Monetary Policy Lags: Why Rate Changes Take Time to Impact the Economy

Why monetary policy decisions take time to affect the real economy: indirect channels, financial frictions, and lagged effects.

Monetary policy operates with a structural lag. Between a central bank decision and the observable adjustment in activity, inflation, or investment, the economy passes through a chain of intermediate mechanisms shaped by financial and contractual frictions.

Understanding this timing prevents confusing slowness with inefficiency. Transmission channels are neither synchronous nor automatic: they depend on private balance sheets, financing structures, and agents’ expectations. The macroeconomic response reflects sequential propagation, not an instantaneous effect.

Monetary policy decisions are often assessed based on their immediate effects, even though they operate within a deeply frictional economic system. Between the moment a central bank acts and when activity, inflation, or investment respond, multiple intermediate mechanisms come into play. These transmission channels are neither synchronous nor automatic: they depend on balance sheets, financial structures, and agents’ expectations.

This reality fuels a common misunderstanding, where the absence of a rapid response is interpreted as inefficiency. Placing these delays and asymmetries back into their economic logic helps clarify the true macro-financial timing of monetary policy. The data cited comes from publications by the ECB, the Federal Reserve, the Bank for International Settlements, and national statistical institutions.

What makes this topic more strategic than it appears is the growing gap between the speed of monetary announcements and the slow pace of real adjustments. In an environment where rate cuts initiated since 2024 are already fueling expectations of recovery, the effective transmission timing becomes critical to correctly interpreting the phase of the cycle.

A fragmented transmission architecture

Monetary policy does not operate through a single channel. A detailed mapping of monetary transmission channels helps explain why observed effects are spread over time. Policy rates set by a central bank first influence interbank conditions, then propagate to bond yields, credit conditions, asset prices, and exchange rates. Each of these vectors follows its own timeline. Market rate channels react within days. The bank lending channel takes several quarters to produce tangible effects on consumption or investment.

This estimate dates back to Milton Friedman’s work in the 1960s on “long and variable lags.”

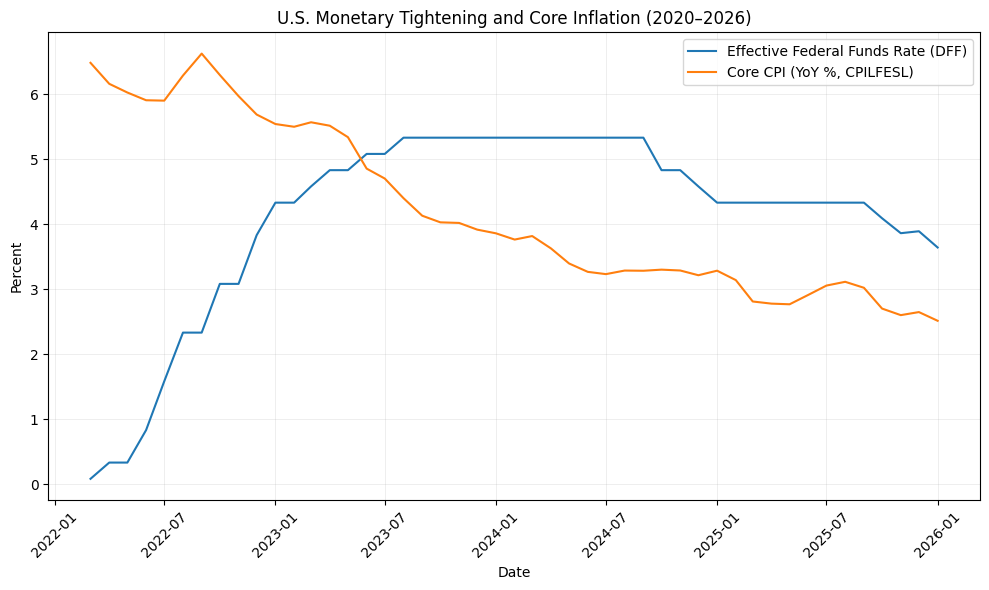

These delays were particularly visible during the recent cycle of rate hikes and their lagged effects, where the impact on real activity materialized well after the peak in policy rates.

