Monetary Policy Explained: Incentives, Limits, and Real Economic Impact

Few economic topics are as systematically invoked—and as deeply misunderstood—as monetary policy. Every central bank decision triggers a wave of analysis about its supposed immediate effects on growth, employment, or markets. This media omnipresence, however, obscures a more subtle reality.

Monetary policy does not function like a control panel where levers are adjusted to produce predictable outcomes. It operates according to a fundamentally different logic: that of an environment of constraints and incentives shaping the conditions under which economic decisions are made, without ever dictating them.

This analysis does not aim to describe the transmission channels of monetary policy to the real economy. Its ambition is more fundamental: to clarify what monetary policy truly is, what it can influence, what it conditions—and, above all, what permanently escapes its reach.

The analytical frameworks used in this article draw in particular on publications from the Bank for International Settlements, the IMF, the ECB, and the Federal Reserve.

Monetary policy: an environment, not a command instrument

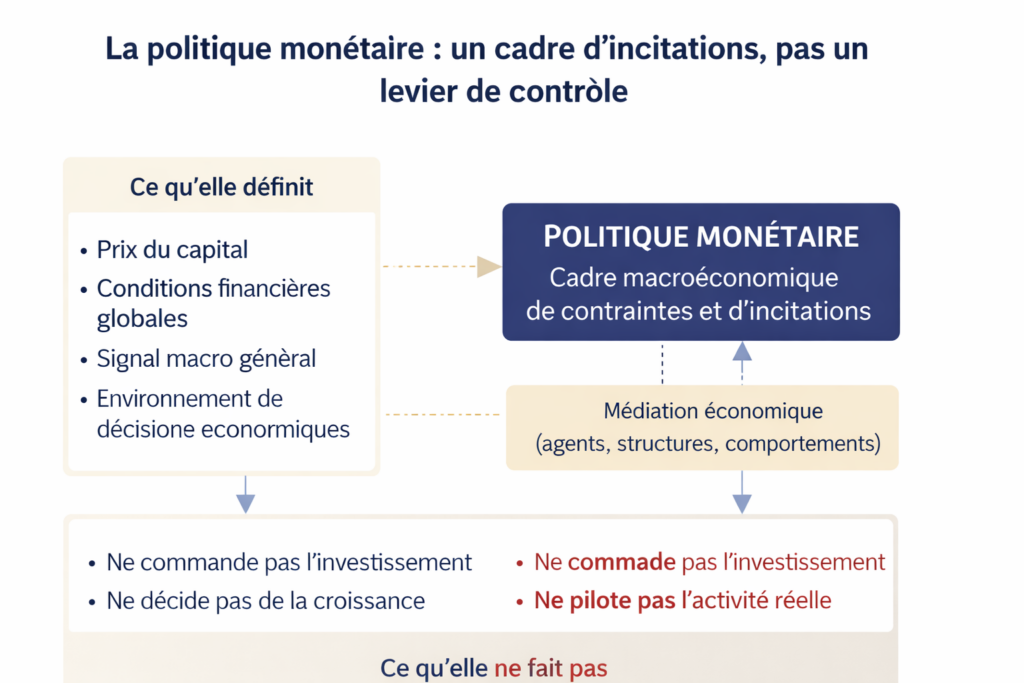

The dominant image of monetary policy—as a set of levers operated by technicians to regulate the economic machine—is largely a myth. In reality, no central bank decides where capital is invested, which projects deserve funding, or how value creation is distributed across the economy.

What monetary policy actually does is define the reference cost of capital, as consistently emphasized by the ECB, the Fed, and the BIS in their analytical frameworks. It establishes a global financial framework—a set of general conditions—within which firms, households, and financial institutions make their own decisions. The distinction is crucial: this is a system of incentives, not a mechanism of direct control.

This framework alters trade-offs between consumption and saving, between risk and prudence, between present and future. But it never substitutes for the millions of decentralized decisions that ultimately constitute economic activity. Monetary policy creates a context; it does not generate activity itself.

Understanding this distinction helps avoid a common pitfall: interpreting every monetary action as a directly transformative force, when it is only one parameter among many in a complex macroeconomic architecture shaped by multiple, sometimes conflicting, dynamics.

The impossibility of direct action on the real economy

Why is monetary policy so often attributed powers it does not possess? Likely because two distinct dimensions are conflated: influencing versus executing. A central bank influences general financial conditions; it does not execute concrete economic decisions.

It does not instruct firms to invest in one sector rather than another. It does not impose technological choices. It does not select viable projects or deserving actors. The real economy remains a space of autonomous decisions, driven by individual expectations, specific constraints, and microeconomic rationalities that no central authority can program.

This distance between the monetary sphere and productive activity is not a flaw to be corrected—it is an intrinsic feature of the system. Monetary policy always operates through mediation: it modifies an environment of constraints without ever becoming direct economic action.

This gap explains why markets react less to monetary decisions themselves than to the anticipated trajectory of their effects—a core mechanism in market expectation cycles, where monetary information is priced in well before observable effects materialize in the real economy.

Monetary policy sets the cost of capital and the financial environment without steering real investment, whose response depends on the economic regime and structural mediations.

The mechanisms through which these constraints translate into the real economy are addressed separately in our article: What is monetary policy and how it affects the real economy.

Keeping this reality in mind is essential: any analysis that treats monetary policy as an autonomous engine of economic activity risks producing overstated—or outright incorrect—conclusions about its actual influence.

