AI-Themed ETFs: Hidden Concentration Risk in a Positive Real Rate Regime

This analysis breaks down AI-themed ETFs beyond the purely technological angle, by crossing flow dynamics, index architecture, and the macroeconomic environment.

The point here is not to assess AI’s transformative potential, but to clarify the actual distribution of risk within allocations through these vehicles and the behavior gaps they can exhibit versus a traditional equity exposure.

TL;DR

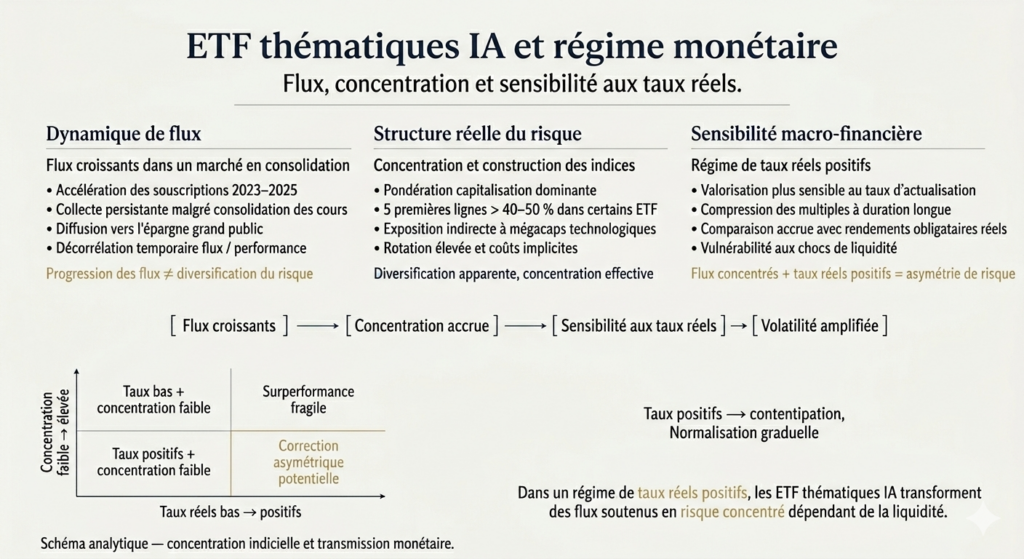

AI-themed ETF assets climbed from roughly $60bn in Q1 2023 to $180-200bn by summer 2025, and in a positive real-rate regime those sustained inflows turn into concentrated risk.

- Net subscriptions of $15-20bn flowed into a handful of flagship products between September and November 2025, even as several AI indices had already corrected 10-15% from their highs.

- The most concentrated AI ETFs hold 20 to 40 names with the top 5 often above 40%, so flows that keep rising without broadening the basket make the risk increasingly asymmetric.

- Q3 2025 results showed AI-related revenue growth slowing to +18-25% year over year, down from +35-45% in 2023-2024, while AI ETFs kept drawing inflows and broad equity ETFs faced waves of redemptions.

- 10-year real rates are positive across most major economies, unlike in 2010-2020, so the multiple expansion of 2023 to early 2024 is no longer automatic and value creation now depends on profit growth rather than narrative.

AI-themed ETFs: a segment under growing pressure

Since the beginning of summer 2025, assets under management in the main AI-themed ETFs listed in the United States and Europe have reached roughly $180 billion to $200 billion, versus barely $60 billion in the first quarter of 2023. Net subscriptions accelerated again between September and November 2025, with roughly $15 billion to $20 billion captured by a handful of flagship products, even as several AI indices had already corrected by 10% to 15% from their highs.

That divergence between capital inflows and price consolidation characterizes the maturation phase of a market narrative: the theme has become established, but its diffusion into retail savings continues. To understand the stakes, it is useful to place this segment within the broader framework of equity and ETF fundamentals before examining its specific features.

This dynamic illustrates a broader phenomenon of increasing rigidity in market behavior, where index and thematic flows tend to reinforce existing trends rather than correct them. This mechanism is explored in the case study on rigidification of behavior driven by financial innovation, which shows how certain products can amplify risk asymmetries.

The critical issue for AI-themed ETFs no longer lies solely in the sector’s explosive growth, but in the way a handful of indices now direct capital allocation on a global scale.

This mechanism cannot be understood without factoring in the decisive role of real policy rates. In an environment where real rates remain positive, long-duration growth assets — a hallmark of AI themes — become much more vulnerable to any revision in liquidity conditions or macroeconomic expectations.

