The Dollar and Your Portfolio: The Second Variable Inside Every Non-U.S. Allocation

European investors holding a World ETF carry hidden dollar exposure on most of their allocation. Reserve-currency status, real-rate differentials and commodity pricing transmit dollar moves into returns typically misattributed to asset selection alone.

The dollar is the second variable embedded in every non-U.S. portfolio. Reserve-currency status, capital flows and commodity pricing transmit its moves into returns that European investors typically attribute to asset selection alone.

TL;DR

A European 'diversified' portfolio across World ETF, emerging markets, commodities and gold is effectively one concentrated bet on the dollar regime, swinging from -5% to +15% in a year.

- The dollar's medium-term direction follows U.S.-versus-rest-of-world real-rate differentials over six- to twenty-four-month horizons: strong-dollar regimes (early-1980s Volcker, 2022-2024) line up with high U.S. real rates, softer phases (2010-2021) with low ones.

- Because that one variable drives commodities and emerging markets alike, a non-U.S. investor crediting 'the rally in U.S. tech' while ignoring a five-point dollar gain against the euro mis-attributes roughly half the year's return.

A European holding a World ETF carries dollar exposure on more than 60% of the allocation, whether they framed it that way or not. The question is not whether to bear that risk — it is whether to read it.

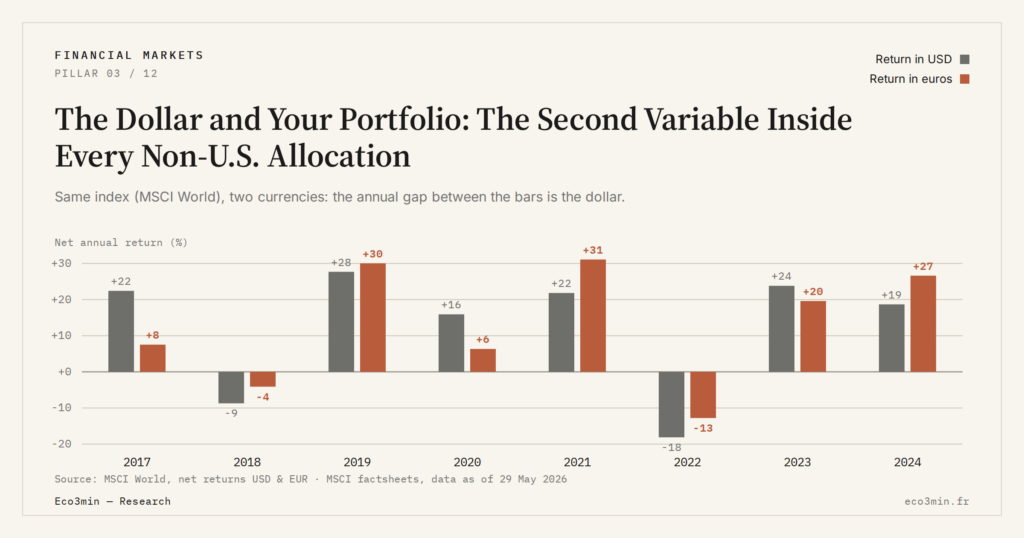

An MSCI World ETF reports +15% over the year in dollars. The European investor sees +8% in their brokerage account. Seven points have evaporated, and the gap owes nothing to hidden fees or a calculation error. It comes from the euro’s move against the dollar. When the dollar weakens, part of the dollar-denominated gain is absorbed by euro appreciation; when it strengthens, the euro-translated return runs ahead of the dollar performance. The mechanism is mechanical, and its annual magnitude — several percentage points — is large enough to dominate the return contribution of asset selection itself. Related coverage: the currency effect on a gold position.

That makes the dollar the most consequential currency in any portfolio that is not euro-purely-domestic. It is also the currency in which most international transactions, foreign-exchange reserves, emerging-market debts and commodities are denominated. Reading how the dollar functions inside the global monetary system means reading a variable that mechanically affects the return of nearly every asset class — even when the underlying is not American.

Reserve-currency status: a structural anchor, not a cyclical detail

According to IMF COFER data, the dollar still accounts for roughly 58% of global foreign-exchange reserves. That share has declined since the early 2000s — it stood at 72% in 2001 — but the gap with the second reserve currency remains wide: the euro does not exceed 20%, and no other currency comes close.

