Commodity Price Formation: Time Asymmetry and Structural Mechanisms

Commodity prices do not reflect an instantaneous balance between supply and demand. They result from a structural asymmetry between physical supply—whose adjustment takes years—and financial demand, which can reconfigure in a matter of hours.

Why Commodity Prices Never Reflect Real-Time Supply–Demand Equilibrium

Commodity prices do not measure equilibrium — they measure the time lag between two worlds operating at different speeds.

Price formation in commodity markets rests on a fundamental asymmetry: physical supply—constrained by geology, industrial capacity, and capital intensity—adjusts over years. Financial demand, driven by portfolio allocation and macro expectations, reconfigures within hours. This structural time lag is what generates the characteristic volatility of commodities—not fluctuations in physical supply and demand alone.

Understanding this asymmetry changes how commodity markets are interpreted: what looks like a shortage signal may simply be financial repositioning, while apparent normalization may conceal structural underinvestment. For asset allocators and industrial decision-makers, separating the physical signal from financial noise is a prerequisite for robust decisions. This article analyzes the structural mechanisms of commodity price formation and their implications for reading the current cycle.

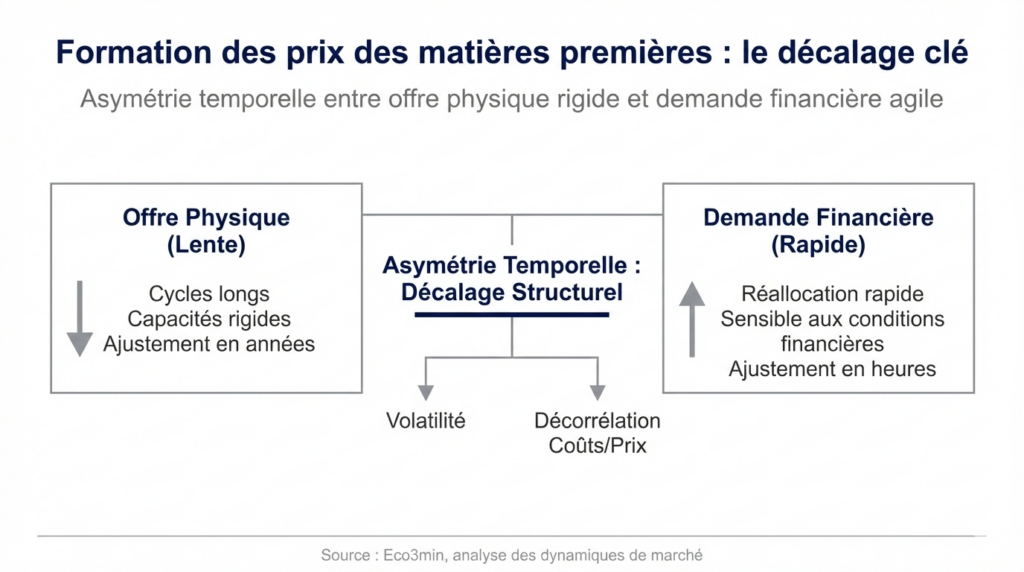

Viewing commodity prices solely through daily fluctuations is akin to confusing the thermometer with the fever. Behind every price move lie two distinct timeframes: physical supply cycles spanning five to twelve years—from exploration to production, according to the IEA and World Bank—and financial demand capable of reconfiguring within a few trading sessions in response to an inflation print, a central bank decision, or portfolio rebalancing. Physical and derivatives commodity markets follow fundamentally different logics—and their coexistence generates the structural volatility of commodities.

This dynamic fits within the broader framework of commodities in the global economy and interacts with the role of real rates and global financial conditions, which determine both the cost of capital for extractive projects and investors’ appetite for the asset class.

- Physical supply adjusts over 5–12 years (extractive investment cycle); financial demand reconfigures within hours

- This time lag creates structural volatility and persistent divergences between market prices and physical fundamentals

- Global financial conditions (real rates, dollar, liquidity) amplify the asymmetry by simultaneously affecting supply (cost of capital) and financial demand (portfolio allocation)

Commodity prices do not measure equilibrium — they measure the time lag between two worlds operating at different speeds. Physical supply, rigid over a 5–12 year horizon, coexists with financial demand that reconfigures within hours—an asymmetry that produces structural commodity volatility. Transmission operates through three channels: supply inelasticity (preventing quantity adjustment), financialization (amplifying price moves beyond physical fundamentals), and global financial conditions (real rates, dollar) that simultaneously shape extractive capital costs and asset-class demand. This framework is documented by the BIS, IMF, and IEA; the calibration of the gap between financial prices and physical equilibrium in the current cycle—marked by cumulative underinvestment and positive real rates—remains debated.