To go deeper into how AI exposure can be structured through ETFs, a detailed analysis of the different possible approaches — concentration, diversification, weighting, and portfolio placement — is developed in the article on AI ETFs and the associated investment strategies.

In this context, some valuation indicators commonly used in tech, such as ARR or recurring growth metrics, become less reliable when interpreted outside the prevailing monetary regime. The limits of these indicators in a positive real-rate environment are detailed in the analysis devoted to ARR and its valuation biases in technology.

The decisive point to watch is not the absolute volume of flows, but their progression while the concentration of risk keeps rising.

AI-themed ETFs: when flows mask risk concentration

Flows into AI ETFs continued to rise in late 2025, even as concentration in a few key names reached historically elevated levels.

⚠️ The more flows grow without broadening the underlying basket, the more asymmetric the risk becomes.

- Confusing marketing narrative with actual exposure: the “AI” label often hides an overrepresentation of generic tech names.

- Extending 2023–2024 performance without accounting for the new regime of positive real rates, which leads to overestimating the capacity of multiples to keep expanding.

- Underestimating real concentration: an ETF may hold many names while still being dependent on 5 dominant stocks.

Recent trigger: record inflows despite slowing leaders

Between August and November 2025, several Nasdaq-listed AI giants reported more nuanced results: slower cloud AI growth, surging capital expenditures, and pressure on margins. Third-quarter 2025 releases pointed to AI-related revenue growth of only +18% to +25% year over year, versus +35% to +45% in 2023–2024.

At the same time, consolidated AUM data show that AI-themed ETFs continued to record positive flows almost every week since July 2025, while broad equity ETFs went through several waves of redemptions. In other words, the AI theme continues to attract capital, sometimes at the expense of more diversified indices.

A segment of the consensus still sees these flows as a simple extension of the technology cycle. Yet a closer look at index weights and construction rules reveals a more structural risk: extreme concentration in a few stocks and heightened sensitivity to monetary policy.

This framework is increasingly challenged by microeconomic data. Earnings surprises published by several AI leaders reflect a growing dispersion between companies able to turn their investments into recurring profits and those whose growth still relies heavily on massive capex and delayed monetization.

in 2025

The anatomy of AI-themed ETFs: what is hiding under the hood

AI-themed ETFs are generally built around proprietary indices that select:

- direct providers of AI technologies (semiconductors, GPUs, cloud infrastructure);

- software platforms and services integrating generative AI;

- companies presented as “beneficiaries” of AI (healthcare, industrials, finance, cybersecurity).

In practice, three parameters shape the risk profile:

- The weighting method (market-cap weighted, equal-weighted, capped weighting), which determines how concentrated the bets are.

- Theme purity: strictly “AI” index or a broader “tech + AI” basket.

- Index turnover, often high, which creates implicit costs (trading costs, market impact).

When long-term real rates rise, as has been the case since mid-2024 in most advanced economies, long-duration growth stocks (with a high share of future cash flows) become more sensitive to changes in the discount rate. AI-themed ETFs, which are highly concentrated in these profiles, amplify this sensitivity.

What many investors are trying to determine is whether AI-themed ETFs are simply a vehicle for exposure to a structural trend or a disguised lever on the most speculative part of the equity market. The case is built out in the analysis of strong dollar transmission to global markets. The answer depends less on the technology itself than on how these products distribute risk: the more concentrated the exposure to 5 to 10 names, the more the ETF behaves like a targeted bet, even if the marketing emphasizes “sector diversification.”

Macro decoding: the decisive role of rates and liquidity

Between 2022 and the end of 2023, central banks raised policy rates by several hundred basis points. In the euro area, the deposit rate rose from -0.5% to roughly 4% in autumn 2023 before gradually easing to around 3% by mid-2025. In the United States, the fed funds rate peaked in a range of roughly 5% to 5.5% before the first gradual cuts in 2025.

This configuration sits within a still-unstable monetary cycle, marked by a yield curve that remained inverted for a long time. As long as that inversion is not resolved in an orderly manner, the most concentrated and liquidity-dependent segments — such as AI-themed ETFs — will remain exposed to abrupt valuation adjustments.

