The Strong Dollar Regime: Structural Mechanisms and Market Transmission

The US dollar’s persistent strength is not the result of a cyclical exuberance: it reflects a structural reconfiguration of the international monetary order, whose transmission effects — across asset classes, corporations and emerging economies — are reshaping global financial equilibria.

Why the US dollar remains structurally strong in the current cycle

The strong dollar is not a market signal — it is a macro regime whose effects transmit across the financial system.

The structural appreciation of the US dollar rests on a sustained real‑rate differential in favor of the United States, amplified by the dollar’s safe‑haven role in a fractured geopolitical environment. This strong‑dollar regime acts like a prism that distorts relative prices — across asset classes, currencies, commodities and funding costs — with transmission effects that vary by region and sector.

Treating the dollar as a structural variable — not merely a market parameter — changes how we interpret international financial performance, emerging-market financing conditions and allocation tradeoffs. For a global allocator, ignoring the exchange-rate regime is tantamount to flying half-blind. This article examines the structural drivers of the strong dollar, its macro-financial transmission channels, and the implications for international asset allocation, including its direct impact on portfolio construction and performance.

Quarter after quarter, the DXY index has remained above its long‑run averages. The euro underperforms, the yen weakens, and the renminbi struggles to assert itself. This movement is not the product of a one‑off shock — it reflects a structural imbalance rooted in differentials of growth, productivity and monetary policy between the United States and the rest of the world. The IMF (World Economic Outlook, October 2025) estimates the real effective exchange rate of the dollar to be about 15% above its long‑run average — a level comparable to the peaks of 1985 and 2001, but supported this time by stronger macro fundamentals. The BIS (Annual Report, 2025) notes that the 10‑year real‑rate differential between the United States and the euro area is around 150 basis points — a gap that, historically, explains the bulk of EUR/USD variance over a cycle. Several Federal Reserve and IMF studies converge on the view of the dollar as a systemic variable in global financial conditions.

This strong‑dollar regime is part of the broader new financial markets paradigm, characterized by the return of positive real rates and the rehabilitation of the price of capital. The “real cost of money” framework underpins this interpretation.

- The strong dollar rests on a structural real‑rate differential, not on cyclical exuberance

- It transmits across the financial system: international equities, commodities, emerging‑market debt and global funding conditions

- A definitive reversal would require macro conditions that are not present today

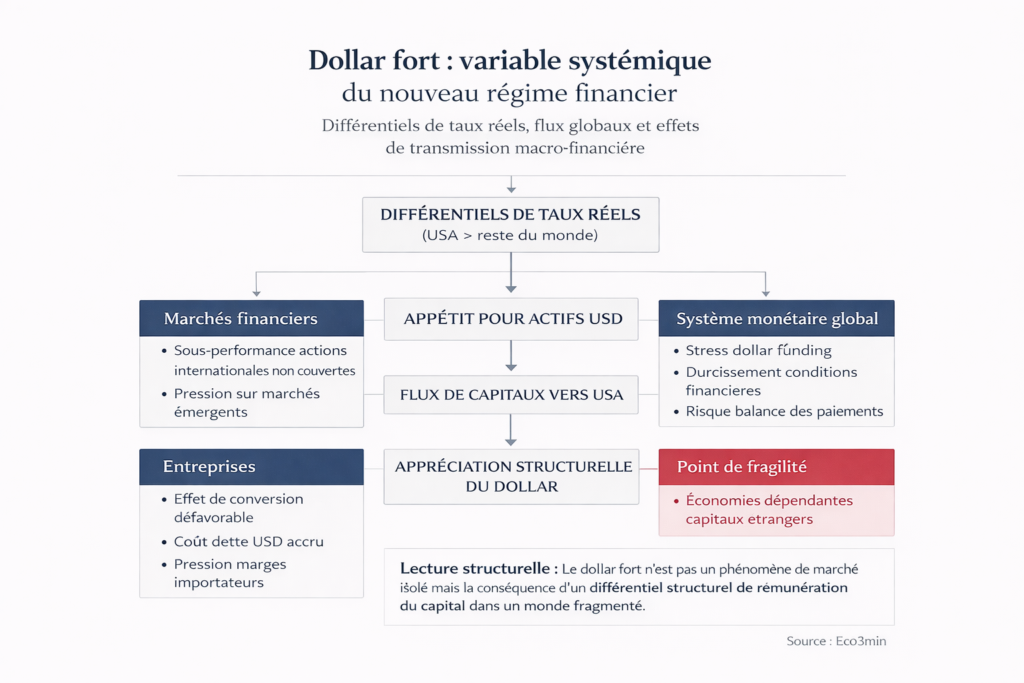

The strong dollar is not a market signal — it is a macro regime whose effects transmit across the financial system. The structural appreciation of the greenback is driven by a durable real‑rate advantage for the United States (~150 bps on 10‑year real rates vs. the euro area), amplified by its safe‑haven function amid geopolitical fragmentation. This regime operates through three transmission channels: the flow channel (reallocation to dollar assets), the funding channel (higher cost of dollar financing outside the United States) and the competitiveness channel (distortion of relative prices). The mechanism is well documented (BIS, IMF, literature on the “dollar smile”); the exact magnitude and duration of this third major strong‑dollar cycle in fifty years remain debated.