Core Mechanism: How Temporal Asymmetry Generates Volatility

Commodity price formation follows a causal chain whose defining feature is the speed asymmetry between physical supply and financial demand.

Expectation shock (macro, geopolitical, monetary) → Financial repositioning (hours/days) → Price move amplified by supply inelasticity → Divergence: financial price vs physical equilibrium → Slow correction via inventories and/or production (months/years)

Price alone performs the short-term adjustment function, given the rigidity of physical quantities.

Trigger: structural inelasticity of physical supply. Commodity production relies on heavy assets—mines, fields, refineries, transport infrastructure—whose commissioning requires 5–12 year horizons and multi‑billion‑dollar investments per project. The IEA (World Energy Outlook 2025) estimates average delays from investment decision to first commercial output at ~7 years for conventional oil, ~10 years for copper, and ~12 years for lithium. Over a few quarters, supply is therefore largely inelastic: a 50% price increase does not translate into higher available volumes—it triggers an investment decision whose effects materialize only in the following decade. This inelasticity forces prices to bear the entire short‑term adjustment burden, producing structurally higher volatility than in manufactured goods markets.

Transmission channel: financialization and demand velocity. Facing rigid supply, financial demand stands out for its velocity. It aggregates heterogeneous flows: industrial hedging, strategic pension allocations, macro hedge fund bets, portfolio decorrelation strategies. Whenever the financial environment shifts—real‑rate inflection, inflation‑expectation revision, monetary regime change—commodity exposures can be reshaped within a few sessions. An IMF working paper (Cheng & Xiong, 2014, “Financialization of Commodity Markets”) formalizes this mechanism, showing that financialization structurally increased the correlation between commodity prices and global financial conditions beyond what physical fundamentals justify. CFTC data show that net speculative positions in oil futures can shift by 200,000–300,000 contracts within weeks—volumes equivalent to several days of global production moved without any physical barrel changing hands.

Amplifier: global financial conditions as a multiplier. Global financial conditions—real rates, dollar strength, liquidity—act as multipliers of temporal asymmetry by simultaneously influencing both sides of the equation. On the supply side, high real rates raise the cost of capital for extractive projects (with multi‑decade ROI), restraining investment and prolonging inelasticity. On the financial-demand side, a strong dollar compresses real commodity prices (quoted in dollars) and reshapes portfolio allocation. The BIS (Annual Report 2025) documents this dual influence, noting that extractive investment cycles are negatively correlated with real rates with a 2–3 year lag—meaning current underinvestment (linked to positive real rates in 2022–2025) will translate into supply constraints only in 2027–2030.

Consequence: persistent divergences between financial prices and physical fundamentals. These channels combine to generate prolonged episodes where market prices diverge from underlying physical equilibrium. Prices can rise without physical shortages (financial positioning anticipating future tightness) or fall despite tight physical markets (speculative unwinds, stronger dollar). The oil market offers constant illustrations: pullbacks in Brent do not always signal excess physical supply but may reflect financial reallocations disconnected from real flows. The natural gas market shows the reverse dynamic: certain price signals go largely unnoticed while foreshadowing structural tensions ahead.

- Investment → production delay: ~7 years (conventional oil), ~10 years (copper), ~12 years (lithium). Source: IEA, World Energy Outlook 2025.

- Financial repositioning: 200k–300k oil futures contracts shifted within weeks (≈ several days of global production). Source: CFTC.

- Commodity/financial-conditions correlation: structurally higher since 2000s financialization. Source: IMF, Cheng & Xiong, 2014.

- Extractive investment/real-rate correlation: negative, with 2–3 year lag. Source: BIS Annual Report 2025.

- Cumulative underinvestment: new capacity additions (energy, metals) remain below prior upcycle projections (end‑2025 sector data). Sources: IEA, World Bank.

Cumulative extractive underinvestment + positive real rates (capex drag) + declining commercial inventories + strong dollar (real price compression) → setup conducive to supply tensions in 2027–2030, even if short‑term prices remain under financial pressure.

What the Consensus Prices In — and the Underinvestment It Underestimates

The dominant view—promoted by major investment bank commodity desks and echoed in market outlooks—assumes gradual normalization: anticipated monetary easing should stabilize prices, and supply will respond to past price signals with a reasonable lag. This diagnosis has merit—previous cycles did show supply responses to high prices with 3–5 year delays.

