Signal-Less Market Phases: When Indicators Stop Reflecting Risk

The signal-less phases describe a particular market regime in which synthetic indicators stop providing useful information about the true level of risk. This regime occurs when several macroeconomic dynamics — expansion, monetary stance, liquidity conditions — operate together without any one of them clearly dominating. Information does not disappear; it cancels itself out at the level of broad indices, masking a growing divergence between assets and corporate trajectories. The classic mistake is to read this apparent calm as a sign of normalization or fading risk. This analysis unpacks the structural forces behind these periods, their link to the maturity of the cycle, and the inherent limits of frameworks based only on aggregate data.

This type of regime corresponds to market dynamics driven by neutralized expectations, where the coexistence of contradictory macroeconomic forces prevents the emergence of a readable directional signal at the index level.

This analysis builds on the institutional frameworks of macro-financial cycles, as developed by the Bank for International Settlements and the IMF in their work on financial stability and dispersion dynamics at the end of the cycle.

When markets seem clear… even though they are no longer clear

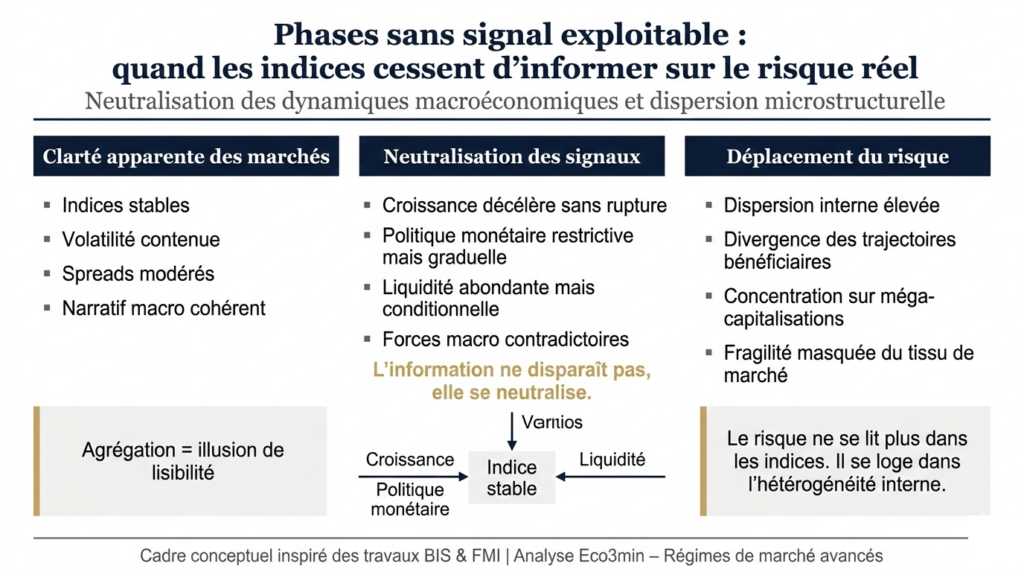

Certain market sequences create the illusion of great clarity. Indices move within tight ranges, volatility recedes, the dominant narratives appear firmly anchored, and the main asset classes seem to send consistent signals. Behind that calming surface, however, something is unraveling. Not a single indicator, nor a dramatic data point, but the market’s own ability to generate usable signals.

These sequences belong neither to panic nor to euphoria. They correspond to a quieter regime, often misdiagnosed, in which aggregate indicators gradually lose their informational power over the reality of risk. Markets do not become unreadable because they are too nervous, but because the signal is saturated. The data remain, but they cancel each other out.

This phenomenon, rarely identified as such, is nonetheless a structural indicator. It does not imply an imminent reversal, but it reveals a great deal about the regime in which investors are operating. Understanding why markets enter these phases of informational silence makes it easier to grasp internal dispersion, cycle shifts, and the growing limits of conventional approaches.

This analytical framework extends the approach developed on the Financial Markets pillar page, which is specifically designed to go beyond simple index observation and decode the underlying mechanisms.

When markets go quiet, it is not because they have nothing left to say — it is because they are speaking at another level.

The mirage of aggregate indicators

Contemporary markets rely heavily on synthetic indicators. Equity indices, implied volatility, credit spreads, long-term rates, and macro surprise indices condense vast amounts of information into readable signals. This aggregation is valuable in early and mid-cycle phases, when dynamics remain relatively homogeneous and the dominant macro forces affect all assets in the same direction.

As the cycle matures, however, that aggregation becomes a source of illusion. Averages conceal a widening internal fracture. Assets stop responding uniformly to the same impulses. Some companies absorb a higher cost of capital with ease; others begin to feel it acutely. Some earnings trajectories remain legible; others become erratic. Yet the index continues to display a form of stability.

The problem is not that the indicators are wrong, but that they are incomplete. They still measure what they are designed to measure, even though the relevant object of observation has changed. The market is no longer governed by a dominant factor, but by a combination of partially antagonistic forces that cancel each other out at the aggregate level.