Core mechanism: how the strong dollar forms and transmits

The strong dollar does not arise from a single factor but from a combination of reinforcing structural forces — a configuration often described as the “dollar smile” (Jen, 2001): the dollar appreciates in two opposite scenarios (strong US growth or global risk aversion) and only weakens in the intermediate case (synchronized global growth and strong risk appetite).

Favorable real‑rate differential → Capital flows into dollar assets → Appreciation of the effective exchange rate → Higher cost of dollar funding outside the US → Margin compression and pressure on non‑dollar assets

The three channels (flows, funding, competitiveness) operate simultaneously and reinforce one another.

Trigger: the real‑rate differential. The bedrock of a strong dollar is the real‑yield differential between the United States and other large economies. When US real rates exceed those of other major economies, capital flows toward dollar‑denominated assets — bonds, equities, real estate — via a risk‑adjusted yield arbitrage. A seminal BIS working paper (Avdjiev, Du, Koch & Shin, 2019, “The Dollar, Bank Leverage, and Deviations from Covered Interest Parity”) formalizes this mechanism, showing that real‑rate differentials explain most of the variance in international capital flows over a cycle. FRED data indicate the real yield on the 10‑year Treasury (TIPS yield) was around 2% at end‑2025, versus roughly 0% in the euro area and negative in Japan — a gap that structurally attracts international capital to the dollar.

Main transmission channel: capital flows and global reallocation. The rate differential translates into large capital reallocation toward US assets. Treasury International Capital (TIC) data show net capital inflows to the United States of roughly $1 trillion in 2024–2025 — a level that mechanically supports dollar demand and sustains appreciation. This reallocation is not limited to bonds: inflows into US equities, amplified by S&P 500 outperformance and the concentration in mega‑cap technology names, strengthen the loop. Our analysis of US equity structural outperformance documents this flow concentration mechanism.

Amplifier: the dollar‑funding channel. The US dollar occupies a unique position in the international financial system: roughly 60% of global foreign exchange reserves, 50% of international trade invoicing and 65% of externally issued debt by non‑US borrowers are denominated in dollars (IMF, BIS, 2025). This centrality means that a stronger dollar mechanically raises the cost of servicing dollar debt for non‑US borrowers — sovereigns, corporates and financial institutions. The BIS (Quarterly Review, December 2024) estimates the stock of dollar debt held by non‑US borrowers at about $13 trillion — a stock that, combined with exchange‑rate appreciation, exerts cumulative financial pressure on the most exposed economies. This “dollar funding stress” mechanism is the channel through which a strong dollar acts as a de‑facto global monetary tightening, independent of local central‑bank actions.

Macro‑financial consequence: distortion of relative prices. The combination of these channels produces systematic distortions in relative prices worldwide. Commodities, priced largely in dollars, see their real prices compressed — a barrel of oil can rise in dollar terms while becoming cheaper in purchasing‑power terms for non‑dollar importers. International equity returns are mechanically eroded in dollar terms: an investor in dollars sees a European index’s local gains reduced by the euro’s depreciation. Emerging‑market sovereign spreads widen under the pressure of higher dollar funding costs — the IMF (Global Financial Stability Report, October 2025) reports a +0.7 correlation between DXY and EMBI spreads over 2022–2025. This mechanism is central to our analysis of monetary crises and geopolitical challenges.

- DXY: ~15% above its long‑run average (comparable to 1985 and 2001). Source: IMF WEO, October 2025.

- 10‑year real‑rate differential US vs. euro area: ~150 bps end‑2025. Source: BIS, FRED.

- Net capital inflows to the US: ~ $1,000 bn in 2024–2025. Source: TIC System.

- Non‑US dollar‑denominated debt stock: ~ $13,000 bn. Source: BIS, Quarterly Review, December 2024.

- DXY / EMBI correlation: +0.7 over 2022–2025. Source: IMF GFSR, October 2025.

Durable real‑rate differential > 100 bps + sustained positive TIC inflows + stressed emerging‑market spreads → high probability of persistence in the strong‑dollar regime. A reversal requires the simultaneous arrival of three conditions: macro convergence, geopolitical easing, and restored risk appetite.

What the consensus incorporates — and the asymmetry it underestimates

The prevailing view among currency strategists and major-bank outlooks expects a gradual dollar weakening over a 12–18 month horizon based on monetary‑policy convergence (the Fed easing faster than the ECB). This scenario is not without foundation — the rate differential is indeed the dominant explanatory variable over a cycle.