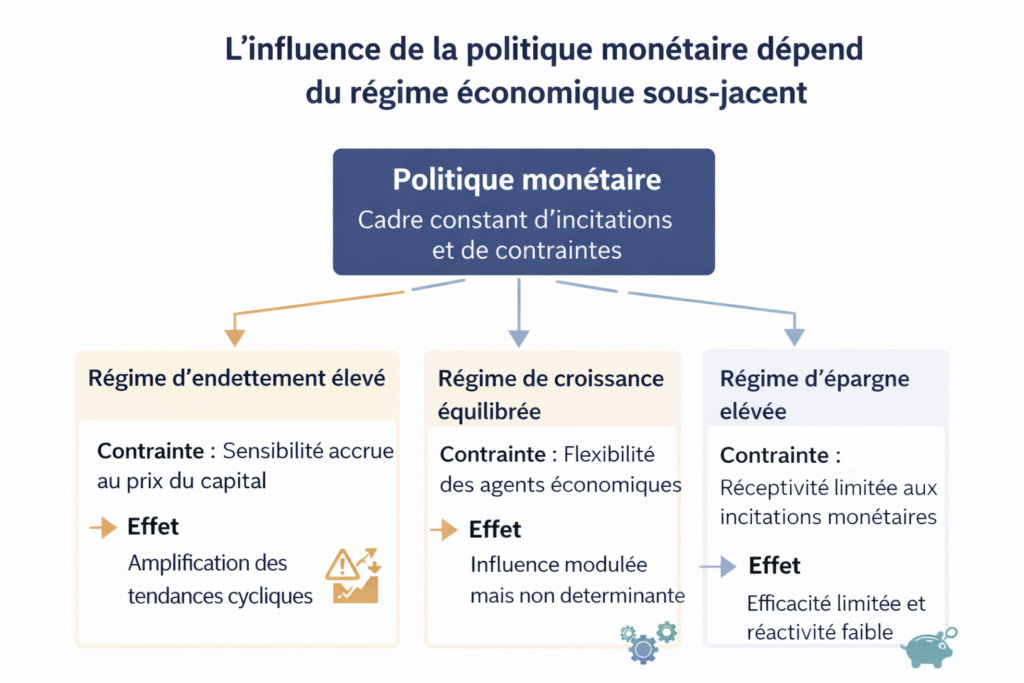

Effectiveness depends on the prevailing economic regime

If monetary policy does not directly command outcomes, its influence is far from constant. It varies significantly depending on the economic regime in which it operates, as documented by IMF and BIS research on heterogeneous monetary transmission. This regime is itself partly shaped by real constraints—particularly energy and material conditions—that structure inflation and the broader macroeconomic environment. The article Commodities, inflation, and monetary policy explores these mechanisms in detail. This structural dependency explains an apparent paradox: identical monetary measures can produce radically different outcomes across contexts.

The level of indebtedness determines agents’ sensitivity to changes in borrowing costs. The structure of the banking system conditions how monetary impulses translate into financing decisions. Economic agents’ behavior, shaped by recent experience and risk perception, modulates their responsiveness to central bank signals.

In some configurations, monetary policy amplifies existing dynamics. In others, it may have little to no effect—without indicating any design or implementation failure. Monetary effectiveness is never absolute; it is always contingent.

This dependence on the economic regime rules out any universal interpretation of monetary policy. It requires careful analysis of underlying configurations, rather than mechanical application of general principles across different contexts.

Persistent illusions of monetary omnipotence

The central role of monetary policy in public debate fuels several enduring misconceptions. The first is attributing near-total control over the economy to central banks. This view dramatically overestimates their power while ignoring the complexity of decentralized economic mechanisms.

A second widespread misconception assumes that favorable monetary conditions are sufficient to generate growth. This belief confuses necessary conditions with sufficient ones. Sustainable growth depends on structural factors—innovation, human capital, institutions—that largely lie beyond the scope of monetary policy, as repeatedly emphasized by the IMF and OECD in their analyses of potential growth.

A third misconception views monetary policy as a tool for permanent stabilization. This mechanistic perspective ignores the fact that deep imbalances, exogenous shocks, and long-term structural changes cannot be neutralized by simple adjustments to financial conditions.

These illusions are not trivial. They shape expectations, structure dominant narratives, and can lead to persistent analytical errors—both in macroeconomic interpretation and in the reading of market dynamics.

The limits of monetary policy

Properly defining the scope of monetary policy requires clearly identifying what lies beyond its reach. Certain fundamental dimensions of the economy are structurally outside its influence.

Productivity depends on technological, organizational, and human factors that no adjustment in financial conditions can generate. Demographics impose long-term trends over which monetary policy has no control. Deindustrialization results from strategic choices, productive specialization, and geoeconomic dynamics that transcend the monetary framework.

The quality of capital allocation depends on microeconomic decisions, institutional frameworks, and governance structures that cannot be corrected through changes in policy rates.

Recognizing these limits does not diminish the importance of monetary policy. On the contrary, it is the condition for understanding it properly: a constraining macroeconomic framework whose action remains fundamentally indirect.

This analysis fits within a long-term macro-financial perspective, grounded in institutional monetary frameworks and in the observation of differentiated effects across economic regimes.

Viewing monetary policy as an imperfect system of incentives, dependent on the economic regime in which it operates, is a prerequisite for any clear-eyed analysis of contemporary economic and financial dynamics.

Last updated — 3 April 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.