The average lag between a monetary action and its observable impact on real activity ranges between 12 and 24 months—an order of magnitude that recent cycles have not fundamentally altered. Mapping the different monetary transmission channels helps explain why these timelines do not add up linearly.The role of liquidity and financial conditions in the transmission sequence is critical: they form the first observable link in the chain, well before adjustments in the real economy.

The credit and bank balance sheet filter

Monetary transmission largely operates through the banking system, as detailed in our analysis of monetary transmission through bank lending. However, banks do not mechanically pass through changes in policy rates. Their lending decisions depend on balance sheet strength, regulatory constraints (Basel III, leverage ratios), and their perception of default risk.

According to the ECB’s Bank Lending Survey (Q4 2025), euro area banks maintained restrictive lending standards for corporate loans, despite the start of the rate-cutting cycle. The Fed’s Senior Loan Officer Opinion Survey (January 2026) confirms a similar dynamic: monetary easing does not automatically translate into looser credit conditions.

Confusing lower policy rates with an actual easing of credit. A central bank lowers a benchmark rate, but commercial banks adjust their lending conditions based on their own balance sheet constraints. The gap between the two creates a blind spot where monetary policy appears ineffective, when it simply has not yet reached the productive economy.

This reality primarily affects non-listed companies dependent on bank financing, whose investment capacity remains tied to the effective supply of credit. The banking channel thus structurally shapes the real effectiveness of monetary policy by filtering impulses from policy rates.

Expectations and the forward-looking dimension

Monetary policy operates as much through its signals as through its decisions, particularly via the role of expectations in monetary transmission. When a central bank communicates its future path—forward guidance—markets immediately adjust asset prices and yield curves, well before the real economy moves. Agents’ expectations can alter transmission effectiveness, sometimes more powerfully than the instruments themselves.

The baseline scenario adopted by many market participants in early 2026 assumes a soft landing, where monetary easing gradually restores financing conditions. This view relies on the assumption of smooth and steady transmission. However, Atlanta Fed President Raphael Bostic stated in November 2022 that it could take “18 months to two years or more” for rate hikes to fully take effect. If this framework also applies during easing phases, rate cuts initiated by the ECB and the Fed since 2024 may only reach their full impact on credit and investment by 2026–2027.

Asymmetries and lagged effects on prices

Transmission lags are not only long—they are asymmetric. The contractual and financial mechanisms that delay the impact of rate hikes do not reverse symmetrically during rate cuts. Fixed-rate contracts, multi-year investment commitments, and wage adjustments create frictions that slow any change in direction.

This asymmetry is particularly visible in price dynamics.Inflation responds with a lag to monetary decisions, as analyzed in our study on inflation’s delayed response to monetary policy, due to nominal rigidities, indexation mechanisms, and cost chain inertia. According to Eurostat data, core inflation in the euro area took nearly 18 months to begin a meaningful decline after tightening started in July 2022.

Transmission also varies across regions. Financial fragmentation within the euro area creates uneven transmission within a single monetary zone: the same ECB decision produces different effects depending on banking structures and national debt levels.

Monetary transmission is not a technical delay: it is a structural filter that redistributes effects based on balance sheets and financial positions.

- The average lag between a rate decision and its effect on real activity ranges between 12 and 24 months depending on the channels involved.

- Commercial banks filter transmission based on their balance sheets and regulatory constraints, not just policy rate levels.

- Effects are asymmetric: rate cuts do not produce a mirror image of hikes due to contractual and nominal rigidities.

Several paths remain possible. If transmission channels gradually normalize, monetary easing could support activity in the medium term. But if bank balance sheets remain constrained or inflation expectations become unanchored, delays could lengthen further. According to BIS data (2025), the credit-to-GDP ratio in advanced economies remains about 15 points above its 2019 level, structurally altering the economy’s sensitivity to monetary impulses.

For companies, the effective cost of financing does not decline at the pace of announcements. For bond markets, yield curves embed transmission assumptions that reality may contradict. For households, mortgage and consumer credit conditions evolve with a lag that blurs cyclical interpretation. The ability of central banks to calibrate policy is measured less by the initial decision than by the depth and duration of its diffusion into the real economy.

Mis à jour : 20 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.