Macro-Financial Regimes: From the Great Moderation to the Structural Break

Economic cycles, systemic fragilities, and geopolitical recomposition: the structural forces that determine market regimes.

— Markets react to flows. Regimes transform under the weight of structures.

The global economy is not going through a bad patch. It is changing regime. The question that structures this pillar is not “where are we in the cycle?” — it is: what macroeconomic regime are we operating in, and what are the structural forces that produced it?

For three decades, the global economy operated under a remarkably stable regime: low inflation, accelerating globalization, cheap energy, and no major conflict between great powers. This regime — the “Great Moderation” — produced exceptionally favorable financial conditions and shaped the expectations of an entire generation of investors. Since 2020, this regime has fractured under the impact of three simultaneous shocks: the return of inflation, geopolitical fragmentation, and the resurgence of physical constraints on energy and commodities. These three forces are not transitory accidents — they are durably redefining the structural parameters of the global economy.

For an accessible introduction to the economic and financial mechanisms discussed here, see our guide to learning how to invest.

This page serves as the analytical summit of Eco3min’s Macroeconomics and Geopolitics cluster. It does not summarize its sub-pillars — it rises above them by offering a unified reading of the contemporary macroeconomic regime, its historical formation, its rupture, and its structural implications. The detailed mechanisms — cycle, inflation, debt, deglobalization, geopolitics — are developed in the dedicated sub-pillars.

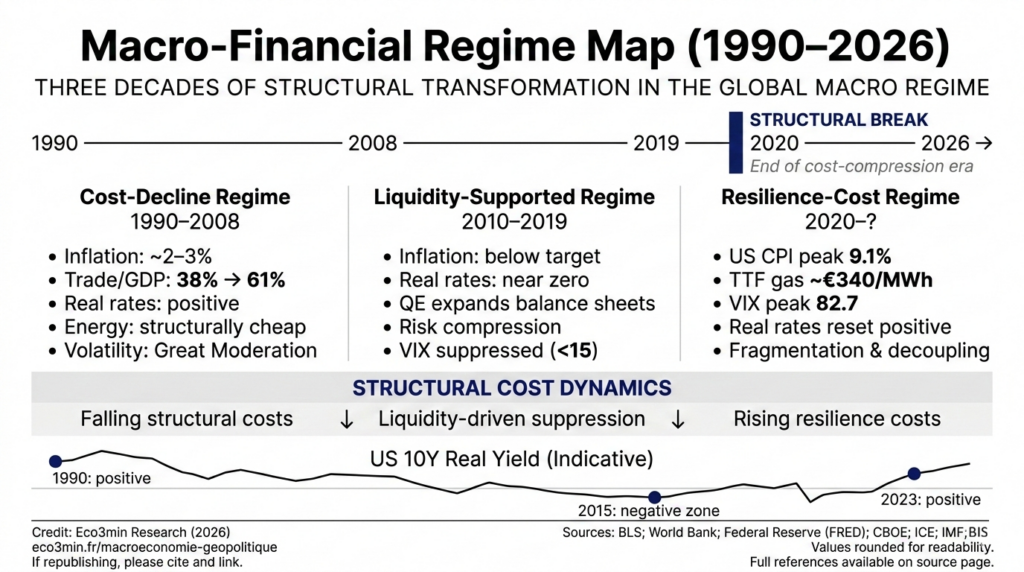

The eco3min macroeconomic barometer

This pillar formalizes the analytical frameworks. The monthly macroeconomic bulletin offers the operational reading applied to the current environment.

Key data series used in this analysis

Eco3min’s macro-financial analytical framework draws on several long-term historical series used to analyze economic regime transitions, inflation cycles, and asset price dynamics.

1990–2008: The Great Moderation — the declining-cost regime

The macroeconomic regime that governed the global economy from 1990 to 2008 rested on the convergence of three exceptionally favorable structural forces, whose simultaneous combination has no historical precedent.

Globalization as a disinflationary machine

The integration of 1.5 billion workers — China, India, the former Soviet bloc — into the global market economy constituted the most massive supply shock in economic history. World trade quadrupled between 1990 and 2008, rising from $4.3 trillion to $16.1 trillion (WTO). The global trade-to-GDP ratio rose from 38% to 61% (World Bank). Chinese exports surged from $62 billion in 1990 to $1.43 trillion in 2008 (WTO).

