Investment Strategy vs Performance — Why Results Mislead Decisions

Understanding why an investment strategy structures decisions over time, beyond observed outcomes and market conditions.

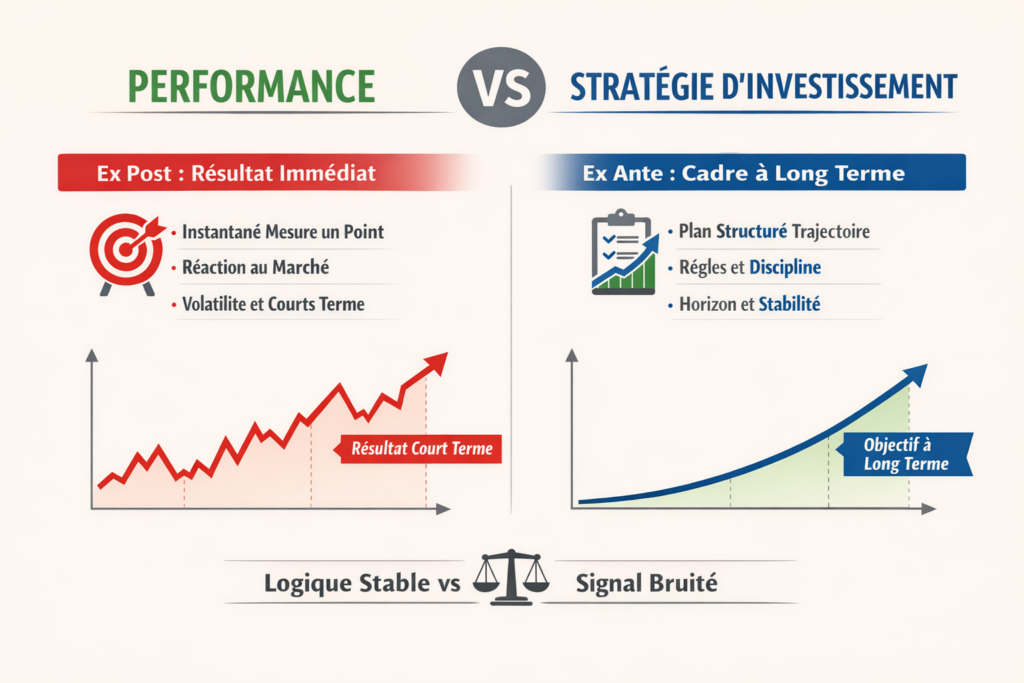

Visible results attract attention, but they say nothing about the logic that produced them. What shapes an investment trajectory is first and foremost a framework that organizes decisions before their effects become observable. An investment strategy establishes this logic and allows for a sequence of consistent choices despite uncertainty and market variability. When this framework is absent, decisions become difficult to connect. The most common confusion is judging an approach based on isolated performance rather than on the robustness of its decision architecture. This distinction between observed outcomes and process consistency is what clarifies the central role of strategy.

- Performance is an ex post outcome, strategy is an ex ante framework.

- A strategy connects decisions over time through explicit rules.

- Without a prior framework, observed results become misleading signals.

What prices imperfectly reflect is often related to timing. In early 2026, markets still shaped by high policy rates and highly dispersed asset performance reinforce the illusion that the “right choice” is immediately visible in results. This gap between instant interpretation and long-term consistency makes the strategic question more pressing than it appears.

Performance measures a point, strategy defines a trajectory

Observable performance is a snapshot. It captures a result at a given point in time, under specific market conditions. A strategy, by contrast, is a sequence of rules that connects these points over time. It defines in advance what can change, what must remain stable, and under what conditions an adjustment becomes legitimate.

A frequently underestimated fact is that two trajectories can display identical performance over twelve months while relying on fundamentally different logics. One may be consistent with a long-term horizon and accepted volatility, while the other results from successive arbitrage decisions without a guiding thread. The visible result then masks the fragility of the process.

This distinction is essential to understand why performance cannot be the starting point. Used as an initial compass, it leads to constantly rewriting the rules based on a noisy signal.

Strategy does not just organize decisions; it organizes their sequence over time.

This confusion is often reinforced by a shift between decision layers. What belongs to strategy — stable rules and time horizon — is frequently mixed with tactical adjustments or timing reactions. Yet this distinction is essential to understand why seemingly rational decisions can produce an incoherent trajectory, as illustrated by the difference between strategy, tactics, and timing.

The implicit consensus: judging strategy by recent performance

Part of the operational consensus assumes that a strategy is validated or invalidated by its recent performance. Dominant projections, often implicit, suggest that a framework that “does not work” over a given period should be replaced.

