Saving vs Investing vs Placing: Understanding Risk, Time, and Liquidity

Saving, placing, and investing refer to three distinct financial functions. Understanding their differences in risk, time horizon, and liquidity.

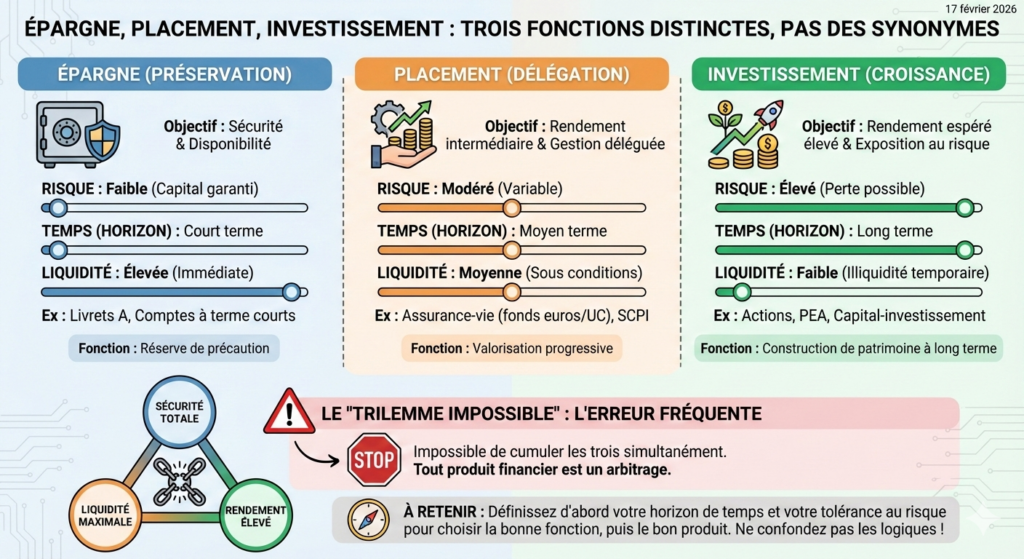

Saving, placing, investing: three verbs often used interchangeably in everyday language, yet they reflect fundamentally different financial logics. Each implies a distinct relationship to risk, time, and liquidity—three dimensions that most individuals never explicitly separate. This confusion is not trivial: it leads to evaluating financial products without understanding the function they are meant to serve. A savings account is not designed to generate returns, just as an equity investment is not meant to preserve capital in the short term. Establishing these distinctions provides a framework before even considering specific financial products.

What most financial product analyses overlook is this: the confusion between these three functions does not only create individual disappointment—it distorts aggregate savings behavior. When millions of households treat a savings account like an investment, or equities as a short-term reserve, capital flows are misallocated toward uses they were not designed for. This structural mismatch carries a collective cost that is rarely measured.

Three functions, three distinct logics

Saving, in its strict sense, fulfills a preservation function. Its objective is to maintain capital that is available, liquid, and nominally stable. Instruments such as regulated savings accounts or short-term time deposits are the most direct expressions: capital is guaranteed in nominal terms, and access is immediate or near-immediate. According to the AMF Savings and Investment Barometer (2025 edition), nearly 60% of French households report not perceiving any functional difference between “placing” and “investing.” This figure highlights the scale of the linguistic bias that blurs these distinctions.

Placing introduces delegation. The term suggests entrusting money to a vehicle or manager, with an implicit expectation of returns higher than pure savings. But this expectation obscures a key reality: any placement carries risk—interest rate risk, market risk, or inflation risk—that the term itself tends to downplay. Understanding what the word “placement” conceals means identifying the gap between perception and the product’s actual function.

Investing, finally, is a deliberate exposure to uncertainty. The investor accepts the possibility of loss in exchange for expected returns. It is the boundary between preservation and exposure that defines the fundamental distinction: saving is about rejecting risk; investing is about accepting it under specific conditions.