Its limitation lies in underestimating cumulative underinvestment. IEA data (World Energy Investment 2025) show upstream oil & gas capex remains ~25% below its 2014 peak despite comparable price levels. In critical metals (copper, lithium, cobalt, nickel), the investment gap is even more pronounced relative to projected demand from the energy transition. The World Bank (Commodity Markets Outlook 2025) estimates investment in transition metals must triple by 2030 to meet climate goals—a pace never achieved historically.

The consensus is therefore right to expect short‑term price normalization (driven by financial easing) but may underestimate structural tensions emerging at the cycle horizon. The accumulation of investment delays and the growing fragmentation of value chains—documented in the analysis of the new geopolitical front of critical minerals—create conditions for a durable high‑volatility regime, even absent acute shocks.

Interpreting commodity price moves as direct signals of physical shortages or surpluses. In reality, short‑term price dynamics mostly reflect financial repositioning (portfolio allocation, hedging, speculation) whose timing is disconnected from physical supply. Price declines can coexist with structural underinvestment, and rallies can occur without immediate physical strain. The relevant signal is not the price level but the gap between market price and marginal cost of production—an indicator that anchors price formation over the cycle horizon.

| “Price reflects supply and demand” view | Temporal asymmetry view | |

|---|---|---|

| Implicit assumption | Supply adjusts quickly to price signals | Supply inelastic for 5–12 years; price = adjustment variable |

| Observed signal | High price = shortage, low price = surplus | Price reflects financial/physical interaction, not instant equilibrium |

| Time horizon | Quarterly (production/consumption data) | Cycle (5–12 years supply, hours financial demand) |

| Main risk | Overreacting to temporary supply shocks | Underestimating structural underinvestment masked by financial easing |

| Key variable | Physical supply–demand balance | Price vs marginal cost gap, extractive capex, real rates, CFTC positioning |

Inventories, Marginal Cost, and Geopolitics: Three Asymmetry Amplifiers

The core mechanism of temporal asymmetry is amplified by three structural factors that shape the intensity and duration of price–fundamental divergences.

Inventories as buffers—and their depletion as accelerators. Between rigid supply and volatile demand, inventories (strategic and commercial) play a decisive buffer role. As long as inventories are sufficient, the system can absorb financial-demand shocks without abrupt price corrections. But once inventories are depleted, volatility rises non‑linearly—prices must absorb imbalances that quantities can no longer offset. The role of inventories in price formation explains why tensions persist even without visible supply-chain disruptions. EIA and IEA data show OECD commercial oil inventories at end‑2025 below their five‑year average—a thinner cushion that heightens price sensitivity to any shock.

Marginal cost as a long‑term anchor. Over the cycle horizon, commodity prices converge toward marginal production cost—the cost of the highest‑cost unit needed to balance the market. When prices remain below this level, marginal output becomes uneconomic, capacity contracts, and prices eventually recover. This anchoring mechanism, analyzed in the framework of marginal cost and equilibrium commodity pricing, is the long‑term constraint that short‑term financial arbitrage cannot eliminate—only postpone.

Geopolitics as additional rigidity. Supply adjustment is not purely technical or geological—it is political. Producer states’ fiscal choices, rent‑seeking strategies (OPEC+), trade sanctions, and regulatory constraints directly affect volumes. The role of producer countries in price cycles shows why tensions can persist long beyond initial financial signals. The case of palladium illustrates this dynamic: extreme production concentration (Russia, South Africa) combined with structurally rigid auto demand creates tensions that neither price nor technological substitution can quickly resolve. Growing geopolitical fragmentation—documented in the analysis of critical minerals as a new geopolitical front—adds further rigidity to supply.

Implications for Interpreting the Current Cycle

Reading market prices. The temporal asymmetry framework implies that current commodity prices embed global financial conditions (real rates, dollar, liquidity, speculative positioning) more than the true state of physical equilibrium. Price pullbacks amid a strong dollar and positive real rates do not necessarily signal oversupply—they may mask structural underinvestment whose effects will emerge only years later. The most relevant indicator of physical market conditions is not the spot price but the futures curve structure (contango vs backwardation) and commercial inventory levels.

Energy transition. The shift to a decarbonized economy requires massive increases in critical metal output (copper, lithium, cobalt, nickel, rare earths). The temporal asymmetry framework highlights the core dilemma: demand for these metals rises over 5–10 years, but supply can adjust only with comparable delays. This phase shift creates structural bottleneck risks that could slow the transition itself—risks not yet reflected in financially pressured spot prices.