This interpretation relies on an implicit equivalence between strategic validity and recent performance. Yet a strategy can remain coherent while going through a phase of underperformance, precisely because it is exposed to an unfavorable regime. This gap is highlighted by the analysis of strategy coherence versus observed performance, which are often wrongly conflated.

The analysis diverges on a key mechanism: short-term performance aggregates exogenous factors — interest rate regimes, flows, macro shocks — that strategy is not designed to optimize continuously. Confusing strategic validation with cyclical success amounts to ignoring the role of time lags and regimes.

The facts are clear: in 2025, performance dispersion across asset classes reached levels rarely observed since 2010–2012, driven by the combined effect of positive real rates and concentrated flows. The implicit assumption that a “good” framework must perform in all environments is therefore questionable.

Why the absence of strategy leads to incoherent decisions

Without an explicit strategy, each decision becomes dependent on the signal of the moment. The reasoning fragments: what was acceptable yesterday suddenly becomes unacceptable today, not because the framework has changed, but because the observed outcome has.

This inconsistency has a measurable cost. Industry data shows that excessive decision turnover — frequent reallocations, rule changes — generates cumulative friction of approximately 50 to 150 basis points per year over the long term, combining direct costs and timing errors. These orders of magnitude, observed over 2015–2024, illustrate a structural mechanism rather than an anomaly.

The real question is not whether a recent decision performed “well” or “poorly,” but whether it was consistent with the framework defined before uncertainty. This is what an investment strategy aims to capture, beyond immediate outcomes.

Facts, assumptions, and interpretations: clarifying levels

Facts: as of early 2026, policy rates in major developed economies remain well above their 2010–2019 averages, with still-restrictive monetary policies. Observed twelve-month performance is therefore strongly conditioned by this regime.

Assumption: a strategy is designed to navigate multiple regimes, not to optimize a single environment. It assumes variability is part of the process.

Interpretation: if this dynamic persists, the temptation to adjust rules based on recent outcomes increases mechanically, to the detriment of overall consistency.

This interpretative bias is reinforced by seemingly reassuring indicators — moderate volatility, positive aggregate performance — which may mask process fragility. A structured reading of these signals, such as that provided by a framework of misleading economic indicators, helps distinguish apparent stability from real robustness.

Time horizon acts as a decisive filter. The same decision can be coherent or not depending on the horizon considered, regardless of its immediate outcome. This is why investment horizon fundamentally changes the meaning of decisions, turning a temporary deviation into either noise or a true signal.

What the reader really wants to know

The discomfort often comes less from results than from uncertainty about the validity of the framework used.

Behind this question lies a simple concern: is it risky to rely on a framework that does not “pay off” immediately? The analytical answer is that the main risk is not temporary underperformance, but the absence of rules when the environment changes.

Variables that could invalidate this interpretation

This analysis would be challenged if a structural shift durably reduced uncertainty — for example, prolonged macro stability with low return dispersion — or if exogenous constraints (regulatory, tax-related) forced adjustments independent of the strategic framework. Conversely, a shock in rates or flows would further widen the gap between short-term performance and process consistency.

Even when structured, a strategy remains bounded by implicit assumptions about regimes, volatility, or liquidity. When these parameters shift persistently, the framework ceases to be fully effective without being immediately invalidated. This gray zone is precisely what is described in the analysis of the structural limits of any investment strategy.

Confusing temporary underperformance with a strategic error. This interpretation is misleading because it ignores market regimes and adjustment lags, whereas strategy should be evaluated based on the consistency of decisions.

Useful indicators to assess consistency

- Decision turnover rate: a rapid increase signals adaptation to outcomes rather than adherence to the framework.

- Gap between stated rules and actual decisions: the larger it is, the more fragile the strategy becomes.

- Exposure to macro regimes: assess whether decisions remain aligned despite changing conditions.

An investment strategy precedes performance because it organizes decisions under uncertainty, while observed outcomes primarily reflect the market regime.

Conclusion: framework before numbers

This is not the base case today, but the temptation to judge a strategy by its latest results remains strong. The issue is not to deny the importance of performance, but to place it in its proper role: an ex post indicator, never a foundational principle. As long as macro regimes remain unstable, the consistency of the framework deserves more attention than isolated figures.

Within the ecosystem of investment strategies, this distinction determines how future decisions are interpreted, whether in terms of markets, companies, or wealth trajectories.

3 key takeaways

- Performance describes an outcome; strategy describes a logic.

- Judging a framework based on recent numbers amplifies decision biases.

- Ex ante consistency becomes rarer as uncertainty increases.

Mis à jour : 20 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.