Risk, time, liquidity: a structural trilemma

Each financial function is defined by a combination of three variables. Saving prioritizes liquidity and nominal safety, at the cost of low or even negative real returns. Investing accepts temporary illiquidity and the risk of loss in exchange for potentially higher long-term returns. Placing occupies an intermediate zone, often poorly defined, where expectations of return coexist with a tolerance for risk that is rarely made explicit.

The most common trap is trying to achieve all three simultaneously: a product that is liquid, risk-free, and high-performing. This trilemma does not exist. According to Banque de France data (Q3 2025), the household savings rate stood at around 17.5% of gross disposable income—one of the highest in the euro area. Yet a significant share of this savings remains concentrated in capital-guaranteed products, raising a structural question: does this allocation reflect informed choice, or confusion between functions?

The dominant narrative often interprets this concentration as excessive prudence among French households. The reality is more nuanced: it also reflects the absence of a clear framework to distinguish precautionary savings, intermediate placement, and deliberate risk exposure. The issue is not prudence—it is the lack of functional segmentation. Some of this savings could serve an investment function if the distinction were made upfront, but this cannot be assumed without considering each individual situation.

Believing that a product can be liquid, high-performing, and risk-free at the same time. This expectation stems from confusion between financial functions. In practice, every financial product involves trade-offs—it never combines all three. Evaluating a savings account based on its return or an equity portfolio based on its safety means applying the wrong criteria to the wrong function.

Time: the most underestimated variable

The most overlooked dimension in this confusion is time. A two-year horizon does not allow for the same vehicles as a twenty-year horizon. The difference is not merely quantitative—it fundamentally changes the nature of acceptable risk. It is the structuring role of time horizon that explains why the same product can be either appropriate or unsuitable depending on the duration considered.

According to OECD projections published in December 2025, potential growth in advanced economies is expected to remain constrained around 1.5% to 2% per year over the next decade. In this context, the distinction between saving and investing becomes even more critical: capital without a clearly defined function will not benefit from the same compounding effects. And it is precisely the multiplier effect of time that explains why delaying an investment decision has an exponential—not linear—cost.

What this confusion changes in practice

The most widespread illusion concerns returns. Many individuals look for a “good investment” by focusing solely on past performance, without distinguishing the function the product is meant to serve. They project investment expectations onto savings products, or vice versa. This mismatch fuels the illusion of guaranteed returns—a concept that financial theory itself treats as a fragile convention, not a market reality.

According to Eurostat data (2025), euro area households held approximately 35% of their financial assets in deposits and cash—a proportion that has remained stable for a decade, despite several years of negative real interest rates. This aggregate behavior suggests that confusion between functions does not self-correct through market conditions alone.

If this framework were to be invalidated, it would require the emergence of financial products genuinely capable of combining liquidity, safety, and returns—a scenario that neither current market conditions nor regulatory trends make likely. Conversely, a prolonged environment of low real interest rates would further reinforce the need to clearly distinguish these functions in order to understand what each financial vehicle actually delivers.

Confusing saving and investing does not only create individual risk—it distorts capital allocation at the level of an entire economy.

Saving, placing, investing: three functions, three relationships to risk, time, and liquidity. Establishing this framework does not solve decisions—but it prevents making them based on confusion. Multiple paths remain possible depending on macroeconomic, fiscal, and personal contexts. The distinction proposed here is not a decision-making tool—it is a lens, applicable to every concrete choice encountered in everyday financial trade-offs.

- Saving preserves capital in nominal terms; investing exposes it to risk in exchange for expected returns—two distinct functions, not two degrees of the same action.

- The term “placement” obscures risk exposure by suggesting safety, which distorts product evaluation.

- No financial product combines full liquidity, nominal safety, and high returns—this trilemma structures every financial decision.

- Time horizon determines the nature of acceptable risk, not just its magnitude—it is the primary variable to identify.

Mis à jour : 30 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.