Financial Education: The Right Sequence for Personal Wealth Decisions

In personal finance, losses rarely come from a bad decision in itself—but from a correct decision made at the wrong time or in the wrong context. Financial education is fundamentally about sequencing, not knowledge.

How to Avoid the Most Costly Financial Mistakes—Even When You’re Well Informed

The real financial risk is not choosing poorly—it’s choosing in the wrong order.

Financial education is typically framed as a catalog of tools: save regularly, diversify, invest for the long term. This view misses the essential point. In real-life wealth trajectories, fragility rarely stems from a single bad choice, but from an incoherent sequence of choices—individually rational decisions whose combination over time creates vulnerability.

The key is not knowing what to do—it’s knowing when to do it. The same financial product can strengthen or weaken a household’s financial position depending on where it appears in the trajectory. This time dimension—decision sequencing—remains the neglected core of financial education, even though it is its operational heart. This article proposes a practical and accessible framework to structure financial decisions in the right order.

The figures are telling. According to household financial literacy surveys (INSEE, ECB, OECD, 2024–2025), more than 70% of households believe they understand the fundamentals of day-to-day financial management. Yet vulnerabilities persist: excessive reliance on consumer credit, insufficient emergency savings, and poorly calibrated risk-taking. Consolidated euro area banking data show that in 2025, nearly 40% of retail financial product subscriptions involved risk-bearing instruments, while median liquid savings covered less than three months of recurring expenses. This paradox suggests the issue goes beyond access to information: it is not about knowing, but about prioritizing.

This analysis fits within a broader reflection on the interaction between individual decisions and the macroeconomic environment, developed in the analysis of real interest rates and their asset implications. Household financial decisions never occur in a vacuum: they are embedded in regimes of interest rates, growth, and volatility that radically alter their relevance over time.

- 70% of households believe they understand financial fundamentals, yet 40% invest in risky products with less than three months of emergency savings

- Wealth losses more often result from poor sequencing than from isolated bad choices