The effect on prices was spectacular. Prices of manufactured goods imported into the United States fell by 7% in real terms between 2000 and 2008 (BLS). The BIS estimates that globalization exerted a disinflationary pressure of 0.3 to 0.5 percentage points per year on advanced economy inflation (BIS, 2023). This continuous compression of production costs allowed central banks to keep rates low without triggering inflation — an equilibrium that appeared virtuous but masked an accumulation of fragilities.

The peace dividend and abundant energy

The collapse of the Soviet bloc opened a period of low perceived geopolitical risk. Global military spending fell from 4.7% of GDP in 1988 to 2.3% in 1999 (SIPRI) — a “peace dividend” that freed up considerable fiscal resources. Oil prices fluctuated between $15 and $35 per barrel for most of the 1990s (EIA), well below the real levels of the 1973 and 1979 shocks. European natural gas traded at around €10–20/MWh (ICE). Cheap energy functioned as an invisible subsidy to the entire economy.

Macroeconomic outcomes: unprecedented stability

The convergence of these forces produced what James Stock and Mark Watson formalized as the “Great Moderation” (2002): a historic reduction in macroeconomic volatility. The standard deviation of U.S. GDP growth fell from 2.7% over 1950–1984 to 1.2% over 1984–2007 (BEA). U.S. inflation stabilized around an average of 2.5% over 1990–2007 (BLS). The U.S. unemployment rate fell to 4% in 2000 — a level considered incompatible with price stability before globalization altered the Phillips curve.

For markets, this regime was exceptionally favorable. The S&P 500 quintupled between 1990 and 2007. Bond yields converged downward — the 10-year Treasury from 8.5% to 4.5% — supporting the valuation of all asset classes. Eurozone sovereign spreads compressed toward the Bund, with the market treating Greek and German debt as near-substitutes. Geopolitical risk premiums were temporary and dissipated within weeks.

This regime contained the seeds of its own destruction. Macroeconomic stability bred increasing complacency in risk-taking — Minsky’s paradox applied at the scale of the global economy. The 2008 collapse did not destroy this regime — it simply revealed the accumulated fragilities, as the Systemic Fragilities sub-pillar analyzes.

2010–2019: The regime of growth on life support

The regime that emerged from the 2008 crisis was fundamentally different from its predecessor — but this difference was masked for a decade by massive central bank intervention. Growth returned, markets reached new highs, unemployment fell. But the nature of the regime had changed.

Anemic growth boosted by liquidity

GDP growth in advanced economies averaged 1.8% per year between 2010 and 2019 (IMF), compared with 2.8% between 1990 and 2007 — a one-percentage-point slowdown that, compounded over a decade, represents a substantial shortfall. Total factor productivity growth — the ultimate driver of long-term wealth creation — fell to 0.5% per year in advanced economies, versus 1.0% in the prior period (Conference Board Total Economy Database). Larry Summers formalized this trajectory as “secular stagnation” (2013): a chronic shortfall in aggregate demand that interest rates, even at zero, could not correct.

The response was monetary rather than structural. The combined balance sheets of the four major central banks (Fed, ECB, BoJ, BoE) grew from $4 trillion at the end of 2007 to $16 trillion by end-2019 (BIS) — before the Covid shock. Policy rates remained near zero — or negative for the ECB and BoJ — throughout the entire period. This policy supported asset prices and enabled debt refinancing at historically low costs, but it did not resolve the structural problems — insufficient productive investment, demographic aging, slowing productivity — that weighed on potential growth. The mechanics of this policy are analyzed in depth in the Monetary Policy and Rates pillar.

Early geopolitical cracks

It was during this decade that geopolitics began to re-emerge as a macroeconomic variable. The annexation of Crimea (March 2014), Brexit (June 2016), the election of Trump (November 2016), and especially the U.S.-China trade war (March 2018) each signaled a paradigm shift. U.S. tariffs on Chinese imports rose from an average of 3.1% to 19% (Peterson Institute). U.S. business investment growth slowed from 5.9% to 1.4% per year between 2018 and 2019 (BEA). The global manufacturing PMI dropped below 50 for eight consecutive months.