Its limitation is the underestimation of the structural asymmetry of the “dollar smile.” The dollar only weakens durably in a very specific configuration: synchronized global growth, elevated risk appetite, and credible convergence of macro fundamentals. These three conditions are not present in 2025–2026: growth remains desynchronized (US > euro area > China), geopolitical tensions sustain a safe‑haven premium, and any nascent convergence in real rates is modest. The BIS (Annual Report, 2025) reminds us that the previous two strong‑dollar cycles (1980–1985, 1995–2001) lasted 5–7 years — and that reversals occurred only after a full regime change, not after a simple policy adjustment.

The consensus is therefore correct to anticipate a dollar peak, but may conflate tactical adjustment and structural regime change. A 3–5% DXY pullback — compatible with a moderate narrowing of the rate differential — does not invalidate the strong‑dollar regime. Only the joint realization of the three structural conditions would signal a genuine regime reversal.

Confusing a tactical dollar correction (a 3–5% DXY retracement due to rate differential narrowing) with a regime reversal. Both previous strong‑dollar cycles lasted 5–7 years and reversed only after a comprehensive change in the global macro environment — not after a Fed pivot alone. Any structurally short dollar position requires a global convergence scenario that is weakly supported by current data.

| View: “the dollar has peaked” | View: structural regime | |

|---|---|---|

| Core assumption | Rate convergence weakens the dollar | Real‑rate differential narrows but does not vanish; the regime persists |

| Signal invoked | Fed pivot, lower US rates | Desynchronized growth, safe‑haven premium, persistent dollar‑funding stress |

| Historical precedent | 1985 (Plaza Accord), 2002 (post‑bubble reversal) | 5–7 year cycles; reversal only after full regime change |

| Main risk | Missing the reversal if convergence happens fast | Underestimating regime duration and transmission magnitude |

| Key variable | Nominal rate differential, Fed forward guidance | Real‑rate differential, TIC flows, real DXY, EMBI spreads |

Differentiated transmission: why the strong dollar affects actors unevenly

The strong‑dollar regime does not produce uniform effects: transmission is highly asymmetric across asset classes, sectors and geographies.

International equities: mechanical erosion of returns. For a dollar‑based investor, foreign market returns are mechanically reduced by local currency depreciation. A Euro Stoxx 50 rising 10% loses half its performance if the euro falls 5% versus the dollar. This conversion channel explains part of US equity outperformance since 2022 — a dynamic amplified by the documented reallocation flows in our US equity outperformance analysis. The decision to hedge currency exposure is therefore a first‑order performance choice — and its cost depends on the rate differential (hedging becomes more expensive when US rates are higher).

Commodities: compression of real prices. Commodities, priced mainly in dollars, suffer a twofold impact. Dollar appreciation compresses their real price for non‑dollar buyers, reducing demand. At the same time, higher real rates increase carry costs for inventory financing, reducing incentives to hold stock. The result is downward pressure on commodity real prices — a mechanism supported by the World Bank (Commodity Markets Outlook, 2025), which finds a -0.5 correlation between DXY and a non‑energy commodity price index over 2000–2025.

Emerging markets: imported financial tightening. The dollar‑funding channel is the most powerful transmission vector to emerging economies. A stronger dollar raises the servicing cost of dollar debt (the $13 trillion stock), triggers capital outflows (investors repatriate to dollar assets), and forces local central banks to maintain higher rates to defend their currencies — even where domestic conditions would allow easing. The IMF (GFSR, October 2025) documents these “monetary spillovers” and estimates that dollar appreciation is equivalent to a 50–100 bps tightening for the most exposed emerging economies. The role of certain safe‑haven currencies as potential shock absorbers is examined in our yen as a safe haven piece.

Corporates: highly asymmetric effects. For firms, the impact depends on their position in global value chains. European exporters gain short‑term price competitiveness but face greater currency volatility exposure. US multinationals see foreign revenues reduced through translation effects — the BEA estimates that over 40% of S&P 500 revenues come from abroad. Import‑heavy sectors (energy, electronic components) face margin compression. Non‑US borrowers with dollar debt confront mechanically higher financing costs. Managing FX risk thus becomes a strategic priority beyond classical treasury operations.

Implications for reading the current cycle

For asset allocation. The strong‑dollar regime makes currency decisions a first‑order performance determinant — often more decisive than market or sector selection. Allocation between dollar and non‑dollar assets and the associated hedging policy account for a substantial share of total return. This perspective informs our work on an asset allocation adapted to the new regime.

