”), native leverage (DeFi protocols 10–20×, CEX up to 100×), speculation on tokens without utility, TVL 180bn. Tightening phase (2022): Fed +425 bps, QT → sequential collapses: TerraUSD/Luna (May, -$40bn), Three Arrows Capital (June, -$10bn), Celsius (June, withdrawal freeze), FTX (Nov, fraud + bankruptcy, -$8bn client losses). Total market cap $800bn (-73%). Recovery phase (2023–2024): de facto easing of financial conditions, rate-cut expectations, spot ETFs approved → market cap $2,500bn+.

Technological narratives — AI, tokenization, RWA (Real World Assets) — act as cyclic amplifiers: they provide intellectual justification for risk-taking in liquidity-rich phases and disappear in contraction phases. They are not the engine — liquidity cycles are. The sub-pillar Cycles and volatility develops this analysis and the structural mechanisms (fragmented liquidity, lack of stabilizing market-makers, native leverage) that explain the amplitude of swings.

III — Systemic integration: regulation, geopolitics and structural risks

Accelerated institutionalization

SEC approval of spot Bitcoin ETFs in January 2024 is an inflection point. The 11 approved ETFs drew more than $12bn of net inflows in 3 months (Bloomberg), with BlackRock’s iShares Bitcoin Trust (IBIT) becoming the fastest-growing ETF at launch (10bn AUM in 7 weeks, Bloomberg). Spot Ethereum ETFs followed in May 2024 (SEC). This institutionalization has three structural consequences. First, it reinforces correlation with traditional assets — Bitcoin enters the same portfolios, risk management systems and allocation flows as equity and bond ETFs. Second, it increases market depth — ETF volumes now represent a significant share of total Bitcoin volume. Third, it subjects crypto-assets to the same regulatory constraints as traditional assets — reporting, compliance and market surveillance.

Regulation: MiCA, SEC and the race to framework

The MiCA regulation, effective in the EU in December 2024, is the first comprehensive crypto-assets framework in a major jurisdiction. It imposes reserve requirements for stablecoins (1:1 reserves, segregation, audit), licensing obligations for crypto service providers, and transparency rules for token issuers. In the U.S., the approach remains fragmented between an enforcement-driven SEC and the CFTC (derivatives regulator), without a unified legislative framework — creating legal uncertainty that pushes some actors to clearer jurisdictions (EU, Dubai, Singapore).

Regulation produces two contradictory effects. It reduces systemic risk by imposing reserve norms on stablecoins and excluding fraudulent actors (post-FTX). But it also accelerates integration into the existing system — and therefore correlation with traditional cycles. The more regulation frames the space, the more crypto-assets resemble classic financial assets — and the further the “alternative system” promise drifts. The sub-pillar Regulation and structural risks expands on this analysis.

Monetary geopolitics: digital dollar, sanctions and CBDCs

Crypto-assets sit within monetary sovereignty tensions analysed in the sub-pillar Structural geopolitics and the sub-pillar Dollar and the global system. Russia used crypto-assets to partly circumvent Western sanctions after 2022 — rouble flows to crypto platforms multiplied by 5 in the weeks following the invasion (Chainalysis, 2022). China banned mining and crypto trading (2021) while launching a digital yuan (e-CNY) — illustrating the choice of full monetary sovereignty over decentralization. Over 130 countries are exploring central bank digital currencies (CBDCs, Atlantic Council 2024) — the rivalry between public monetary infrastructures (CBDCs) and private ones (stablecoins, Bitcoin) will shape monetary geopolitics for decades.

Structural risks: what persists despite institutionalization

Institutionalization reduces some risks (fraud, opaque stablecoin reserves) but does not eliminate structural risks inherent to crypto-assets. Liquidity risk remains dominant: Bitcoin’s order book is 10–20x thinner than the S&P 500’s (Kaiko), meaning price moves are amplified versus traditional markets. Concentration risk is high: the top 100 addresses hold roughly 15% of total Bitcoin supply (Glassnode), and the three largest stablecoins represent 90% of stablecoin capitalization (CoinGecko). Leverage risk is native: platforms offer 10–100× leverage on crypto derivatives, generating cascade liquidations during corrections (> $1bn liquidated in 24h during the August 2024 flash crash, CoinGlass). Technology risk persists: DeFi hacks exceeded $3bn cumulative in 2022 (Chainalysis).

What crypto-assets will not change

Crypto-assets will not eliminate economic cycles, central banks, or financial risk. Bitcoin’s programmed scarcity (21 million units) does not shield it from monetary tightening — 2022 proved this (-77%). Ethereum smart contracts do not remove counterparty risk — they shift it to code risk (bugs, exploits, governance). Stablecoins are not “safe digital dollars” — they are parity promises backed by reserves whose quality and transparency vary. TerraUST’s collapse (-100% in 72 hours, -$40bn, May 2022) is empirical proof that decentralization does not prevent runs — it can accelerate them.

Analysing crypto-assets lucidly requires simultaneously recognising that blockchain infrastructure is a significant innovation in financial programmability — and that its valuation remains fully subject to the same macro forces as traditional assets. Technology can be revolutionary; its valuation does not escape the monetary cycle.

The more crypto-assets institutionalize, the more macro-dependent they become. The decoupling promise has collapsed: Bitcoin/Nasdaq correlation reached 0.80 (Bloomberg); every major bull phase coincided with liquidity expansion (QE $4,800bn, real rates -1.19% → Bitcoin +1,050%); every major bear phase with contraction (Fed +525 bps → Bitcoin -77%). Spot ETFs ($12bn of flows in 3 months, Bloomberg) fully integrated crypto-assets into institutional circuits. Stablecoins ($130bn, dominated by Tether) are systemic liquidity instruments whose reserves (largely Treasuries) tie them directly to the traditional financial system. Regulation (MiCA in the EU, SEC in the US) reduces fraud risk but accelerates convergence toward classic assets. Structural risks persist: liquidity 10–20× thinner than traditional markets (Kaiko), native leverage 10–100×, high concentration, DeFi hacks > $3bn cumulative (Chainalysis). Programmed scarcity does not protect against monetary tightening — technology can be revolutionary, but its valuation remains subject to the monetary cycle.