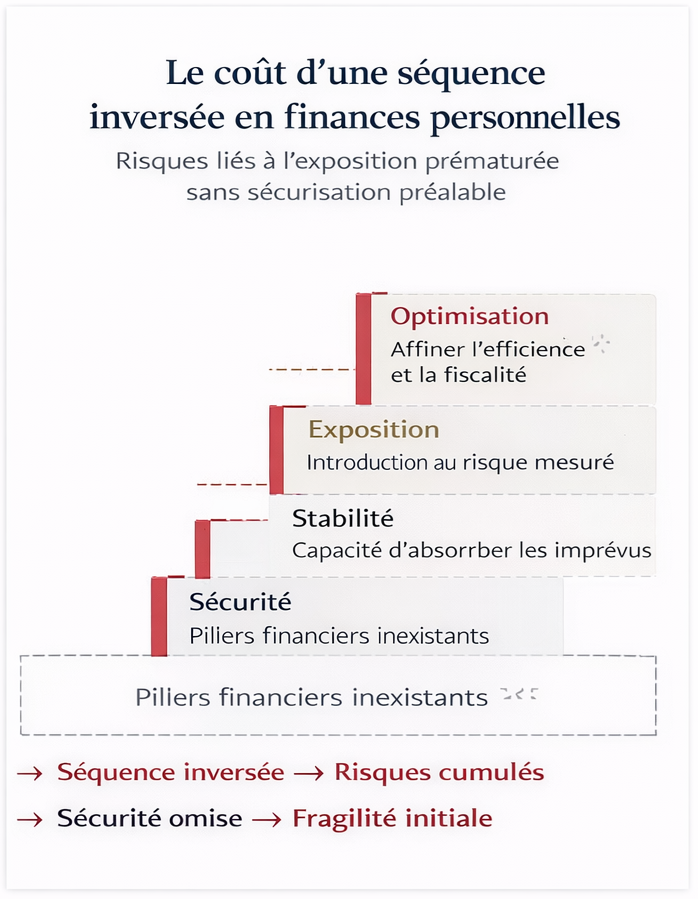

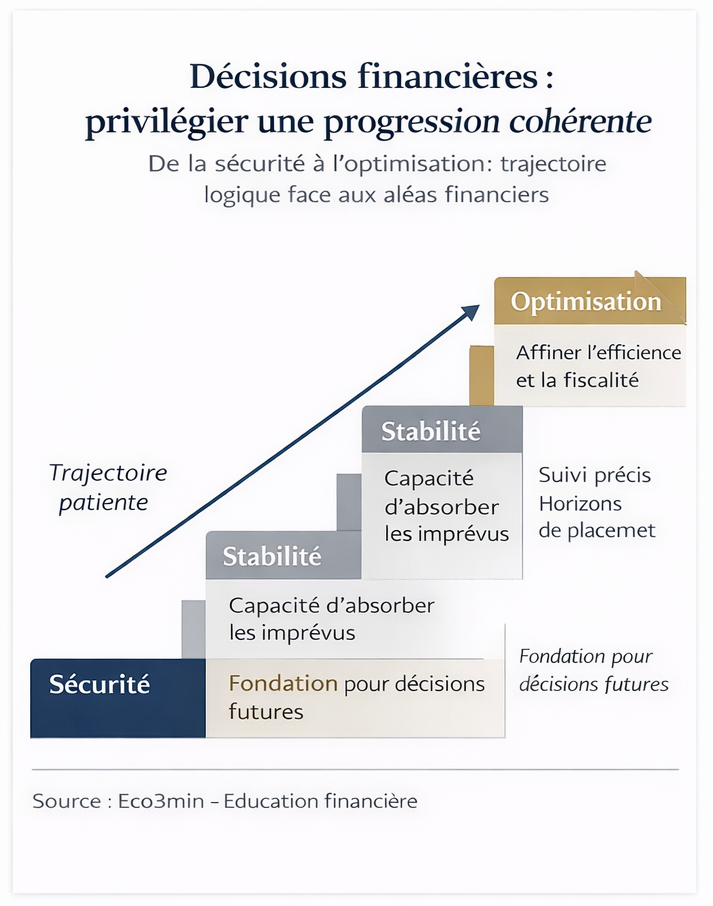

- The structuring sequence: safety → stability → exposure → optimization. Reversing this order creates cumulative fragility

The real financial risk is not choosing poorly—it’s choosing in the wrong order. Financial education as commonly practiced focuses on instruments (what to buy, which product to choose). The determining factor of financial resilience is decision sequencing: first secure (emergency savings), then stabilize (manageable debt, stable income), then gain exposure (long-term investment), then optimize (tax efficiency, fine allocation). Reversing this order—investing before securing, borrowing before stabilizing—creates cumulative fragilities that surface during shocks. This sequencing framework is cycle-independent, but the current environment (high rates, weak growth, persistent inflation) amplifies its consequences: timing mistakes are more costly when margins for error are compressed.

The Core Mechanism: Why Decision Order Creates (or Destroys) Wealth Value

Wealth sequencing is not an abstract theory: it is a concrete mechanism whose effects compound over time and become visible during shocks.

1. Safety (emergency savings: 3–6 months of expenses) → 2. Stability (manageable debt, durable income) → 3. Exposure (long-term investment, real estate) → 4. Optimization (tax efficiency, fine allocation, private equity)

Each step serves a function that protects the next. Skipping a step creates invisible fragility—until a shock reveals it.

Step 1 — Safety: the invisible foundation. Financial safety—readily available emergency savings and coverage of major risks (insurance, health plans)—is the first shield against short-term shocks. It generates little financial return, but preserves something more valuable: the ability to avoid making financial decisions under pressure. A household losing its job with six months of expenses in liquid savings has time to find new employment without being forced to sell investments at a loss or take on emergency debt. A household in the same situation without emergency savings is forced to react—and every urgent reaction destroys value. This protective function gives emergency savings its value—not its 2.4% yield.

Step 2 — Stability: absorbing volatility. Stability allows moderate volatility to be absorbed without disrupting overall balance. Concretely, this means: a manageable debt ratio (France’s HCSF caps debt-service ratios at 35% of income, but comfort lies closer to 25–30%), sufficiently durable income to meet recurring commitments, and a debt structure compatible with repayment capacity even if income temporarily declines. A fixed-rate mortgage provides stability; variable-rate consumer credit reduces it. Stability is not spectacular—but it is what enables households to withstand cycle fluctuations without dismantling the rest of their financial structure.

Step 3 — Exposure: linking to the real economy. Exposure connects households to economic dynamics and financial markets. This is where equity investments (e.g., diversified ETFs), rental real estate, and unit-linked life insurance come into play. Exposure only works if the first two steps are in place: without safety (emergency savings), even minor shocks force loss-making sales; without stability (manageable debt), the ability to maintain exposure over time is compromised. Dalbar data (QAIB, 2025) show the average equity fund investor captures about 6.5% annual returns versus 10% for the S&P 500—a 3.5-point gap largely attributable to timing errors (selling at cycle lows, buying at highs). The lack of prior safety buffers is a key cause of these forced sales. The investment discipline analysis details this mechanism.