But these signals were largely ignored by markets anesthetized by liquidity. The S&P 500 gained 189% between March 2009 and December 2019, despite two near-recessions in the industrial sector (2015–2016 and 2018–2019), an energy shock (oil collapsed to $26 in February 2016), and a repo crisis in September 2019 (repo rates 2% → 10% within hours). Every episode of stress was absorbed by central bank intervention, reinforcing the conviction that the monetary “put” was permanent. That conviction would be brutally challenged.

Interpreting market performance between 2010 and 2019 as validation of the underlying macroeconomic regime. The rise in asset prices primarily reflected the compression of discount rates — a mechanical effect of monetary policy — not an improvement in growth fundamentals. Globalization was a declining-cost regime; the 2010s were a regime of returns artificially inflated by liquidity.

2020–?: The triple rupture — inflation, fragmentation, physical constraints

The current regime is not the product of a single shock but of the convergence of three structural ruptures whose simultaneity is historically exceptional. Each one, taken in isolation, would have been enough to alter macroeconomic parameters. Combined, they redefine the framework in which the economy and markets will operate for the decade ahead.

Rupture 1: The return of inflation and the end of structural disinflation

U.S. CPI reached 9.1% in June 2022 (BLS), eurozone HICP hit 10.6% in October 2022 (Eurostat), and UK inflation peaked at 11.1% in October 2022 (ONS) — levels unseen in advanced economies in forty years. The initial shock was supply-driven — supply chain disruption, post-Ukraine energy price surge — but the underlying forces that made it persistent are structural.

Globalization, which had exerted a disinflationary pressure of 0.3 to 0.5 points per year, has reversed: the fragmentation of value chains, nearshoring, and supply redundancy carry a structural cost. The ECB estimates that this reconfiguration could add 1 to 2 percentage points to imported goods inflation over the medium term (ECB, Economic Bulletin 2023). Advanced economy labor markets are structurally tighter than before the pandemic — the U.S. job openings-to-unemployed ratio remained above 1.0 for most of 2022–2024 (BLS, JOLTS), a level unprecedented before 2021. The energy transition, while reducing costs in the long run, generates short-to-medium-term “greenflation” driven by the massive investment required and rising prices for critical metals.

Core PCE remained at 2.8% at the end of 2024 (BEA), 18 months after the rate peak — a transmission lag consistent with the upper bound of historical estimates, analyzed in the Inflation sub-pillar. The structural question is not “when will inflation return to 2%?” but “has the inflation regime changed durably, and if so, what are the consequences for real rates, debt, and valuations?”

Rupture 2: Geopolitical fragmentation and the end of the peace dividend

The invasion of Ukraine in February 2022 shifted geopolitics from a one-off risk to a permanent constraint. Global military spending reached $2.443 trillion in 2023, an all-time high in real terms (SIPRI). The number of trade restrictions quintupled between 2017 and 2024 (Global Trade Alert). The freezing of $300 billion in Russian central bank reserves was a first that altered the strategic calculus of every non-Western central bank — central bank gold purchases hit a record 1,037 tonnes in 2023 (World Gold Council).

The macroeconomic impact is measurable. Germany — Europe’s largest economy, whose model relied on the combination of cheap Russian energy and exports to China — saw its GDP stagnate at 0.0% in 2023 then decline by 0.1% in 2024 (Destatis). FDI into China collapsed from $344 billion to $33 billion between 2021 and 2023 (UNCTAD). The IMF estimates that geoeconomic fragmentation could reduce global GDP by 1 to 7% in the long run depending on the extent of decoupling (World Economic Outlook, 2023).

Geopolitics is no longer an exogenous risk to be modeled as a tail scenario. It is an endogenous parameter that reshapes production costs, capital flows, risk premiums, and inflation regimes. This transformation is analyzed in the Structural Geopolitics sub-pillar and the Deglobalization sub-pillar.

Rupture 3: The return of physical constraints

The third rupture is the return of physical constraints — energy, commodities, resources — to the center of macroeconomic analysis. European natural gas (TTF) reached €340/MWh in August 2022, versus an average of €20 over the prior decade (ICE) — a 17-fold increase. Wheat surged 60% in two weeks following the invasion of Ukraine, with Russia and Ukraine accounting for 28% of global exports (FAO). These shocks reflect the reintegration of commodities into the global inflationary dynamic and monetary policy trade-offs. The energy cost overrun for the European economy was estimated at over €200 billion for 2022 alone (Bruegel).