For reading global monetary policy. The strong dollar acts as a transmission channel for US monetary policy to the rest of the world — an “exported” tightening that constrains non‑US central banks. This mechanism interacts with the delayed effects of restrictive monetary policy to produce a double tightening for the most exposed economies: local restrictive policies stack with imported tightening via the dollar. Cycle desynchronization amplifies this pressure.

For global financial stability. The $13 trillion stock of non‑US dollar debt is a systemic vulnerability whose intensity is directly proportional to the exchange‑rate level. A confidence shock in a sizable emerging economy — comparable to the 1997 Asian crisis or Turkey 2018 — could trigger a feedback loop: capital outflows → local currency depreciation → higher dollar debt burden → sovereign credit deterioration → further outflows. This contagion dynamic is analyzed in our monetary crisis and geopolitical risks framework.

Invalidation condition. This analytical framework loses relevance if the real‑rate differential narrows materially (convergence below ~50 bps), if synchronized global growth restores risk appetite, or if major geopolitical easing reduces the safe‑haven premium. A coordinated currency agreement (a modern Plaza Accord) would also catalyze a reversal — though such an outcome appears politically unlikely today. Conversely, geopolitical escalation, an energy shock, or an asymmetric global recession (sparing the US) would amplify the strong‑dollar regime and its transmission effects.

Three horizons to monitor the dollar regime

Short horizon (0–6 months): the real‑rate differential remains the dominant factor. Watch the 10‑year real‑rate gap US vs. euro area/Japan, TIC flows (capital in/out), speculative dollar positioning (CFTC data), and EMBI spreads as an indicator of emerging‑market funding stress. Short‑term risk is further dollar strengthening if Fed easing expectations are pushed out.

Cycle horizon (1–3 years): the structural question is the pace of convergence of macro fundamentals. If the euro area and China regain credible growth momentum, the real‑rate gap will narrow and the dollar will weaken gradually — the consensus central scenario. If desynchronization persists, the strong‑dollar regime will continue with cumulative transmission effects. Interaction with the real economic cycle determines this trajectory.

Structural horizon (5+ years): the current cycle raises long‑term questions about the dollar’s reserve status. De‑dollarization efforts (reserve diversification, alternative payment systems, renminbi internationalization) are documented but remain marginal relative to the dollar’s structural weight. The BIS (2025) notes the dollar’s share of global FX reserves fell from 71% in 2000 to 59% in 2025 — a real but gradual erosion that does not threaten the dollar’s centrality over a cycle. A credible alternative would require market depth, legal frameworks and institutional stability that neither the euro nor the renminbi fully provide today.

The strong dollar is a macro regime based on a structural real‑rate differential, amplified by safe‑haven demand and the dollar’s centrality in global finance. It functions as a de‑facto global tightening, raising the cost of financing for $13 trillion of non‑US dollar debt and distorting relative prices worldwide. While consensus expects a peak, it may conflate tactical retracement with structural reversal: historical cycles lasted 5–7 years. Treating the dollar as a structural variable — not as a reaction to single Fed decisions — is essential for serious analysis of international financial performance.

Robust: The link between real‑rate differentials and exchange‑rates is well documented (BIS, Avdjiev et al., 2019). The dollar‑funding stress mechanism for non‑US borrowers is formalized by the BIS and confirmed by flow data. Historical durations of strong‑dollar cycles (5–7 years) are empirically observed. The dollar’s effect on commodity prices and emerging‑market spreads is visible in contemporary data.

Uncertain: The exact timing of the dollar cycle peak is inherently unpredictable. Emerging economies’ capacity to absorb stress depends on local factors (reserves, exchange‑rate regime, debt structure) that vary widely. The long‑term impact of de‑dollarization on the dollar’s status remains debated. The prospect of a coordinated currency policy agreement remains speculative.

Our weekly macro bulletin (weekly macro note) confronts this framework with the latest rates, flow and international financial‑condition data. Reading the dollar through its structural mechanisms — real‑rate differentials, centrality in global funding, and safe‑haven demand — offers a sturdier framework than reacting to isolated Fed moves for anticipating the exchange‑rate regime and its transmission effects.

- The strong dollar is a macro regime rooted in a structural real‑rate differential (~150 bps vs. euro area), amplified by safe‑haven demand and the dollar’s centrality in global funding.

- It transmits through three simultaneous channels: capital flows (reallocation to dollar assets), funding (higher cost on $13 trillion of non‑US dollar debt) and competitiveness (distortion of commodity prices and equity returns).

- The consensus expects a dollar peak, but prior strong‑dollar cycles lasted 5–7 years — a structural reversal requires synchronized growth, geopolitical easing and macro convergence, conditions not present today.

- The strong dollar functions as a de‑facto global tightening, exporting US financial conditions and increasing the vulnerability of emerging markets.

- This framework is invalidated if the real‑rate differential narrows materially, if synchronized global growth restores risk appetite, or if a coordinated currency agreement is enacted.

Mis à jour : 31 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.