Restrictive Monetary Policy: Why Tightening Continues After Rate Hikes End

Restrictive monetary policy does not slow the economy instantaneously. Its effectiveness rests on indirect mechanisms — credit, balance sheets, contract repricing — whose real effects appear long after the initial decisions and persist well after the tightening cycle ends.

Tight monetary policy does not stop when rate hikes stop.

A restrictive monetary policy mainly works with lags. Its effects do not depend on the last rate move but on the progressive diffusion of tightening through credit, balance sheets and the repricing of financing.

The policy-rate peak does not mark the end of tightening. As long as financial conditions remain restrictive and the stock of debt is rolled over at new terms, monetary pressure continues to intensify mechanically.

The ECB stopped raising policy rates in September 2023. The Fed did the same in July 2023. For a large part of the consensus, the tightening cycle is therefore over — and its effects fully transmitted. This is precisely where the most costly misinterpretation of the current cycle lies. Because restrictive monetary policy does not cease to act when rate hikes stop: it continues to operate through the progressive renewal of the stock of credit, the repricing of financing conditions and the cumulative erosion of balance sheets. The policy-rate peak does not mark the end of tightening — it marks the start of its most intense phase on the real economy.

This temporal paradox explains why cyclical diagnoses are so frequently upended during tightening phases. The economy can display positive growth, a resilient labor market and stable confidence indicators for several quarters after the rate peak — not because tightening is ineffective, but because its heaviest effects have not yet materialized. Recent history confirms this: the tightenings of 2000 and 2006–2007 produced their recessionary effects only 12 to 24 months after the last rate hike, a pattern documented by the BIS (annual report 2025) and consistent with the academic literature on transmission lags. Convergent estimates from the ECB, the IMF and the BIS place the peak macroeconomic impact of a tightening episode between 12 and 24 months after the policy-rate inflection — a lag that the current cycle does not contradict.

These mechanisms fit within the broader framework of monetary policy and interest rates, and constitute a specific application of the analysis of monetary transmission to the real economy. This article focuses on the concrete mechanics by which restrictive policy continues to produce effects after the apparent end of the hiking cycle.

Tight monetary policy does not stop when rate hikes stop. Restrictive policy mainly acts through the progressive rollover of the stock of credit at new conditions, the cumulative erosion of balance sheets and the endogenous tightening of lending standards — mechanisms that continue to operate independently of the policy-rate level. The peak macro impact of the 2022–2023 tightening is estimated, by convergent IMF and BIS assessments, to fall between the second half of 2025 and the first half of 2026 — i.e., now. This delayed-accumulation mechanism is well established in the literature; the open question is its intensity in a cycle characterized by heterogeneous debt structures and residual savings accumulated during the pandemic.

The central mechanism: how tightening diffuses after hikes end

The diffusion of restrictive monetary policy into the real economy follows a causal chain whose defining characteristic is temporality: each link operates with its own lag, and it is the sequential accumulation of these lags that produces the delayed peak impact. The lags of restrictive monetary policy and the delayed effects of interest rates on activity are among the most documented — and most systematically underestimated — phenomena in macroeconomics.

Trigger: restrictive rate levels maintained over time. The starting point is not an isolated rate hike but the maintenance of policy rates in restrictive territory — i.e., above the estimated neutral rate. The ECB raised its deposit rate from -0.5% to 4% between July 2022 and September 2023; the Fed raised its federal funds from 0–0.25% to 5.25–5.50% between March 2022 and July 2023. But effective tightening is not measured by the pace of hikes: it is measured by how long rates remain restrictive. This is the “surface of restriction” concept — the area under the curve of positive real rates — that determines the cumulative strength of monetary pressure. A BIS working paper (Borio, Disyatat & Rungcharoenkitkul, 2023) formalizes this notion, showing that macro impact depends more on the duration and cumulative level of tightening than on the speed of increases.