Step 4 — Optimization: refining a solid structure. Optimization improves the efficiency of an already well-structured setup: tax optimization (PEA accounts, life insurance wrappers, tax-incentive schemes), fine asset allocation, and introduction of less liquid instruments (private equity, real estate funds, timberland). This step only makes sense if the first three are in place. Optimizing taxes on a portfolio without sufficient emergency savings is like painting the walls of a house whose foundations are unfinished.

- 40% of retail financial product subscriptions in the euro area involve risk-bearing instruments, while median liquid savings cover less than 3 months of expenses. Source: consolidated euro area banking data, 2025.

- Behavior gap: 3.5 annual percentage points lost by the average investor, mainly due to selling at cycle lows linked to insufficient safety buffers. Source: Dalbar QAIB, 2025.

- Average debt-service ratio: households buying property in 2025 devote 33% of income to loan repayment on average, versus 27% in 2019. Source: Crédit Logement Observatory, Q3 2025.

- Core inflation: ~2.6% (INSEE, late 2025)—a level that erodes the purchasing power of uninvested savings and compresses financial error margins.

- Euro area growth: 0.8–1.2% projected early 2026—an environment where sequencing mistakes become more costly to correct.

What the Dominant Approach Misses—and the Framing Error It Perpetuates

The dominant approach to financial education assumes that spreading simple rules is enough to improve behavior: “save 10% of your income,” “diversify your portfolio,” “start investing early.” These guidelines are not wrong—but they are incomplete because they treat tools without addressing sequencing. Telling someone to “start investing early” without ensuring they have emergency savings and manageable debt is encouraging them to build an upper floor without foundations.

The pedagogical consensus assumes households make poor choices due to lack of information. Data analysis suggests a different hypothesis: decisions are often rational individually but incoherent in their overall arrangement. Each choice may make sense locally—opening a tax-advantaged equity account, buying an ETF, purchasing unit-linked life insurance. It is their combination over time that creates vulnerability. A household investing in equities before building emergency savings is not making a product-selection mistake—it is making a sequencing mistake. The investment decision is relevant; its timing is not.

This shift in perspective—from choices to the sequence of choices—transforms financial education. The relevant question is not “what is the best investment?” but “which step of the sequence am I at, and does my next decision respect this order?” Misleading economic indicators and market narratives (“you must invest now before it’s too late”) constantly push individuals to skip steps—a trap all the more effective because it relies on arguments that are individually valid.

Investing in risky assets (equities, ETFs, crypto, real estate funds) before building sufficient emergency savings (3–6 months of expenses). This reversed sequencing creates invisible fragility: at the next unexpected event (job loss, urgent expense, separation), the investment must be liquidated under potentially unfavorable market conditions. Expected investment returns are then destroyed by forced selling—exactly the mechanism documented by Dalbar’s behavior gap (3.5 points/year lost). The cause is not a poor product choice—it is poor timing within the wealth sequence.

| “Instrument catalog” approach | Sequencing approach | |

|---|---|---|

| Core question | What is the best investment? | Which step of the sequence am I at? |

| Identified source of error | Lack of information (we didn’t know) | Poor prioritization (we knew, but not in the right order) |

| Success metric | Return of the selected product | Sequence coherence and structural robustness |

| Shock protection | Diversification across instruments | Respecting the sequence safety → stability → exposure |

| Main trap | Choosing the wrong product | Choosing the right product at the wrong point in the sequence |

When the Macroeconomic Context Amplifies the Cost of Poor Sequencing

Wealth sequencing is a structural framework—it remains relevant regardless of the cycle. But certain macroeconomic environments dramatically amplify the cost of sequencing errors, and the current cycle is one of them.

The 2022–2025 regime shock as a stress test. Between 2022 and 2025, the abrupt shift from near-zero policy rates to levels of 4–5% in advanced economies upended the implicit hierarchy of financial trade-offs, as documented by ECB studies on monetary transmission to households. Choices that once seemed harmless—borrowing at variable rates, investing all available savings, purchasing property at the maximum borrowing capacity—became penalizing. This regime shift exposed fragilities that had long remained invisible: households with incoherent sequencing (exposure without safety buffers, leverage without stability) felt the impact first. The analysis of the role of real interest rates clarifies why the same nominal rate level can be accommodative or restrictive depending on inflation—and why household financial decisions must incorporate this dimension.