The energy transition, far from resolving these tensions, is creating new ones. The International Energy Agency (IEA) estimates that copper demand will need to double by 2040, lithium demand multiply by seven, and graphite demand by five to meet climate goals (IEA, Critical Minerals 2023). China controls 60% of global rare earth production, 70% of cobalt refining, and 80% of graphite processing (USGS, IEA) — near-monopoly positions that constitute as many potential geopolitical levers, as evidenced by Beijing’s export restrictions on germanium and gallium imposed in December 2023. Electric vehicles consume six times more copper than their combustion-engine equivalents. A large offshore wind turbine contains several tons of rare earths. The geography of critical minerals is drawing new fault lines, analyzed in the Energy and Commodities sub-pillar.

The convergence of the three ruptures: a new macroeconomic regime

The simultaneity of these three ruptures — structural inflation, geopolitical fragmentation, physical constraints — does not produce a mere episode of cyclical turbulence. It constitutes a macroeconomic regime change whose parameters differ radically from those that governed the preceding thirty years.

From a declining-cost regime to a costly-resilience regime

Globalization was a declining-cost regime: each year, offshoring, logistics optimization, and the integration of cheap labor compressed production costs. Fragmentation is a costly-resilience regime: redundancy, proximity, security, and supply diversification all come at a price — which the BIS estimates at between 1 and 7% of global GDP depending on the extent of decoupling (BIS, Annual Economic Report 2023).

This shift alters the fundamental inflation/growth trade-off that has structured macroeconomic policy for forty years. In the previous regime, central banks could keep rates low without triggering inflation thanks to globalization’s disinflationary pressure. In the new regime, structural forces push the equilibrium inflation rate higher — which implies higher real rates, more fragile debt sustainability, and structurally less favorable financing conditions.

Debt as a regime amplifier

Debt levels accumulated during the previous regime constitute the primary amplification factor — and vulnerability — of the current one. G7 public debt averages 122% of GDP (IMF). U.S. federal debt stands at 97% of GDP (CBO), with interest payments exceeding $880 billion in 2024 — more than the defense budget. Total global debt (public + private) exceeds $307 trillion (IIF, Global Debt Monitor 2024), or 330% of global GDP.

In a low-rate regime, this debt was arithmetically sustainable. In a regime of positive real rates and structural inflation, it becomes a constraint that limits governments’ room for maneuver, compresses productive investment, and creates a risk of fiscal dominance — the configuration in which debt constraints end up dictating monetary policy. This tension between debt sustainability and price stability constitutes one of the structural dilemmas of the new regime, analyzed in depth in the Monetary Policy and Rates pillar.

The end of volatility suppression

The previous regime was characterized by the systematic suppression of volatility — every episode of stress was contained by central bank intervention. The VIX averaged below 15 for most of 2017 and 2019 (CBOE). The monetary “put” functioned as free insurance against downside risk. The new regime is characterized by the return of structural volatility: the VIX reached 82.7 in March 2020 (CBOE), a level exceeding the 2008 peak. 2022 saw historic market moves — long-term bonds -31%, equities -19%, crypto -65%, a positive equity/bond correlation unseen since the 1970s. Volatility is not a malfunction — it is the mechanism through which prices adjust to a regime change that market participants are progressively absorbing.

The business cycle in the new regime

The business cycle has not disappeared — but its parameters have changed. Under the Great Moderation, recessions were rare (two in 18 years: 2001 and 2008), moderate outside of financial crises, and followed by recoveries supported by massive monetary easing. The new regime alters these parameters across three dimensions.

Cycles will likely be shorter and choppier. Structurally higher inflation reduces central banks’ room to support activity during slowdowns. The threshold for triggering monetary easing is mechanically higher when inflation remains above target — meaning the Fed or ECB may be forced to keep rates restrictive longer than in the prior decade, increasing the risk of recession through excessive tightening.

Supply shocks become more frequent. Geopolitical fragmentation, commodity tensions, and climate change multiply potential disruptions — pandemic (2020), energy (2022), shipping (2023–2024). Unlike demand shocks, which central banks know how to treat (rate cuts, QE), supply shocks create a dilemma between supporting activity and fighting inflation — a dilemma that barely existed in the previous regime.

