Real Policy Rates: The Invisible Tightening Driving Markets

Real policy rates have emerged as the essential compass for financial markets. Often pushed into the background in central bank rhetoric, these indicators nonetheless determine the true stance of monetary policy, the price of risk, and the direction of economic cycles.

Key takeaways at a glance

- The decline in inflation has pushed real rates into positive territory, without any change in nominal rates.

- This invisible tightening makes monetary policy far more restrictive than it appears.

- A sustained environment of positive real rates compresses valuation multiples, particularly for assets with long-duration cash flows.

- Investors have not yet fully priced in this new structural regime.

This analysis deciphers the mechanics of real policy rates and their implications across the financial system, from funding costs to portfolio allocation decisions.

It is not a market timing tool, but a regime indicator, essential for understanding the price of capital and valuation dynamics over a multi-year horizon.

This study relies on official data from major central banks,

harmonized inflation indices, and key macro-financial indicators

used by the analyst community.

The approach is structural and regime-based: it aims to highlight the persistent effects of real policy rates on the cost of capital, cycle dynamics, and valuation levels, independently of short-term communication or central bank meeting calendars.

The silent reversal in real rates

Since early December 2025, a technical variable has moved to the forefront without attracting media attention: real policy rates, that is, central bank benchmark rates adjusted for inflation.

With core inflation returning to around 2.2% in the euro area and 2.5% in the United States according to the latest releases from Eurostat and the Bureau of Labor Statistics (late 2025), real rates now range between +1 and +1.5 percentage points. In practical terms, monetary policy has tightened mechanically, without any need for nominal rate hikes.

This shift fundamentally alters the cost of money, corporate financing conditions, and the risk premium required on financial assets. Yet a significant share of market participants continues to interpret disinflation as monetary easing—a misreading with important consequences.

This perception bias is widespread because markets predominantly think in nominal terms. However, when real rates turn positive while growth is slowing, historical evidence suggests that transitions are rarely linear. The persistence of an

inverted yield curve

reinforces this gap between a reassuring narrative and the underlying reality of the cycle.

Past episodes show that sustained inversion of the 2Y–10Y spread has preceded most U.S. recessions since 1976, with a median lag of around 14 months—as documented in

the full history of yield curve inversions

.

Beyond the level of rates, monetary constraint primarily operates through liquidity and financial conditions. A positive real rate does not only affect the price of capital: it tightens access to funding, raises lending standards, and alters the effective circulation of money within the system, well before the real economy shows visible signs of slowdown.

Understanding how real rates are calculated — and why it matters

The formula is simple, but its implications are significant:

- Ex post real rate: policy rate minus observed inflation

- Ex ante real rate: policy rate minus expected inflation

From 2010 to 2020, major economies operated in a structurally negative real rate environment, as documented by long-term series from the Bank for International Settlements. By late 2025, the configuration has reversed entirely: real rates are now approaching, or even exceeding, commonly estimated neutral real rate levels.

In other words: even without nominal rate hikes, monetary policy is exerting restrictive pressure in real terms.

Real policy rates: the invisible tightening

The real rate is calculated as policy rate – inflation. When it turns sustainably positive, the monetary regime becomes restrictive, even without nominal rate hikes.

🟢 negative real rates = support for risk assets · 🔴 positive real rates = pressure on valuations and leverage

A positive real rate regime: a structural break

Financial history confirms it: periods of positive real rates coincide with stricter discipline on balance sheets and valuations. Conversely, major episodes of market exuberance have consistently occurred in environments of very low or negative real rates.

The true inflection point did not occur during the rapid tightening of 2022–2023, but later: when nominal rates stabilized while inflation continued to decline.

This underlying shift explains why valuation models calibrated on the 2010s are now losing relevance.

This constraint weighs particularly heavily on long-duration growth themes, whose value depends largely on distant cash flows. In a positive real rate regime, these assumptions become extremely sensitive to revisions. The analysis of AI thematic ETFs, their flows and hidden risks illustrates how a shift in the monetary regime can widen the gap between technological narratives and actual value creation.

- The reading of the monetary and financial cycle

- The cost of capital and the discipline imposed on leveraged balance sheets

- The hierarchy of valuations across asset classes and sectors

What they do not predict

- A market top or bottom

- The precise timing of monetary policy decisions

- A short-term tactical allocation signal

The market’s blind spot

The dominant narrative assumes that declining inflation will quickly lead to nominal rate cuts sufficient to support risk assets.