This is not a symbolic standing. When central banks accumulate reserves in dollars, they buy dollar-denominated assets, primarily U.S. Treasury bonds. The structural demand that follows simultaneously supports the dollar’s external value and the price of U.S. government debt — which means the financing cost of the U.S. economy is partly subsidised by foreign reserve managers. The mirror of that arrangement is dependence: any meaningful confidence shock that pushed reserve holders away from the dollar would transmit to U.S. yields, then to the global cost of capital, with consequences far beyond a currency adjustment. Each major strong-dollar regime and its transmission to markets has historically reshaped financing conditions outside the United States, particularly in emerging economies carrying dollar-denominated debt.

For a European holder of an international portfolio, the practical consequence is that the dollar is not merely an exchange-rate risk: it is a systemic risk that surfaces inside cross-asset correlations. The dataset tracking the dollar through global crises since 1973 shows that every major financial crisis of the past fifty years had a dollar component — either because a sudden surge squeezed non-U.S. borrowers carrying dollar debt, or because dollar weakness coincided with rushed reallocations into other safe-haven assets. The wider context: why a strong dollar can persist without a global crisis. Our analysis of systemic risk indicators and financial market stress signals lays out the underlying framework.

Real-rate differentials: the mechanism behind dollar trends

The dollar does not drift randomly. Over six- to twenty-four-month horizons, its direction is driven by real interest-rate differentials between the United States and the rest of the world.

The mechanism is straightforward. When U.S. real rates run above those in the euro area or Japan, international capital flows toward dollar assets to capture the yield advantage. The inflow lifts the dollar. When the differential narrows — because the Fed cuts, because the ECB hikes or because foreign inflation falls faster — the flow reverses and the dollar weakens. This capital-flow channel dominates exchange-rate moves over medium horizons and tends to swamp the trade-balance channel that textbooks emphasise.

The long history of U.S. real interest rates places the current configuration in context. Each episode of structurally high U.S. real rates — the early 1980s under Volcker, 2022–2024 in the post-pandemic tightening — has coincided with a strong-dollar regime. Each episode of low or negative real rates — most of the 2010–2021 decade — has corresponded to a softer, range-bound dollar. The correlation is imperfect, distorted by crisis episodes, central-bank intervention and geopolitical shocks, but it provides a robust frame for reading the dollar’s directional trend.

Why the dollar surfaces in commodities and emerging markets

That direction transmits to asset classes most European investors hold without explicitly mapping their dollar exposure. Commodities are priced in dollars: a stronger greenback typically pushes oil, copper and gold lower in dollar terms even when underlying supply-demand balances are unchanged, because the same barrel becomes more expensive in importer currencies and physical demand softens at the margin. Emerging-market equities and bonds carry an even tighter link: countries running current-account deficits financed in dollars face mechanically tighter financial conditions when the dollar rises, which depresses local growth, local-currency assets and dollar-denominated sovereign spreads simultaneously.

The implication is uncomfortable. A European holding what looks like a diversified portfolio — World ETF, emerging-market exposure, a commodity sleeve, perhaps gold — is, in effect, running a single concentrated factor bet: the dollar regime that prevails over the holding period. Asset-class correlations across regime shifts document the pattern: the apparent diversification across asset classes collapses precisely when dollar conditions tighten, because the same variable drives all the moving parts. A related question: why contango erodes commodity ETF returns.

What this means for reading portfolio performance

The takeaway is not a hedging prescription — currency hedging carries its own costs, and the appropriate posture is regime-dependent. It is informational. A non-U.S. investor who explains a strong year by “the rally in U.S. tech” while ignoring that the dollar appreciated five points against the euro is mis-attributing roughly half of the return. The same investor in the symmetric year — equities up in dollars but the dollar down against the euro — will see a flat statement and conclude their selection was poor, when the currency leg simply offset the asset leg.

Reading the dollar means watching what it watches: U.S.–rest-of-world real-rate gaps, Fed reaction-function shifts, term-premium moves on the long end of the Treasury curve and signals from the foreign-exchange reserve managers themselves. None of these will produce a tradeable signal on a given Monday. Taken together, they explain why the same global equity portfolio can deliver −5% or +15% to its European holder in any given year — without a single line of the underlying allocation having changed.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…