Why Economic Cycles Are Not Synchronized Across Regions

Regional cycles do not move in lockstep. Three structural channels — monetary policy, fiscal policy, productive specialization — explain why growth gaps between the US, the euro area, and Asia are widening rather than closing. Why aggregate readings of 'global conditions' increasingly miss what matters.

Economic cycles diverge across regions because productive specializations, financial structures, and policy mixes shape the transmission of every shock differently.

TL;DR

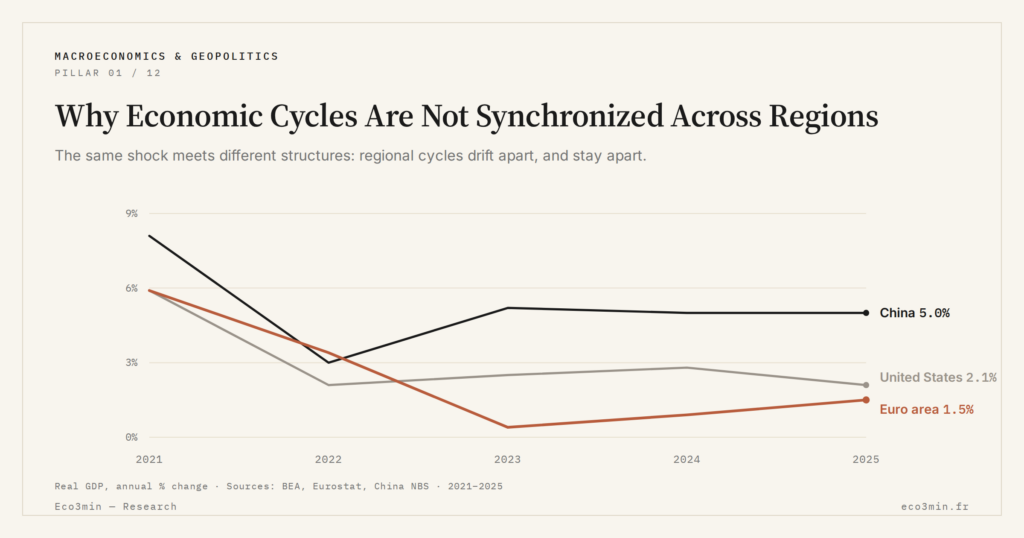

Regional cycles diverge structurally and keep widening, with US growth reaching 2.4% in Q3 2025 against 0.8% in the euro area and an estimated 4.5% in China.

- Three structural channels drive the divergence: separate Fed and ECB rate cycles, fiscal gaps like the US Inflation Reduction Act against Europe's Stability and Growth Pact limits, and contrasting productive specialization.

- The OECD noted in November 2025 that euro-area industrial production fell 2.1% year over year while US industrial production rose 0.4%.

Economic cycles are often presented as global and synchronized in media coverage. The data tell a different story: persistent lags between regions, driven by structural differences that no single global shock can erase for long. The United States, the euro area, and Asia can sit in different phases of the cycle at the same time. Treating “global economic conditions” as an operational aggregate masks the dynamics that actually drive returns, capital flows, and policy responses.

The point markets are slowly absorbing is that this divergence is not a temporary timing mismatch. Growth gaps between major regions are no longer narrowing the way they did in earlier cycles. They are stabilizing, and in several cases widening. That has consequences for the way investors price assets denominated in different currencies and for the credibility of any “global rate cycle” narrative.

A growth differential that keeps widening

In Q3 2025, the United States posted annualized growth of 2.4% (Bureau of Economic Analysis), compared with 0.8% for the euro area (Eurostat) and an estimated 4.5% for China (National Bureau of Statistics, October 2025). The spread is not a quarterly accident: it reflects different structural configurations. The U.S. economy benefits from sustained fiscal support and a more flexible labor market. The euro area is still absorbing the energy crisis and a monetary tightening cycle that bears more heavily on an economic fabric dominated by bank-financed SMEs. Related explainer: how growth patterns differ between India and China.

The real economic cycle and its deep determinants explain why these divergences persist. When investment patterns, productivity trajectories, and credit structures differ fundamentally across regions, the same shocks — higher rates, trade tensions, the energy transition — do not produce the same effects. Desynchronization is not a cyclical accident; it is the visible surface of lasting productive divergences. A related answer: how demographics shape economic cycles.

Three structural channels of divergence

The first channel is monetary policy. The Fed and the ECB are not operating in the same inflationary context, nor under the same institutional constraints. The gap between their rate cycles — with the Fed beginning its tightening earlier and signaling its first cuts sooner — creates diverging financial conditions that spread through exchange rates, capital flows, and domestic credit conditions. A simultaneous reading of both central banks as a single “global monetary stance” misses the spread that is actually pricing into the dollar and into cross-border funding costs.

The second channel is fiscal policy and its interaction with the cycle. The Inflation Reduction Act in the United States injected a massive sectoral stimulus with no equivalent in Europe, where Stability and Growth Pact rules cap fiscal room for maneuver. Each cycle therefore carries its own institutional singularities, which makes direct comparisons between regions less informative than they appear. Two recessions of similar amplitude may rest on entirely different fiscal architectures — and produce different recovery paths.

The third channel is productive specialization. Germany, exposed to heavy industry and Chinese exports, does not move through the cycle under the same conditions as the United States, which is more driven by services and technology. The OECD noted in November 2025 that euro area industrial production had fallen 2.1% year over year, while U.S. industrial production rose 0.4%. That sectoral divergence propagates through the wider cycle and shows up in earnings, capex, and labor demand long before it surfaces in headline GDP.

- Cycle desynchronization across major regions is not a temporary lag but the visible surface of distinct productive, financial, and institutional structures.

- Monetary policy, fiscal policy, and sectoral specialization are the three main channels of cyclical divergence.

- Any broad cyclical reading that aggregates the U.S., Europe, and Asia risks masking decisive local dynamics — including those that price into FX and cross-border funding.

What this means for reading the cycle

A large systemic shock — a global financial crisis, a pandemic, a generalized trade conflict — can temporarily resynchronize cycles by forcing a simultaneous adjustment. That is what happened in 2020. But these episodes remain the exception. Once the initial shock fades, the fundamental mechanisms shaping the cycle reassert themselves and trajectories diverge again.

The practical implication for any cross-region reading is straightforward: a single global indicator carries less and less information about local conditions. The variables worth tracking — bank lending surveys, regional PMIs, fiscal stance indicators, and the spread between major central bank policy rates — have to be read region by region, then layered, rather than averaged. The aggregate hides what the spread shows.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…