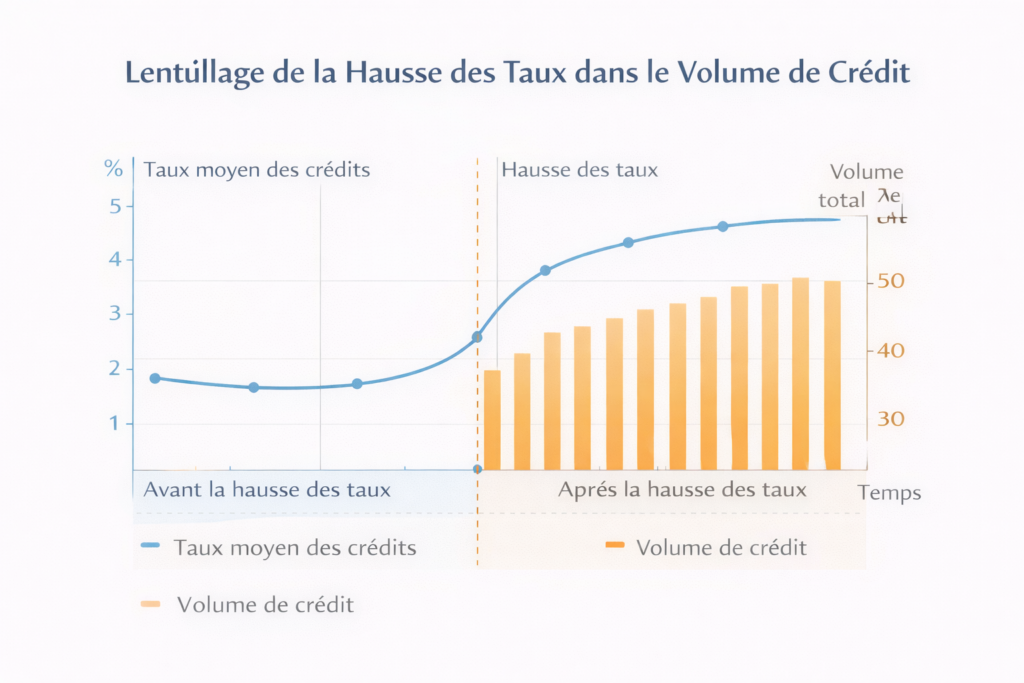

Transmission channel: progressive repricing (roll-over) of the stock of credit. The most powerful — and most underestimated — mechanism is the gradual repricing of the existing stock of debt at new rate conditions. Each month, a fraction of fixed-rate loans matures and is renewed at the current rate; each quarter, variable-rate contracts reprice. This roll-over process means the economy’s effective average borrowing rate continues to rise well after the last policy-rate increase. ECB data (December 2025) illustrate this dynamic: the rate on new corporate loans in the euro area rose from about 1.5% in 2021 to 4.5% at the end of 2025, but the average rate on the total stock of loans — which determines the actual financial burden — had only partially converged to that level, leaving a residual gap of roughly 150 basis points. Closing that gap, purely mechanically, will continue to raise financial charges for another 12 to 18 months.

Amplifier: endogenous tightening of lending standards. Beyond higher borrowing costs, restrictive policy triggers an autonomous tightening of banks’ lending criteria. Faced with rising credit risk and declining collateral values, banks tighten standards — higher collateral requirements, strengthened coverage ratios, rejection of marginal profiles — regardless of policy-rate levels. The ECB’s Bank Lending Survey (Q4 2025) reports that net tightening of lending standards for corporate loans continues for the ninth consecutive quarter. This amplification channel works like the financial accelerator described by Bernanke and Gertler (1995): deteriorating balance sheets reduce borrowing capacity, which compresses activity, which further weakens balance sheets — a feedback loop that self-sustains even if the central bank stops tightening.