What the signal from AI-themed ETFs changes

- The assessment of equity risk in concentrated growth segments

- Portfolio sensitivity to real rates and global liquidity

- The trade-off between broad tech exposure and targeted thematic bets

What it does not allow us to conclude

- That AI is a bubble or that it will not generate economic value

- That AI ETFs should be systematically avoided

- That they provide a reliable short-term timing signal

Even though headline inflation has fallen sharply from its 2022 peak, 10-year real rates remain positive in most major economies, which was not the case between 2010 and 2020. That configuration is fundamentally reshaping the valuation of growth stocks:

- acceptable price-to-earnings multiples are mechanically lower when real rates are positive;

- the required risk premium increases for the most volatile segments;

- flows are compared more directly with real bond yields.

For AI-themed ETFs, this means that the expansion phase in multiples seen in 2023 to early 2024 is no longer necessarily repeatable if real rates stabilize at an elevated level. Value creation will then need to come from actual profit growth, not from the narrative alone.

What valuations are only partially pricing in

An element markets still seem to be only partly incorporating: the delayed impact of AI on margins outside the pure tech sector. A portion of productivity gains could benefit end users more than infrastructure providers or flagship software companies. If that hypothesis is confirmed, some AI-themed ETFs that are too concentrated on the “upstream” part of the AI value chain could underperform broader indices.

This potential redistribution of value echoes the changes taking place in finance itself, where AI is already modifying cost structures, margins, and risk profiles. These developments are analyzed in the article on financial AI as a new regime of margins and allocations, which highlights the links between technological innovation and real economic constraints.

Concentrated AI ETFs versus diversified AI ETFs: radically different profiles

To avoid confusion, it is useful to distinguish between two families:

- Highly concentrated AI ETFs: 20 to 40 holdings, heavy weighting of the top 5 names (>40%), strong exposure to semiconductors and cloud.

- Broad AI exposure ETFs: 60 to 150 holdings, inclusion of user sectors (healthcare, industrials, finance), more balanced weighting.

The first behave like a near-direct proxy for the cycle of mega-cap tech and data center spending. AI datacenter power demand traces this dynamic. The second capture the gradual spread of AI through the real economy, with greater sensitivity to macro cycles (corporate investment, financing costs, regulation). A full breakdown is given in the exposure routes to AI, from chips to indices.

The dominant forecasts often assume a lasting outperformance by the purest AI ETFs. A more nuanced reading suggests that the sectoral diffusion of AI could, over the medium term, make baskets combining providers and adopters of the technology more attractive, even if they are less spectacular in the short term.

The classic pitfalls in analyzing AI-themed ETFs

- Confusing the sales pitch with actual exposure: the ETF name may emphasize “AI” or “robotics,” while a significant share of the assets is invested in generic tech stocks. Only a detailed look at the holdings can reveal the true exposure level.

- Extrapolating past performance: extending 2023–2024 gains without accounting for the new regime of positive real rates leads to overestimating the capacity of multiples to keep expanding.

- Underestimating concentration risk: an ETF can list 80 holdings and still remain highly dependent on 5 names. Relying only on the number of holdings masks the real risk.

Key indicators to monitor risk in AI-themed ETFs

To keep the analysis rigorous, a few indicators deserve close attention:

- 10-year real rates (United States, euro area): they define the overall valuation framework for growth assets. A rapid rise would be a stress signal for AI ETFs.

- Weight of the top 5 holdings in the ETF: above 40% to 45%, dependency on a handful of names becomes significant.

- Trend in AI capex announced by the major platforms

- Weekly flows into the main AI ETFs: continued inflows despite prolonged underperformance would signal excess confidence.

These indicators complement a broader view of financial innovation dynamics and their diffusion into portfolios.

Practical rules for sizing an AI exposure

To keep the framework readable, a simple rule is to treat AI-themed ETFs as a growth satellite around a more diversified portfolio core. As a purely illustrative benchmark, a “60/30/10” framework can be used: 60% broad exposures (global or regional indices), 30% more targeted segments (sectors, factors), and no more than 10% to pointed themes, including AI.

This rule is obviously not universal, but it reminds us that AI-themed ETFs belong more to the “opportunity/innovation” sleeve than to the structural core of a portfolio. Another useful principle is to limit a given theme (for example, concentrated AI ETFs) to a fraction of that sleeve rather than allocating the entire discretionary risk budget to it.

