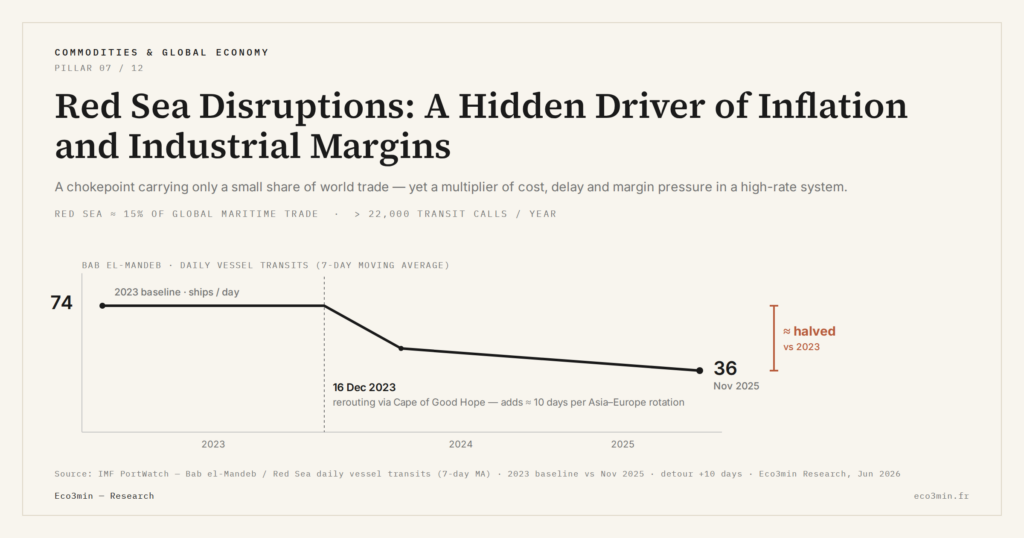

Red Sea Disruptions: A Hidden Driver of Inflation and Industrial Margins

The Bab el-Mandeb Strait is once again becoming a major pressure point in global trade. In an environment of high interest rates and fragile supply chains, a localized maritime disruption can now quickly transmit to industrial margins and inflation.

TL;DR

Since late 2025, Red Sea reroutings via the Cape of Good Hope have fed into industrial margins and inflation because elevated rates leave little cushion to absorb logistics costs.

- Shipping lines introduced Red Sea surcharges of 10–25% on Asia–Europe routes from December 1, 2025; rerouting via the Cape adds 10–14 days to a Shanghai–Rotterdam run and 10–15% to fuel and crew costs per rotation.

- With policy rates between 3% and 4.5% across major advanced economies in early 2026, lengthening inventory turnover from 30 to 45 days consumes roughly 0.3–0.5 points of annual gross margin on affected lines.

- Where 2020–2022 saw Asia–Europe spot rates rise four- to sixfold under near-zero rates, today's positive real rates mean even moderate shocks feed more directly into margins or prices.

- The article frames a possible “latent crisis regime” adding 0.2–0.4 points of annual inflation on selected goods (manufactured, automotive, household equipment) over 2026–2028 versus a normalized environment.

The Bab el-Mandeb Strait is re-emerging as a strategic chokepoint for international trade. Analysis of its implications for inflation, corporate margins, and global supply chain organization.

While the Red Sea accounts for only a limited share of global trade, it nevertheless acts as a multiplier of constraints in an already fragile logistics system.

Red Sea: a vital artery of global trade under pressure

Since late 2025 and into early 2026, the resurgence of attacks on merchant vessels in the Red Sea has driven a sharp increase in maritime insurance premiums and forced part of the shipping industry to reroute via the Cape of Good Hope. This corridor, which handles around 12–15% of global trade and more than 20% of containerized flows between Asia and Europe (2018–2023 consolidated estimates from port authorities), has once again become a critical node in global geoeconomics.

Why it matters: in an economic system already shaped by high interest rates and fragile supply chains, a localized maritime disruption can quickly feed into industrial costs and inflation.

Beyond the immediate security episode, the Red Sea reflects a deeper dynamic: the long-term transformation of trade routes under the combined effects of strategic rivalry, forced regionalization, and rising political risk, within an environment of increased dispersion of performance and fragmented flows. This perspective fits within the broader framework of structural geopolitics, which focuses not on isolated shocks but on persistent reconfigurations of flows, dependencies, and power balances.

To fully grasp the stakes, the Red Sea must be placed within a broader macroeconomic context: global supply chains, the inflationary spiral initiated after 2021, and persistently restrictive monetary policy.

The data cited are drawn from international port statistics, central bank publications, and aggregated estimates from major economic institutions.