The current environment: compressed margins for error. In early 2026, European growth projections stand between 0.8% and 1.2%, core inflation remains around 2.6% (INSEE), and credit conditions are still restrictive. Margins for error are tightening: decisions made without prior safety buffers become more costly to correct. France’s Livret A savings account at 2.4% offers a slightly negative real return—a configuration that pushes some savers to seek yield in riskier assets, at the cost of sacrificing the safety function. This is precisely the most common sequencing mistake in the current cycle: skipping the safety step to move directly to exposure, attracted by the promise of returns.

Information overload as an amplifier. A common thesis holds that democratized access to financial information will gradually reduce household financial mistakes. Behavioral evidence suggests the opposite: information overload can amplify confusion when a proper framework is missing. Social media, financial influencers, and low-cost trading platforms make instruments more accessible—but they also encourage skipping safety steps to move straight into exposure. The issue is not accumulating more instrumental knowledge but having a prioritization framework—something information alone cannot provide.

How to Concretely Assess the Coherence of Your Wealth Sequence

Wealth sequencing is not an abstract concept—it translates into practical indicators anyone can assess.

Indicator 1: Coverage ratio. How many months of recurring expenses (rent/mortgage payments, food, transport, insurance, subscriptions) does immediately available savings cover? Less than 3 months = Step 1 incomplete. Between 3 and 6 months = foundation in place. Beyond 6 months = eligible to move to the next steps (unless income is highly volatile—freelancers, intermittent workers—in which case 6 to 12 months is more appropriate).

Indicator 2: Debt-service ratio. What share of income goes to debt repayment (mortgage + consumer loans)? Below 25% = stability comfort zone. Between 25% and 35% = caution required, limited shock-absorption margin if income declines. Above 35% = regulatory ceiling reached (HCSF in France), structural fragility. This ratio is the best indicator of the ability to maintain the wealth structure during shocks.

Indicator 3: Irreversibility ratio. What proportion of financial commitments is difficult to reverse in the short term? A mortgage, a real estate fund with lock-up clauses, private equity with an 8-year holding period—these are commitments that cannot be easily exited. If more than 70–80% of wealth is tied up in irreversible commitments, adaptability is compromised. This ratio does not judge whether choices are good or bad—it measures the degree of freedom remaining to adjust when circumstances change.

These indicators do not predict outcomes. They position a household’s trajectory along the safety–exposure axis, regardless of the instruments used—and help identify whether the next decision respects or violates the sequence.

Practical Implications for Different Profiles

For young professionals at the start of their careers. Priority is safety: build three months of expenses in liquid savings before any other allocation. Once this base is in place, begin investing—even modest amounts (€50–100/month in a diversified ETF through a tax-advantaged equity account, for example)—to benefit from holding duration, the most decisive factor for long-term returns. Typical mistake: investing in equities or crypto before building emergency savings, drawn by headline returns on social media.

For households with a recent mortgage. Stability is the central issue: the debt-service ratio must not compromise the ability to build emergency savings or absorb income shocks. In the current cycle (mortgage rates around 3.5–4%), monthly payments represent a structurally heavier burden than during the 2010–2020 decade. The credit-versus-investment trade-off only arises once emergency savings are rebuilt. Typical mistake: using all savings for the home down payment and ending up without a safety buffer after purchase.

For mid-life savers with established wealth. Optimization can come into play—but only if the first three steps are solid. Verify that emergency savings remain sufficient (they must be periodically reassessed based on expenses), that debt ratios are comfortable, and that investment allocation matches the real horizon (not the desired one). Typical mistake: multiplying optimization vehicles (tax incentives, real estate funds, private equity) without reassessing foundational strength—a form of sophistication that masks structural fragility.

Invalidation condition. This sequencing framework would lose relevance if real interest rates were durably anchored at very low (or negative) levels, reducing the cost of timing errors—because the opportunity cost of emergency savings would become negligible. Institutional mechanisms that automatically strengthen household financial safety nets (universal income, expanded unemployment insurance) would also reduce the impact of sequencing failures. An unexpected economic rebound could temporarily mask structural weaknesses—without resolving them.

