Yield Curve Inversion: How the Credit Channel Triggers Recessions

Yield-curve inversion occupies a special place among leading indicators. Yet the real mechanism linking this signal to cyclical reversals — the bank-credit channel — remains largely misunderstood.

The yield curve does not predict recession — it causes it, via credit.

Yield-curve inversion is not a mere statistical indicator: it represents a causal mechanism that compresses bank intermediation margins, chokes the credit channel, and produces a slowdown in the real economy with a structural lag of 6 to 24 months.

What distinguishes this signal from other leading indicators is that it does not only correlate with past recessions — it identifies the mechanism by which monetary tightening turns into an activity contraction. The yield curve is the thermometer of the credit cycle. This mechanism alters how we time investment decisions, fiscal policy, and asset allocation.

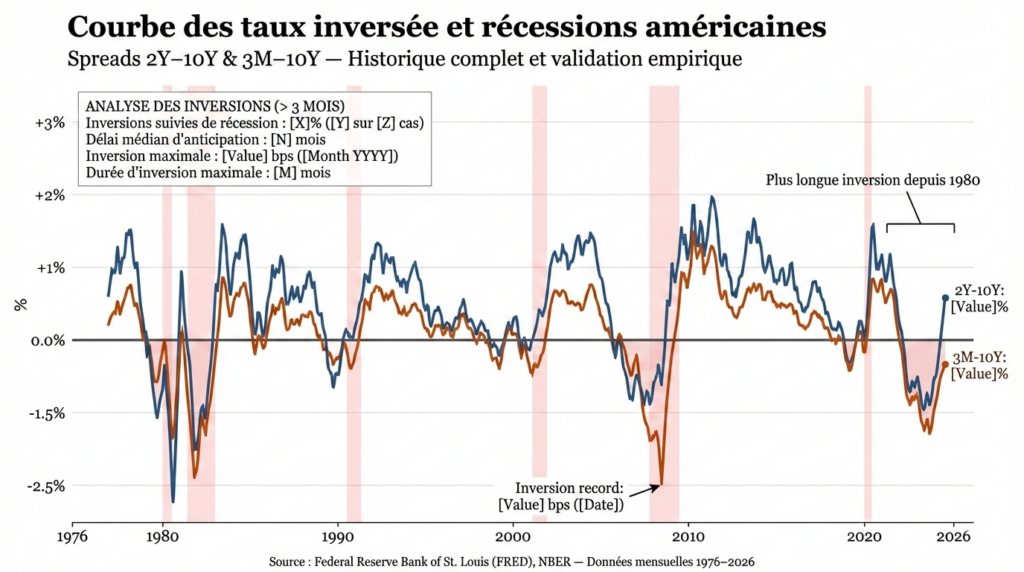

Since the 1970s, every prolonged inversion of the 2-year/10-year or 3-month/10-year spread in the United States has preceded an NBER-dated recession. This predictive record is unmatched among macro indicators. Yet debate about the yield curve remains stuck between two reductive readings: the mechanical reading (“the curve inverts, therefore a recession follows”) and the skeptical reading (“this time is different”). Both miss the essential point: the causal mechanism by which inversion transmits to the real economy — the bank-credit channel.

When short rates exceed long rates, banks’ intermediation margins compress. Banks, whose business model rests on maturity transformation (borrow short, lend long), see profitability erode — which leads them to tighten lending conditions, independently of any central-bank directive. This endogenous credit contraction is what turns a market signal into a real slowdown. The yield curve is therefore not an instantaneous cyclical indicator but an intertemporal synthesis of growth expectations, monetary policy expectations and term premium — and reading it through the credit cycle reveals its causal scope.

The yield curve does not predict recession — it causes it, via credit. Inversion compresses bank intermediation margins, which triggers an endogenous tightening of lending standards independent of monetary-policy instructions. This mechanism — formalized by Bernanke & Blinder (1988) and empirically documented by the New York Fed (Estrella & Mishkin, 1998) — preceded each of the seven U.S. recessions since 1970, with a lag of 6 to 24 months. The prolonged inversion of 2022–2024 was the longest since 1980. The causal chain (inversion → margin compression → credit contraction → slowdown) is well established; the open question is how it calibrates in a cycle marked by strong bank balance sheets and unprecedented fiscal buffers.

Why an inverted yield curve almost always ends in recession

The relationship between yield-curve inversion and recession is not a mysterious statistical correlation: it rests on an identifiable causal chain whose central link is the bank-credit channel.

Yield-curve inversion → Bank NIM ↓ → Credit ↓ → Investment ↓ → Recession

Transmission lag: 6 to 24 months. Each link is independently observable in the data.

Trigger: the slope reversal of the curve. In normal conditions the yield curve is upward-sloping: long-term yields exceed short-term yields, reflecting a term premium (compensation for uncertainty at longer maturities) and expected nominal growth. Inversion occurs when tightening pushes short rates above long rates — signalling that markets expect either future growth below current growth or monetary easing ahead in response to an anticipated slowdown. The 2Y–10Y U.S. spread turned negative in July 2022 and remained negative for more than two years — the longest inversion since 1978–1980, per FRED (St. Louis Fed) data.