The monetary safety net is less reliable. With already inflated balance sheets (the Fed’s still at $6.8 trillion at end-2024, seven times its pre-2008 level), residual inflation, and record public debt, central banks’ intervention capacity is structurally reduced. The monetary “put” still exists, but its strike price is higher and its effectiveness less certain. Reading the cycle in this new context is developed in the Business Cycle sub-pillar.

How structural forces transmit to markets

The structural forces identified in this pillar are not theoretical abstractions — they transmit to financial markets through concrete, measurable channels. This reading is essential because financial markets and the real economy never move at the same time, which creates structural lags between the business cycle and market dynamics.

The real rate channel. The shift in real rates from negative to positive — 10-year TIPS from -1.19% in August 2021 to +2.40% in October 2023 (Federal Reserve) — mechanically alters valuation multiples across all asset classes. The S&P 500 forward P/E fell from 23x to 15.5x between end-2021 and October 2022 (FactSet). Real estate, bonds, credit, and speculative assets all undergo the same repricing to varying degrees.

The risk premium channel. Geopolitical fragmentation and structural uncertainty raise the risk premiums demanded by investors. The Treasury “term premium” — the compensation for holding duration — has turned significantly positive again after a decade of compression (NY Fed). Gold reached record highs above $2,400 per ounce in 2024 (LBMA), embedding a structural geopolitical premium. Eurozone sovereign spreads once again reflect the differentiation of fiscal risk between countries.

The dispersion channel. The previous regime, dominated by liquidity, compressed performance differentials between countries, sectors, and companies — “a rising tide lifts all boats.” The new regime, dominated by fundamentals and structural constraints, amplifies dispersion. The Magnificent 7 accounted for over 60% of the S&P 500’s gains in 2023 and 2024 (S&P Global), while the rest of the market stagnated. Countries benefiting from nearshoring (Mexico, Vietnam, India) outperform those that lose from it. Sector-level dispersion is elevated, reflecting the heterogeneity of exposure to the structural forces at play. These dynamics propagate across the entire global financial system through the central role of the dollar in global flows.

The detailed analysis of this transmission is developed in the Financial Markets pillar.

Three trajectories for the macroeconomic regime ahead

The current regime is a transition whose outcome remains open. Three trajectories are plausible.

Controlled stabilization — the base case — assumes a gradual normalization of inflation, managed geopolitical fragmentation (selective decoupling without rupture), and an orderly adaptation of economies to the new cost of capital. Global growth would stabilize around 3% (IMF baseline), real rates would remain positive but moderate, and markets would progressively adjust to a regime of lower expected returns and higher volatility. This scenario assumes minimal fiscal discipline and the absence of a major geopolitical shock.

An accelerated fragmentation scenario would see intensified U.S.-China escalation (Taiwan crisis, extended cross-sanctions), a new energy shock (Middle East conflagration, Strait of Hormuz crisis), or a sovereign debt crisis in a major economy. The cost of fragmentation would reach the upper range of the IMF estimate (-7% global GDP). Inflation would become structurally elevated again, defaults would multiply, and systemic fragilities would crystallize. This scenario, unlikely in its most extreme form, is plausible enough to justify a permanent risk premium.

A positive technological breakthrough scenario — the least consensual — assumes that artificial intelligence and energy breakthroughs (fusion, Generation IV) generate a productivity shock sufficient to offset the structural inflationary forces and fragmentation. History shows that technological revolutions (electricity in the 1920s, computing in the 1990s) have the potential to alter macroeconomic regimes — but with diffusion lags of 10 to 20 years that make this scenario unlikely in the near term.

The global economy has changed regime. The framework in which markets and businesses operated for three decades — low inflation, accelerating globalization, cheap energy, no major conflict, central banks in permanent support mode — no longer exists in its prior form. The emerging regime is structured by three converging forces: durably higher inflation, growing geopolitical fragmentation, and the return of physical constraints on energy and commodities. Globalization was a declining-cost regime; the period ahead is a costly-resilience regime. The relevant question is not “when will things return to normal?” but “what are the parameters of the new regime, and what are the implications for debt, growth, valuations, and price formation?” That is the question this pillar and its sub-pillars endeavor to answer.