Three Time Horizons for Applying Sequencing

Immediate horizon (0–6 months): assess the three indicators (coverage ratio, debt-service ratio, irreversibility ratio). If the coverage ratio is below three months, the absolute priority is rebuilding emergency savings—before any other allocation, including early debt repayment or additional investments.

Medium horizon (1–3 years): structure the sequence according to profile. Set up an automated savings and investment process (monthly transfers to regulated savings, then to a tax-advantaged equity account, for example) that mechanically respects sequencing without requiring active decisions each month. Automation reduces the risk of skipping steps under market narratives. Interaction with the economic cycle determines whether the environment amplifies or mitigates the cost of sequencing errors.

Long horizon (5 years and beyond): periodically reassess (once a year) the structure of the household balance sheet. The three ratios evolve with life-cycle changes (income shifts, childbirth, home purchase, inheritance) and macro cycles (rates, inflation, credit conditions). Sequencing is not a static framework—it is a lens applied to every new financial decision, regardless of timing. The weekly macro update and the hub dedicated to financial education provide a consistent monitoring framework.

The real financial risk is not choosing poorly—it is choosing in the wrong order. Financial education is fundamentally about sequencing: safety → stability → exposure → optimization. Each step serves a function that protects the next, and reversing this order creates cumulative fragilities revealed during shocks. The current cycle—high rates, weak growth, persistent inflation—compresses margins for error and amplifies the cost of poor sequencing. The right question is not “what is the best investment?” but “which step of the sequence am I at, and does my next decision respect this order?” This cycle-independent framework is the invisible foundation of resilient wealth building.

Robust: The sequencing principle (safety before exposure) is a structural framework validated by behavioral finance (Kahneman, Thaler) and empirical studies on the behavior gap (Dalbar, Morningstar). The impact of forced selling (linked to insufficient emergency savings) on long-term performance is documented across 30 years of data. The link between high debt-service ratios and wealth fragility during shocks is confirmed by Banque de France over-indebtedness data.

Context-dependent: The optimal level of emergency savings depends on income stability and family structure—there is no universal number. Future returns across asset classes are inherently uncertain. The macro cycle’s impact (rates, inflation) on the cost of sequencing mistakes varies over time. Indicative thresholds (3–6 months, 25–35% debt-service ratio) depend on individual circumstances.

This sequencing framework underpins the analysis developed across all articles dedicated to financial education. It does not prescribe an optimal allocation—it provides the lens to structure each decision in the right order, regardless of amount, product, or cycle phase.

- The real financial risk is not choosing poorly—it’s choosing in the wrong order. Wealth losses more often stem from sequencing failures than isolated bad decisions.

- The structuring sequence: safety (3–6 months of expenses) → stability (manageable debt) → exposure (long-term investment) → optimization (tax efficiency, fine allocation). Each step protects the next.

- 40% of risk-product subscriptions in the euro area are made by savers whose liquid savings cover less than three months of expenses—the most widespread and costly sequencing mistake.

- Three practical indicators assess sequencing coherence: coverage ratio (months of expenses in liquid savings), debt-service ratio (debt/income), irreversibility ratio (illiquid commitments/total wealth).

- This framework is invalidated if durably negative real rates eliminate the opportunity cost of savings, or if institutional mechanisms make financial safety automatic.

Frequently Asked Questions on Wealth Sequencing

Should I wait until I have six months of emergency savings before investing?

The idea is not to wait for a magical threshold, but to respect priority. If emergency savings cover two months and your budget allows €300/month in savings, allocating €200 to strengthen the safety buffer and €100 to begin investing (e.g., via a tax-advantaged equity account) respects sequencing: safety improves first, exposure begins in parallel. The mistake would be investing the full €300 while leaving the buffer at two months.

“Livret A earns nothing”—why keep money there?

At 2.4%, Livret A offers a slightly negative real return (core inflation ~2.6%). But emergency savings are not meant to generate returns—they are meant to prevent forced selling at a loss during unexpected events. Their value is measured in months of resilience, not annual percentages. A slightly negative real return costs about €20 per year in purchasing power on €10,000. A forced ETF sale at cycle lows can cost €3,000–5,000 on the same amount. The trade-off is clear.

Does this framework apply if I don’t have much money?

Sequencing applies regardless of amount—that’s its strength. With €100/month, the sequence is the same: first build a safety buffer (even €1,000 in regulated savings already provides a month of flexibility), then start investing modest amounts. The principle is not “reach a threshold before starting” but “respect the order of priorities in every decision.” Amounts scale with means—the sequence is universal.

Mis à jour : 20 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.