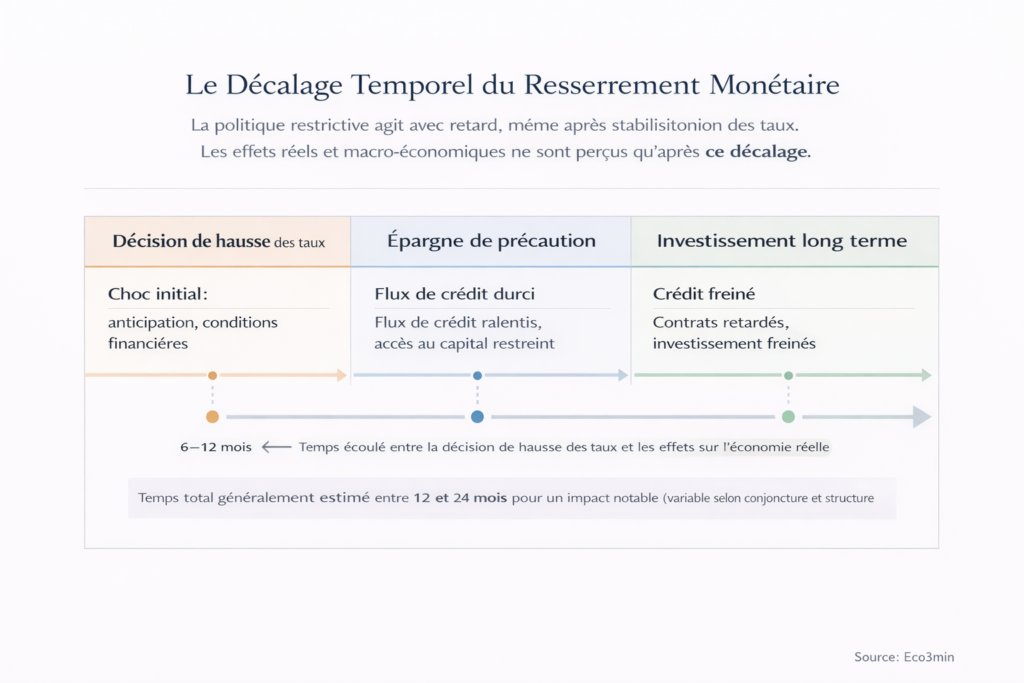

Macro consequence: sequential accumulation-induced slowdown. The delayed diffusion of tightening produces a characteristic slowdown pattern whose sequence is documented by past cycles: financial conditions tighten first (T+0 to T+6 months), then credit flows contract (T+6 to T+12), then productive investment slows (T+12 to T+18), then employment starts to adjust (T+18 to T+24). This sequence explains why labor-market resilience — often cited as proof that tightening is fully transmitted — is in reality the last link, not the first. The IMF (World Economic Outlook, October 2025) estimates the peak impact of the 2022–2023 tightening on advanced-economy growth to fall between the second half of 2025 and the first half of 2026.

What the consensus underestimates: confusing a pause with the end of tightening

The dominant reading of the monetary cycle, carried by most institutional projections and a significant slice of market consensus, rests on a seemingly logical argument: policy rates have stopped rising, inflation is falling, employment is holding — therefore most of the tightening is behind us. This diagnosis has the virtue of clarity. Its flaw is to confuse two distinct realities: the end of the hiking cycle (a fact) and the end of the transmission of tightening to the economy (an unverified assumption).

The roll-over mechanism of the stock of credit is enough to demonstrate this distinction. As long as the average rate on the outstanding stock of debt has not converged to the rate on new loans, tightening continues to diffuse mechanically without any new monetary-policy decision. An ECB working paper (Altavilla, Burlon, Giannetti & Holton, 2022) shows that convergence speed varies by a factor of two to three across euro-area countries, depending on the share of fixed-rate lending and the average maturity of banks’ portfolios. In France, where mortgage credit is almost exclusively fixed-rate, convergence is particularly slow — which means the restrictive effect of the 2022–2023 tightening will continue to accumulate for French households until at least 2027 via the loan-renewal mechanism alone.

Observed short-term cyclical resilience is therefore fully compatible with an unfinished transmission process. It does not prove the innocuousness of tightening — it illustrates its lag. Monetary expectations can temporarily dampen this pressure if agents expect imminent easing, but they do not neutralize the fundamental roll-over mechanism.

Confusing a pause in hikes with the end of tightening. Stabilized policy rates do not imply a relaxation of financial constraints: as long as rates remain restrictive and the stock of credit renews at new conditions, monetary pressure intensifies mechanically. The 2000 and 2006–2007 tightenings produced their largest recessionary effects 12 to 18 months after the final rate increase — a pattern that current-cycle data do not contradict.

| “Tightening absorbed” reading | Delayed-accumulation reading | |

|---|---|---|

| Central assumption | The economy adjusts quickly after the rate peak | Adjustment continues via roll-over of the stock of credit |

| Invoked signal | Labor-market resilience, falling inflation | Credit contraction, tightening lending standards |

| Analysis horizon | 6–12 months after the rate peak | 12–36 months, with sequential accumulation |

| Main risk | Residual inflation delays the pivot | More persistent and deeper slowdown than anticipated |

| Key variable | Policy rates, forward guidance | Average rate on the stock of credit, Bank Lending Survey, debt-service ratio |

Heterogeneity, threshold effects and feedback loops: the complexity of delayed effects

The sequential-transmission scheme describes the general mechanism, but the reality of delayed effects is crossed by sources of complexity that profoundly alter their intensity and distribution.