Three credible scenarios for AI-themed ETFs

1. Gradual normalization of valuations

In this scenario, AI-related earnings growth remains robust but slows, while real rates stabilize at a moderately positive plateau. Multiples decline gradually, performance diverges by sub-sector, and the more diversified ETFs (providers + adopters) hold up better. This scenario assumes no abrupt rate shock and a gradual AI regulatory framework.

2. Run-up followed by a severe correction

In this hypothesis, flows continue to pour into AI ETFs despite a more pronounced slowdown in results. Valuations reach levels that break away from historical tech averages before a sharp reset triggered by a monetary surprise or a profit shock. The most concentrated vehicles then suffer a deeper correction than broad indices.

3. Successful diffusion of AI into the real economy

This scenario focuses on the rise of AI end users: industrials, healthcare, and services. Value creation gradually moves along the chain, and thematic ETFs that combine providers and adopters benefit from a smoother profile. Broad equity indices also capture a significant share of this dynamic, reducing the specific advantage of ultra-thematic ETFs.

This is not necessarily the central market scenario at this stage, but it deserves special attention because it challenges the idea that exposure to “pure-play” AI names is the only relevant option over the medium term.

Counterarguments and invalidation factors

Several elements could disrupt these scenarios:

- a faster-than-expected easing in rates, which would give growth stocks more breathing room and extend the multiple expansion phase;

- an unexpected acceleration in generative AI revenues, for example through new business models more profitable than those seen in 2023–2024;

- conversely, a sharp regulatory tightening on AI in major jurisdictions, which would reduce monetization prospects and weigh on the entire theme.

These elements show how deeply AI-themed ETFs remain embedded in the broader framework of monetary policy and rate regimes, but also in the regulatory choices surrounding the technology. Related work: the grid of bond categories against the rate regime.

In a positive real-rate regime, AI-themed ETFs turn sustained flows into concentrated risk, amplifying valuation sensitivity to liquidity conditions.

Implications for investors, companies, and individuals

For institutional investors, the central issue is to treat AI-themed ETFs as a targeted exposure tool, not as a substitute for a broad index. Regularly tracking the weight of the top 5 holdings and the direction of capital flows can help identify phases of euphoria or disengagement.

For companies, the rise of AI ETFs is changing shareholder structure: a growing share of capital now comes from thematic index vehicles, which are more sensitive to narratives than to individual earnings trajectories. Understanding that logic may influence how firms communicate about AI projects and associated capex.

For individual investors, the key question is not whether AI will transform the economy — the signals are already visible — but how to integrate the theme into a coherent wealth architecture: limit the weight of thematic products, accept the associated volatility, and monitor a few structural indicators rather than past performance alone.

Ultimately, the risk in AI-themed ETFs is less visible than in other more heavily publicized segments, which makes them all the easier to overweight without realizing it. That is precisely why they should be analyzed separately, in relation to the broader framework of global financial markets. The data behind it is compiled in Eco3min’s mapping of regime-driven correlation changes. Related material: our analysis of how financial markets form expectations and price risk.

Frequently asked questions about AI-themed ETFs

Do AI-themed ETFs duplicate exposure already held through a Nasdaq ETF?

Often yes, at least partly, because the major AI names are also heavily represented in broader technology indices. The degree of overlap depends on the concentration level of the AI ETF and the weighting of mega-caps in its composition. Our analysis of artificial intelligence ETFs walks through the underlying drivers.

How can you tell whether an AI ETF is too concentrated in a few names?

A simple indicator is the combined weight of the top 5 holdings. Concentration above roughly 40% to 45% signals strong dependence on a small number of names, even if the ETF holds many stocks.

Do AI ETFs really capture the productivity generated by AI in the real economy?

Not systematically. Products focused on the upstream technology layer mainly benefit from the initial investment phase. If productivity gains spread widely, more diversified indices or ETFs combining providers and adopters may better reflect that value creation.

Which indicator should be watched to know whether the AI theme is “too expensive”?

Beyond earnings multiples, the combination of long-term real rates + expected growth in AI-related earnings is decisive. A widening gap between multiples and profit growth may suggest that the narrative is overtaking the fundamentals.

- AI-themed ETFs are concentrating more and more capital even as earnings growth normalizes and real rates remain positive.

- The main risk does not lie in AI technology itself, but in the concentration of indices and their greater sensitivity to the monetary cycle.

- Treating AI ETFs as a limited innovation sleeve, managed through a few simple KPIs, makes it possible to benefit from the theme without making it the core of the portfolio.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…