Asset allocation. Commodities as an asset class respond simultaneously to physical fundamentals (supply, demand, inventories) and financial conditions (real rates, dollar, positioning). This dual dependency makes the asset class more correlated with macro conditions than with its own fundamentals over the cycle horizon—a phenomenon amplified by financialization documented by the IMF. Integrating commodities into portfolios requires explicitly separating the financial component (rate- and dollar-sensitive) from the physical component (inventory- and capex-sensitive)—a distinction rarely made in standard allocation models.

Invalidation conditions. This framework loses relevance if unexpected production accelerations (extraction technology breakthroughs, regulatory easing) significantly shorten supply-adjustment delays. A major negative demand shock (deep global recession) or targeted derivatives regulation (speculative position limits) could also narrow the gap between financial valuations and physical fundamentals. Conversely, tighter-than-expected monetary policy, geopolitical escalation, or faster energy-transition momentum would amplify asymmetry and extend the high‑volatility regime.

Three Time Horizons for Reading Commodity Markets

Short term (0–6 months): financial conditions dominate price formation. Key indicators: 10‑year real rates, DXY index, net speculative positioning (CFTC), commercial inventories (EIA, IEA). A strong dollar and positive real rates exert downward pressure on real commodity prices. The short‑term risk is abrupt financial repositioning (in either direction) disconnected from physical fundamentals—amplified by position concentration in the most liquid futures.

Cycle horizon (1–3 years): cumulative underinvestment begins to translate into supply constraints. The key question is the pace of financial-condition normalization (falling real rates, weaker dollar) and its ability to revive extractive capex. If real rates remain durably positive, underinvestment persists and supply tensions accumulate—a setup conducive to price spikes when physical demand accelerates. Interaction with the real economic cycle will determine timing.

Structural horizon (5+ years): the energy transition reshapes commodity demand structure. Demand for critical metals trends higher while hydrocarbon demand plateaus (IEA baseline). This structural shift creates new asymmetries: transition metals (copper, lithium) enter a relative underinvestment cycle comparable to oil in the 2000s, while hydrocarbons face stranded‑asset risks. The weekly macro dashboard tracks these dynamics.

Commodity prices do not measure a supply–demand equilibrium—they measure the time lag between physical supply adjusting over years and financial demand reconfiguring within hours. This fundamental asymmetry explains why commodity volatility is structural, not cyclical, and why prices can diverge persistently from physical fundamentals. The current cycle adds another layer: cumulative underinvestment in extractive capacity, amplified by high real rates and a strong dollar, sets the stage for supply tensions over the cycle horizon that financially pressured spot prices do not yet reflect. The most informative signal is not the price level but the gap between market price and marginal production cost, combined with extractive capex trends.

Robust: Commodity supply inelasticity over horizons shorter than five years is a structural fact documented by the IEA, World Bank, and academic literature. Commodity market financialization and its impact on correlation with financial conditions are formalized (Cheng & Xiong, 2014, IMF). The anchoring role of marginal production cost over the cycle horizon is confirmed by historical data. Cumulative extractive underinvestment since 2014 is measurable in capex data.

Uncertain: The precise timing of supply tensions linked to underinvestment is inherently unpredictable—depending on physical demand trajectories tied to the global cycle. The magnitude of acceleration in transition‑metal demand (driven by policy and energy-transition pace) shows wide estimate dispersion. The ability of derivatives markets to accurately anticipate future physical tensions remains debated—history shows as many cases of over‑ as under‑anticipation.

Reading commodity markets through temporal asymmetry—rather than price levels or quarterly supply–demand balances—provides a more robust analytical framework to understand structural volatility, identify divergences between financial prices and physical fundamentals, and anticipate tension points over the cycle horizon.

- Commodity prices do not reflect instant equilibrium—they measure the lag between physical supply adjusting over 5–12 years and financial demand reconfiguring within hours.

- Prices alone perform short‑term adjustment given quantity rigidity—producing structurally higher volatility than in manufactured goods markets.

- Global financial conditions (real rates, dollar) amplify asymmetry by simultaneously shaping extractive investment (capital cost) and prices (financial arbitrage).

- Cumulative underinvestment since 2014—amplified by positive real rates—creates supply‑tension risks in 2027–2030, masked short‑term by financial price pressure.

- This framework is invalidated if technological breakthroughs significantly shorten supply adjustment, or if a major negative demand shock eliminates structural tensions.

Mis à jour : 20 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.