Sectoral heterogeneity: vulnerable segments absorb the shock first. Restrictive monetary policy does not weaken the economy uniformly. Credit-dependent SMEs are affected earlier and more severely than large firms with access to bond markets. Households on variable rates face immediate adjustment, while long-term fixed-rate borrowers remain protected for years. Capital-intensive sectors (real estate, construction, infrastructure) bear the brunt of pressure before service sectors. This heterogeneity creates a diffusion pattern: fragility pockets emerge in the most credit-sensitive compartments — SME defaults, construction slowdowns, commercial real-estate tensions — well before aggregate indicators signal broad slowdown.

Threshold effects and non-linearities. Delayed effects of tightening do not unfold linearly. As long as economic agents have adjustment capacities — precautionary savings accumulated during the pandemic, the ability to compress margins, the temporary postponement of nonessential investments — the economy absorbs pressure without visible rupture. But these capacities deplete, and when a critical threshold is reached, behaviors switch abruptly: firms move from postponing to cancelling investments, households from smoothing consumption to cutting back, banks from marginal tightening to credit rationing. The ECB’s Bank Lending Survey (Q4 2025) indicates that the stock of excess household savings in the euro area — accumulated during the pandemic and that served as a buffer — is now largely depleted in most member economies, removing a protective factor that had slowed transmission.

Balance-sheet–credit feedback loop. The interaction between deteriorating balance sheets and lending standards is the main amplification mechanism for delayed effects. Rate increases depress collateral values (real estate, financial assets), which restricts credit access, which compresses activity, which further weakens collateral. This loop — formalized by the BIS as the financial accelerator — can turn an orderly slowdown into a sharper contraction if initial balance sheets are sufficiently fragile. According to Banque de France data (Q3 2025), nonfinancial corporate debt in France reached 160% of GDP, a level that mechanically increases the economy’s sensitivity to the balance-sheet channel and amplifies the potential of this feedback loop.

Geographic fragmentation. The desynchronization of economic cycles amplifies the complexity of delayed effects. Debt-structure differences determine transmission speed much more than policy-rate levels: in economies where variable-rate credit dominates (Spain, Nordic countries), monetary pressure has already largely transmitted; in economies where fixed-rate lending dominates (France, Germany), most transmission is still to come via roll-over. The same monetary policy thus produces time-shifted and intensity-asymmetric effects across the euro area.

Measuring real tightening: beyond policy rates

The policy rate triggers tightening but is a poor indicator of its effective intensity at any given time. The most relevant indicators to assess where transmission truly stands are downstream: the gap between the average rate on the stock of credit and the rate on new loans measures remaining repricing to come; changes in lending standards (Bank Lending Survey) capture endogenous tightening; the debt-service ratio relative to firms’ EBITDA (or to households’ disposable income) measures the effective financial burden.

FRED’s long series on the U.S. household debt-service ratio (Debt Service Ratio, series TDSP) offers historical perspective: over the last five tightening cycles, this ratio continued to rise on average 10 to 16 months after the last rate hike, confirming that the effective financial burden increases long after the hiking cycle ends. The delayed impact of policy rates on the real economy is therefore better measured by financial-burden indicators than by rates themselves. The distinction between nominal and real rates strengthens this point: a stable policy rate combined with falling inflation means a rising real rate — tightening intensifies mechanically even absent any central-bank action.

Implications for reading the current cycle

If the delayed-accumulation framework is relevant, it changes the reading of several ongoing dynamics.

For cyclical diagnosis. The cyclical resilience observed in 2024 and early 2025 should not be read as proof that tightening has been fully transmitted. It is consistent with the documented transmission sequence: financial conditions tightened (done), credit is contracting (in progress), investment is slowing (in progress), employment has not yet significantly adjusted (to come). Structural lags in macro indicators add another layer of delay. The wave of loan repricings and corporate refinancings continues, mechanically extending the restrictive effect regardless of future rate decisions. The timing of the economic cycle in which tightening occurs determines whether the adjustment remains orderly or turns into contraction.

For monetary policy itself. Transmission lags create a permanent dilemma for central banks: they must decide whether to ease or maintain policy based on data that reflect the past, not the current state of transmission. Easing too late risks letting delayed accumulation produce excessive slowdown; easing too early risks reigniting inflation before the disinflation process is consolidated. This dilemma is structurally insoluble under the current monetary-policy framework — it can only be managed, not eliminated. Coupling with the broader real cost of money framework confirms that the effective degree of restriction evolves even when nominal rates are stable.

For firms and households. Agents most exposed to repricing — firms with short-term or variable-rate debt, households renewing mortgages, capital-intensive sectors — face a mechanical rise in financial burden for another 12 to 18 months. If this mechanism interacts with demand slowdown — itself a consequence of monetary transmission — the risk is a scissors effect: rising financial costs combined with decelerating revenues, a configuration historically associated with growing defaults and a sharper investment slowdown.