The disappearance of the signal: a structural phenomenon

A signal-less phase does not mean the absence of information. It means information saturation. Signals still exist, but their coherence fades. Indicators stop converging and begin sending ambiguous, sometimes contradictory, messages depending on the angle of analysis.

It is important to distinguish statistical noise from this disappearance of the signal. Noise refers to short-term agitation, to erratic oscillations. The disappearance of the signal, by contrast, unfolds over time. It reflects a regime in which historical relationships between variables distort without fully breaking down. Correlations do not collapse; they become unstable.

What this phenomenon truly measures is not a market direction, but a transformation in the decision-making architecture. Trade-offs become more complex, the established hierarchy among factors becomes less clear, and risk analysis requires greater granularity.

This loss of readability at the aggregate level does not mean risk has disappeared; it has moved. When indices stop emitting a clear signal, information recomposes itself at a finer level: the dispersion of performance across companies. In late-cycle phases, it is less the market as a whole that speaks than the widening gaps between individual trajectories, a mechanism analyzed in our piece on equity performance dispersion and the increasingly selective nature of the market.

- It does not provide a buy or sell signal

- It does not predict a crash or reversal

- It does not replace valuation analysis

What the market can no longer reflect

In these phases, the aggregate market no longer captures the dispersion of risk. It does not reflect the heterogeneity of financial structures, the divergence of profitability paths, or the differing sensitivity to the cost of capital. It projects a stabilized image of a deeply fragmented whole.

Why this regime emerges late in the cycle

Signal-less phases typically emerge when the macroeconomic cycle reaches maturity. Growth slows without collapsing, monetary policy tightens without immediately triggering a sharp contraction, and the cost of capital stops being neutral.

In that context, real rates become central. Their gradual rise acts as a selective filter. It does not trigger a uniform correction; it widens the gap between robust business models and vulnerable ones. This mechanism has been examined in depth in the pillar article on real policy rates, which shows how they quietly reshape the landscape of risky assets.

Liquidity also changes in character. It remains abundant at the global level, but becomes more conditional. It concentrates in certain segments of the market and gradually withdraws from areas perceived as riskier or less transparent. This movement amplifies dispersion without creating immediate systemic stress.

From beta regime to selective regime

At the start of a cycle, beta rules. Being exposed to the market is usually enough to capture most of the performance. Late in the cycle, that regime fades. Performance becomes increasingly idiosyncratic. The market no longer rewards broad exposure, but the ability to navigate a fragmented environment.

Earnings, dispersion, and microstructure

Corporate earnings are among the clearest reveals of this disappearance of the signal. Earnings paths stop moving in tandem. Positive and negative surprises offset each other at the aggregate level, but they point to growing dispersion at the microeconomic level.

This dynamic lies at the heart of the analysis developed in the article on earnings surprises. When the dispersion of surprises increases without producing a marked directional move in indices, it signals that the market has shifted into a regime in which the aggregate signal has been neutralized.

Sector dynamics are not immune to this phenomenon. Even traditionally defensive sectors become heterogeneous. Some companies retain strong visibility, while others face greater competitive, regulatory, or financial pressure. Market-cap weighting reinforces this illusion of stability by overrepresenting dominant players at the expense of the rest of the market.

Why indices can remain stable

The apparent stability of indices in these phases relies heavily on concentration effects. A few large-cap names, with strong balance sheets and predictable cash flows, are enough to keep the index afloat. That stability masks the gradual weakening of the underlying market fabric.

Decoding the regime, not predicting the market

A disappearance-of-the-signal regime is neither a market-timing tool nor a crash indicator. It does not allow one to date a turning point or anticipate a sharp correction. Its value lies elsewhere. It provides a framework for understanding the market regime.

In such an environment, naïve strategies lose effectiveness. Passive investing remains exposed to growing concentration risk. Systematic approaches based on stable historical relationships become more fragile. By contrast, balance-sheet quality, earnings visibility, and financial discipline take on disproportionate importance.

This regime can last. It is not transitory by nature. As long as macro forces continue to neutralize one another without resolving, as long as the cost of capital keeps filtering without triggering a systemic shock, the market can remain in this intermediate state for a long time.

The neutralization of aggregate signals reflects a regime of high internal dispersion in which risk shifts from indices to microeconomic trajectories.

The key takeaway is not a directional conclusion, but a method of reading. When markets stop producing usable signals, that is not a malfunction. It is information in itself. It indicates that risk can no longer be read in the indices, but in their growing inability to reflect the market’s internal reality.

- Stable indices ≠ healthy market

- Aggregate signal neutralized by dispersion

- Risk displaced, not erased

- Micro reading > aggregate macro reading

This reading framework fits within a structural approach to financial markets, grounded in the observation of dispersion regimes and late-cycle dynamics documented in the institutional literature.

In these phases, the challenge is not to predict, but to understand. Not to anticipate an event, but to recognize a regime. It is often in that ability to detect the absence of a signal that the difference lies between a superficial reading of the market and a truly structural analysis.

Mis à jour : 20 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.