But as long as central banks prioritize their anti-inflation credibility, they have every incentive to maintain real rates slightly above neutral. This stance leads to several consequences:

- a persistently higher cost of financing;

- increased pressure on highly leveraged business models;

- a greater need for selectivity in investment decisions.

Concrete implications across asset classes

Bonds and credit

Positive real rates restore the attractiveness of real yields on short-duration bonds, favor higher-quality issuers, and weaken speculative credit profiles.

Equities and risk assets

Sectors with long-duration cash flows are mechanically impacted by higher real discount rates. Conversely, companies generating immediate and recurring revenues tend to be more resilient.

In this environment, the adjustment is not uniform. The strongest companies can still deliver positive surprises despite higher capital costs, while others see margins compress rapidly. Earnings surprises thus become a leading indicator to identify those that can truly withstand a positive real rate regime, well before these pressures appear in macro aggregates.

Real estate and real assets

The shift from negative to positive real rates has already reduced borrowing capacity by 20–30% for many households at equivalent property prices, according to mortgage brokers and housing credit observatories.

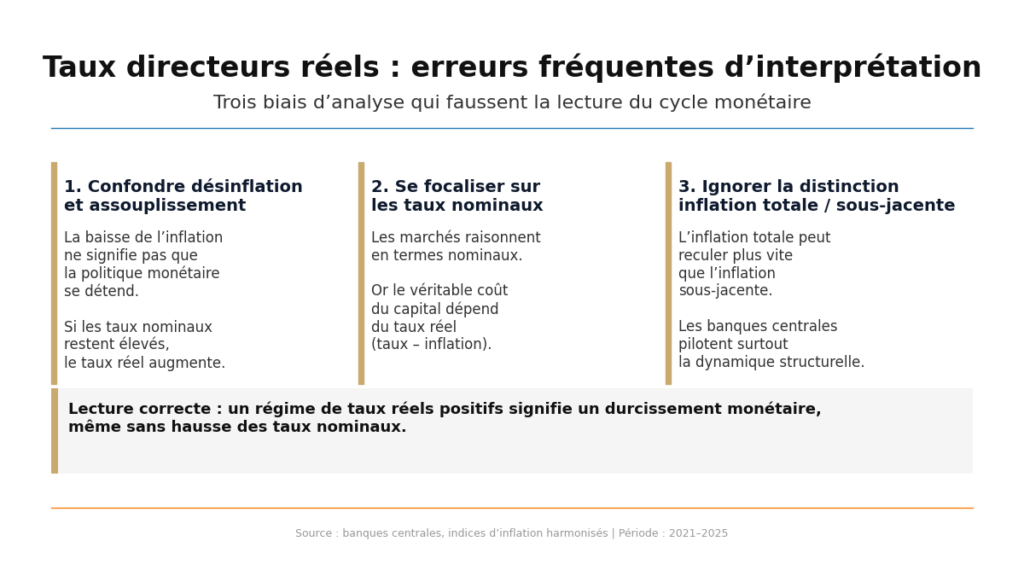

Common interpretation pitfalls to avoid

- Equating disinflation with monetary easing.

- Focusing on nominal rate announcements while ignoring real rates.

- Failing to distinguish between headline and core inflation.

Monetary policy tightens when disinflation pushes real rates higher, even if nominal rates remain unchanged.

Three frameworks to read the current cycle

- Think in terms of real rate regimes, not individual announcements.

- Adopt a 2–3 year horizon rather than focusing on upcoming meetings.

- Differentiate vulnerable sectors from resilient ones.

Conclusion — A discreet but decisive indicator

Real policy rates encapsulate the core of the current monetary stance. As long as they remain sustainably positive, the cost of capital will continue to act as a latent headwind for risk assets.

This regime is neither spectacular nor abrupt, but it shapes investment decisions, sector allocation, and valuation trajectories. Ignoring it is equivalent to navigating the cycle with one key instrument missing.

- Disinflation does not equal monetary easing. When inflation declines faster than nominal rates, monetary constraint intensifies in real terms.

- A positive real rate regime structurally reshapes the cycle. It increases the cost of capital, enforces financial discipline, and penalizes valuations based on distant cash flows.

- Markets are still underestimating this signal. As long as real rates exceed neutral, the dominant risk is not a sudden shock, but a gradual erosion of margins and balance sheet flexibility.

Mis à jour : 20 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.