Invalidation condition. This framework loses relevance if a rapid and massive easing (a 200-basis-point or larger cut within 12 months) interrupts roll-over before peak impact is reached, or if targeted fiscal support neutralizes financial pressure on the most exposed agents. It would also be invalidated if excess savings turn out to be larger than current estimates, prolonging households’ absorption capacity. Conversely, an exogenous shock (energy crisis, trade tensions, sovereign stress) would amplify and accelerate delayed effects by abruptly reducing remaining adjustment capacities.

Three time horizons to monitor delayed effects

Short horizon (0–6 months): the current phase corresponds, according to the documented sequence, to the peak impact on credit and the start of investment adjustment. Priority indicators to monitor: Bank Lending Survey (lending standards and credit demand), flows of new loans to firms and households, payment delays and early defaults in the most exposed segments (SMEs, commercial real estate). The euro-area PMI (48–49 end-2025) and credit contraction signal active transmission. The short-term risk is a non-linear crystallization if adjustment capacities deplete in the most leveraged economies.

Cycle horizon (1–3 years): the determining question is the speed and scale of monetary easing and its ability to interrupt accumulation dynamics before they become a self-sustaining contraction. If central banks delay easing sufficiently, the balance-sheet–credit loop could trigger in the most leveraged economies (France, Netherlands, Nordic countries). The structural dynamics of the real economic cycle will determine whether adjustment remains orderly. Interaction with the structural underinvestment highlighted in the potential-growth analysis could amplify slowdown if productive investment suffers a sustained decline.

Structural horizon (5+ years): the current cycle is a large-scale test of central banks’ ability to steer disinflation without inflicting structural damage. If delayed effects induce prolonged underinvestment, consequences will outlast the cycle and affect long-term trajectories — a case where a countercyclical instrument by design (monetary policy) would produce structural effects (erosion of potential output). This risk questions the limits of monetary action and strengthens the case for a broader framework integrating monetary policy, its incentive framework and structural limits.

Tight monetary policy does not stop when rate hikes stop — it intensifies. Progressive repricing of the stock of credit, endogenous tightening of lending standards and cumulative balance-sheet erosion continue to operate regardless of policy-rate levels. Short-term cyclical resilience illustrates the transmission lag, not its absence. The peak impact of the 2022–2023 tightening is materializing now, and the central question is no longer “Is monetary policy restrictive?” but “How long will its effects continue to accumulate?” — a question that policy rates alone cannot answer.

Robust: The roll-over mechanism of the stock of credit is arithmetic — it happens mechanically so long as rates remain high and loans mature. The 12–24 month transmission lag is a convergent estimate from the ECB, the Fed, the BIS and the academic literature. The sequence financial conditions → credit → investment → employment is documented across the last five cycles. Endogenous tightening of lending standards is observable in Bank Lending Surveys.

Uncertain: The intensity of the peak impact in the current cycle is debated — adjustment capacities (residual savings, high employment) could mitigate the effect. The speed of forthcoming monetary easing will determine whether the balance-sheet–credit loop triggers or is interrupted. Firms’ responses to financial pressure (margin compression vs investment cuts vs employment adjustment) depend on micro factors hard to aggregate. The exact timing of any non-linear tipping point is inherently unpredictable.

Regular monitoring of the weekly macro checkpoint enables confronting this framework with the most recent credit, balance-sheet and financial-conditions data. Several trajectories remain open, but reading tightening through its delayed-accumulation mechanisms — rather than by policy rates alone — provides a more robust framework to anticipate the real-economy trajectory in coming quarters.

- Tight monetary policy does not stop when rate hikes stop: progressive repricing of the stock of credit, endogenous tightening of lending standards and balance-sheet erosion continue transmission independently of rate decisions.

- The peak macro impact of the 2022–2023 tightening falls, according to convergent IMF and BIS estimates, between the second half of 2025 and the first half of 2026 — i.e., now.

- Observed short-term resilience illustrates the transmission lag (financial conditions → credit → investment → employment), not the absence of tightening effects.

- The most relevant indicators are the average rate on the stock of credit (vs new loans), lending standards (Bank Lending Survey), and the debt-service ratio — not policy rates.

- This framework is invalidated if massive easing interrupts repricing, or if adjustment capacities (excess savings, corporate margins) prove more resilient than estimated.

Mis à jour : 30 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.