What gives this maritime passage its outsized strategic importance is that it concentrates “intermediate” flows (far removed from traditional oil shocks), yet tied to high-leverage products—automotive components, electronics, capital goods—whose absence can halt production across European and Asian industries.

This analysis provides an operational macroeconomic reading of the Red Sea corridor, linking geopolitics, logistics, inflation dynamics, and industrial profitability.

The objective is to show how an apparently secondary geopolitical risk can become a structural driver of prices and real constraints—without requiring a dramatic shock.

The trigger: a measured logistics shock in an already constrained system

Since December 1, 2025, several shipping companies have introduced specific “Red Sea surcharges” ranging from 10% to 25% on Asia–Europe routes, following a more gradual increase throughout 2024. From a macro perspective, this is far from the 2021 Suez Canal disruption, but the context is fundamentally different: policy rates remain elevated (between 3% and 4.5% across major advanced economies in early 2026, based on central bank communications), and industrial margins have already been eroded by rising financing costs since 2022.

Part of the economic consensus believes this Red Sea episode will remain background noise, unlikely to trigger a major inflation shock. This view is based on freight rates still 30–40% below 2021–2022 peaks. Our analysis diverges: what matters is not the absolute level, but the combination of three factors—logistics costs + cost of capital + geopolitical fragmentation.

This accumulation of constraints comes at a particularly sensitive point in the cycle. The persistence of an still-inverted yield curve signals that the system remains under stress even without an imminent recession. In this context, an intermediate logistics shock like the Red Sea acts less as an isolated event and more as a revealer of underlying fragilities.

Why a maritime disruption can become a macroeconomic event

Transmission channels: how a maritime corridor can reignite inflation pressures

The Red Sea corridor operates through three main mechanisms:

- Shipping costs: rerouting a container ship via the Cape of Good Hope adds 10–14 days to a Shanghai–Rotterdam journey, implying a 30–40% increase in transit time and a 10–15% rise in fuel and crew costs per rotation.

- Inventory management: more uncertain delivery times force companies either to increase safety stock (tying up capital) or accept temporary supply disruptions.

- Risk premiums: insurance, private security, and selective rerouting for sensitive goods all contribute to higher average freight costs.

At the micro level, a European industrial firm that previously imported Asian components with a 30-day lead time may now face a logistics cycle of 40–45 days if part of its flows bypass the Red Sea. At unchanged interest rates, this translates into higher working capital needs: more capital tied up in inventory for longer periods.

Assuming an average cost of capital close to 8% in early 2026 for a large industrial firm (risk-free rate around 3–3.5% plus a risk premium), moving from 30 to 45 days of inventory turnover consumes roughly 0.3 to 0.5 percentage points of annual gross margin on affected product lines. While modest in isolation, this adds to the margin compression already observed since 2022.

The real question decision-makers are asking

The core issue is not whether freight rates will rise further, but whether the Red Sea corridor can once again destabilize prices, margins, and physical availability of goods. In other words: should we fear a “mini-2021” logistics shock, or is this a manageable risk without major portfolio or industrial reallocation?

Historical perspective: lessons from 2021 in a radically different monetary environment

Between 2020 and 2022, the surge in container freight rates contributed significantly to global inflation: on some Asia–Europe routes, spot rates increased four- to sixfold. At the same time, central banks maintained near-zero rates, facilitating high inventory levels and capacity investment.

By 2025, the landscape has reversed:

- real interest rates are slightly positive across most advanced economies,

- central banks remain cautious about rate cuts due to core inflation still near 3% in both the eurozone and the US at end-2025,

- logistics balance sheets have been streamlined: lower inventories, tighter flows.

This monetary regime shift is detailed in the broader framework of interest rate policy and monetary transmission. For the Red Sea corridor, the implication is clear: even moderate shocks to delays and costs can no longer be absorbed through cheap financing—they feed more directly into margins or prices.

A less intuitive point: it is not only oil prices that matter in this region, but the fragility of all the “invisible components” of value chains—those inputs whose absence can halt entire production lines.

A risk markets still underestimate

The market consensus expects maritime flows to normalize over the coming years, with freight rates converging toward 2015–2019 levels (adjusted for inflation). This assumption rests on three implicit premises:

- disruptions remain contained and temporary,

- global shipping alliances successfully optimize networks,

- regional powers ensure a baseline level of security.

Yet the gap between forecasts and reality is already visible in corporate earnings. Earnings surprises highlight a growing divergence between firms able to pass through logistics cost increases and those experiencing margin erosion. These micro signals often precede broader revisions in risk expectations.

