Why Macroeconomic Indicators Lag the Real Economy

The statistical construction of macroeconomic indicators gives them a structural lag that limits their ability to reveal the cycle in real time.

TL;DR

A GDP figure describes an economy that closed 30 to 90 days earlier, a structural lag built into how data is collected, aggregated, and revised.

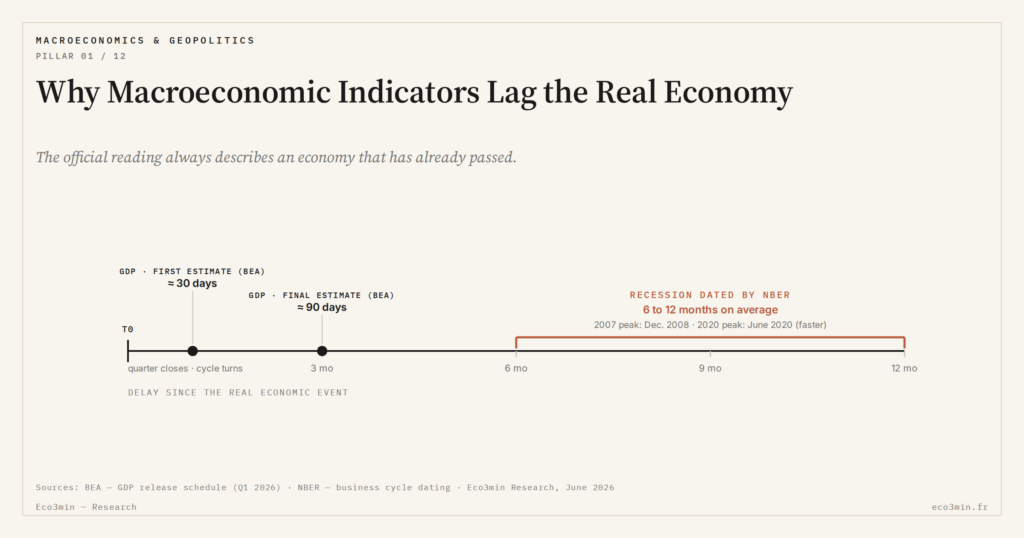

- Eurostat releases its first euro-area GDP estimate about 30 days after the quarter ends, the unavoidable delay of aggregating the national accounts of 20 countries.

- The US BEA issues three estimates (advance, preliminary, final) over three months and revises every five years; the first-to-revised gap reached 1.2 percentage points over 2020–2024.

- The NBER dates US recessions 6 to 12 months late on average; the March 2020 recession was declared only in June 2020, when the economy had already begun recovering.

- Later revisions can flip the sign of a quarter, turning growth first reported as positive into a negative reading after correction, and vice versa.

Macroeconomic indicators are often interpreted as direct signals of the state of the economy. In reality, their statistical construction — data collection delays, aggregation methods, successive revisions — imposes a structural lag on the actual dynamics of the cycle. The GDP published today reflects an economy from several months ago. This inertia is built into the nature of these measures, regardless of the quality of the statistical agencies. The common mistake is to attribute to them a capacity for anticipation that they do not have by design. Understanding this lag mechanism helps avoid confusing retrospective confirmation with a real-time signal.

This delay is rarely quantified, which sustains the illusion of responsiveness. When a GDP figure is released, it describes a period that closed 30 to 90 days earlier. The revisions that follow can change the diagnosis by several tenths of a point. This is not an accidental flaw — it is the normal functioning of a statistical system designed for ex post accuracy, not for real-time diagnosis.

Anatomy of the lag: from collection to publication

The lag in macroeconomic indicators breaks down into three successive layers. The first is the collection delay: activity, employment, and price data pass through surveys, administrative filings, and registers whose processing takes several weeks. In the euro area, Eurostat publishes its first estimate of quarterly GDP about 30 days after the end of the quarter — an unavoidable delay imposed by the need to aggregate the national accounts of 20 countries. For a closer look, see the Eco3min macroeconomic analysis frameworks.

The second layer is the aggregation delay. Raw data are adjusted for seasonal variations, working days, and calendar effects — all treatments that add time and introduce margins of error. The real economic cycle unfolds while these processes are underway, which means the diagnosis is structurally behind the event it is trying to describe.

The third layer is the revision cycle. The Bureau of Economic Analysis (BEA) publishes three successive estimates of U.S. GDP — advance, preliminary, and final — spread over three months, then carries out annual and benchmark revisions every five years. The average gap between the first estimate and the revised figure reached 1.2 percentage points over the 2020–2024 period, an exceptionally high level that reflects the post-pandemic instability of economic structures.

What this lag implies for reading the cycle

The most direct consequence is that cycle turning points are identified only after the fact. The NBER, which dates U.S. recessions, does so with a lag of 6 to 12 months on average. The March 2020 recession was not officially declared until June 2020 — by which time the economy was already in recovery. This delay is not a malfunction: it reflects the methodological caution needed to avoid false positives.

For investors or decision-makers, this lag means they should not wait for statistical confirmation before adjusting their diagnosis. Predictive tools such as the yield curve or industrial orders try to fill this gap, but with their own limitations. Monthly data, despite their imperfections, offer finer granularity than quarterly data — provided they are read as partial signals, not as verdicts.

Treating the first estimate of an indicator as an established fact. The first GDP release is an approximation based on incomplete data. Later revisions can reverse the sign of quarterly growth — which means a quarter initially reported as positive may later turn negative after correction, and vice versa.

Progress in high-frequency data — card spending, mobility, digital transactions — could reduce this structural lag. These sources make it possible to observe certain segments of activity almost instantaneously. But they do not cover the whole economy and raise representativeness issues. The methods of deep cycle analysis remind us that data speed does not guarantee relevance — and that the lag in official indicators is the price of their comprehensiveness and methodological rigor.

Last updated — 10 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…