Our view diverges on a key point: a “latent crisis regime” is more likely than anticipated, where the Red Sea corridor is neither fully disrupted nor fully operational. In such a scenario, shipping companies operate with:

- a portion of their fleet permanently rerouted,

- insurance costs structurally above historical norms,

- greater delivery uncertainty, incompatible with just-in-time production.

If confirmed, the Red Sea becomes a source of structural inflation rather than a temporary shock: not a sharp spike, but an additional 0.2 to 0.4 percentage points of annual inflation on selected categories (manufactured goods, automotive, household equipment) over 2026–2028 compared to a normalized logistics environment.

- Imported inflation pressure on certain manufactured goods

- Industrial margin fragility in a high-rate environment

- Corporate hierarchy based on logistics resilience

What it does not imply

- An immediate global inflation shock

- A logistics crisis comparable to 2021

- A short-term market timing signal

Mapping exposure: shipping, industry, geography

The key for investors and business leaders is identifying where Red Sea risk concentrates within the value chain:

- Shipping companies: in the short term, they benefit from surcharge pass-through, supporting revenues. However, route instability and regulatory pressure limit pricing power over time.

- European and Middle Eastern industrial firms heavily dependent on Asian inputs: automotive, capital goods, consumer electronics, specialty chemicals.

- Strategic transit states: Egypt (Suez Canal), Saudi Arabia, Israel, Yemen; their stability directly determines the corridor’s risk premium.

A less-discussed indicator deserves attention: since mid-2024, valuation gaps have quietly widened between firms heavily reliant on the Red Sea corridor and those shifting toward regional supply chains (Eastern Europe, Mediterranean basin, North America).

Three levers to manage exposure

1. Portfolio calibration

Within a diversified portfolio, a prudent approach is to limit exposure to companies directly dependent on Asia–Europe trade via the Red Sea to 5–10% of the equity allocation, depending on risk tolerance. Within that segment, capping individual positions at 2–3% helps absorb adverse scenarios.

2. Targeted hedging instruments

Advanced investors may deploy hedges via sector indices (transport, European industry) during peak tensions, rather than focusing solely on oil contracts. The goal is to cover both energy and logistics disruption risk.

3. Operational adjustments for companies

- Extend order visibility: move from 1–2 months to 3–4 months planning horizons.

- Supplier diversification: secure at least one alternative source for each critical component.

- Buffer stock adjustment: accept slightly higher inventories for exposed product lines.

Dashboard: key indicators to monitor

- Asia–Europe vs transpacific freight spread

- Transit times (Shanghai–Rotterdam, Singapore–Marseille)

- Shipping and insurance surcharge announcements

- Eurozone producer prices in import-heavy sectors

For non-specialists, the combination of freight rates and transit times provides the most actionable signal. Tracking these monthly helps distinguish between acute crisis, normalization, or a persistently degraded regime.

Common analytical pitfalls

Red Sea risk is not an isolated logistics shock but a macroeconomic amplifier, whose impact depends on the cost of capital and the duration of disruptions.

- Waiting for a “big bang”

- Focusing only on oil prices

- Assuming supply chains adapt without macro consequences

Assuming that the absence of a dramatic disruption means no macroeconomic risk leads to underestimating cumulative effects on margins and inflation.

Three scenarios (12–24 months)

Scenario 1: normalization (consensus)

Incidents remain contained, freight rates normalize, and macro impact stays limited.

Scenario 2: persistent degraded regime

Ongoing disruptions lead to structural logistics adjustments and sustained cost pressures.

Scenario 3: major escalation

A severe disruption temporarily halts flows, triggering simultaneous freight and energy spikes.

How to act depending on your profile

- Investors: diversify and monitor logistics exposure closely.

- Companies: integrate Red Sea risk into 2026–2028 strategic planning.

- Individuals: expect some goods to remain structurally more expensive.

The Red Sea corridor may not trigger a global crisis, but in a world of high rates and fragmented supply chains, it acts as a silent amplifier of economic constraints.

FAQ

Can the Red Sea alone trigger inflation? Unlikely alone, but it can add persistent pressure.

Should maritime stocks be avoided? No, but exposure should remain balanced.

How can SMEs assess exposure? By mapping supply chains and lead times.

Can monetary policy offset this? Partially, but it cannot remove physical constraints.

- 3 key takeaways

- The Red Sea is a structural risk, not a temporary event.

- In a high-rate world, logistics costs have macro impact.

- Investors and firms must treat it as a long-term parameter.

Last updated — 16 June 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…

Diesel versus gasoline: why the two crack spreads diverge

The 3-2-1 crack blends gasoline and distillate into a single number, and that convenience hides something the market…