Transmission channel: compression of bank intermediation margins. The pivotal mechanism runs through commercial banks’ economic model, based on maturity transformation: banks fund short (deposits, interbank market) and lend long (mortgages, corporate loans). When the curve inverts, short-term funding costs exceed yields on long loans — net interest margins (NIM) compress. This mechanism was formalized in a seminal Fed working paper (Bernanke & Blinder, 1988, “Credit, Money, and Aggregate Demand”) and empirically confirmed by Estrella & Mishkin (1998, New York Fed). FDIC data show aggregate U.S. bank NIM fell by roughly 30 basis points between the 2023 peak and end-2025, from 3.3% to about 3.0% — a meaningful compression weighing directly on lending profitability.

Amplifier: endogenous tightening of lending standards. Margin compression does not only reduce bank profitability: it triggers an autonomous tightening of lending standards. Facing squeezed margins, banks become more selective — shortening offered maturities, increasing collateral requirements, excluding the riskiest profiles. This tightening occurs independently of central-bank instructions: it is a rational bank response to an environment in which credit becomes less profitable. The ECB Bank Lending Survey (Q4 2025) confirms this mechanism: net tightening of lending standards for corporate loans continued into its ninth consecutive quarter in the euro area, with a significant share of banks citing margin compression as a driving factor. The BIS (annual report 2025) formalizes this dynamic under the “bank lending channel”: the way monetary policy transmits to the economy not primarily via rates but via the quantity and quality of credit supplied.

Macro consequence: slowdown via credit contraction. Reduced credit supply diffuses to the real economy following the sequence documented in the analysis of restrictive monetary policy and delayed effects: financial conditions tighten first, credit flows contract next, investment slows, and employment adjusts last. The lag between inversion and the official recession start (NBER) ranged between 6 and 24 months over the last seven cycles — a range explained by varying buffers (corporate balance sheets, household savings, fiscal impulses) but never invalidating the causal mechanism itself.

- 7 out of 7: every prolonged 2Y–10Y inversion since 1970 preceded an NBER recession. Source: FRED, NBER.

- Average lag: 6 to 24 months between initial inversion and official recession onset. Source: Estrella & Mishkin, 1998, New York Fed.

- 2022–2024 inversion: ~26 months in negative territory, the longest since 1978–1980. Source: FRED (T10Y2Y series).

- U.S. bank NIM: decline of ~30 bps between 2023 and end-2025 (from 3.3% to ~3.0%). Source: FDIC.

- 1 possible false positive: the brief 1998 inversion was not followed by an immediate recession (but by a market crisis — LTCM). Source: NBER.

What the consensus gets right — and the mechanism it overlooks

The dominant reading, voiced by a significant fraction of market economists and large investment-bank outlooks, argues reasonably that the yield curve’s predictive power may have eroded. Unconventional policies (QE) allegedly distorted long yields, excess savings after the pandemic may have delayed transmission, and stronger bank balance sheets might reduce credit sensitivity to margin compression. The central scenario — a soft landing — assumes these buffers are sufficient to break the historical causal chain.

This diagnosis has merit. Banks’ balance sheets are indeed stronger than in 2007 (CET1 ratios of major U.S. banks near 13% end-2025 vs. 8% in 2007, Fed data). Excess household savings served as a temporary buffer, though ECB estimates indicate much of it has been drawn down in the euro area. Fiscal impulses (Infrastructure Investment and Jobs Act in the U.S., European recovery plans) have partially offset tightening — but their effects are fading.

However, the “this time is different” reading underestimates one structural point: buffers determine how long the mechanism takes to materialize, not whether it will. The credit channel is slowed, not neutralized.

Analysis of the economic-cycle structure as revealed by the yield curve suggests the relevant question is not “will inversion precede a recession this time?” but “how fast and with what intensity does the credit channel transmit the signal?” Bank Lending Survey data and NIM evolution indicate transmission is underway — merely slower than in previous cycles.

Expecting a rapid macro pivot after inversion and declaring the signal invalid if a slowdown does not materialize within months. Inversion produces its effects via progressive compression of bank margins and cumulative credit tightening — a process that unfolds over 6 to 24 months. Post-inversion cyclical resilience reflects the transmission lag, not the signal’s failure. The 2000 and 2006 inversions followed the same pattern: resilient growth for quarters, then reversal.

| “This time is different” reading | Credit-channel reading | |

|---|---|---|

| Core assumption | QE and stronger balance sheets neutralized the signal | Buffers delay transmission; they do not cancel it |

| Observed signal | Post-inversion resilience of growth and employment | NIM compression, endogenous credit tightening |

| Analysis horizon | 6–12 months post-inversion | 12–30 months, with sequential accumulation |

| Main risk | Underestimating the rebound if the soft landing occurs | Underestimating delayed slowdown due to overconfidence |

| Key variable | Nominal spread, employment, GDP | Bank NIM, Bank Lending Survey, credit flows, term premium |

Buffers, non-linearities and feedback loops: why timing remains unpredictable

The causal mechanism is identifiable, but its timing depends on factors that introduce irreducible complexity.

Cyclical buffers: balance sheets, savings, fiscal support. Strong corporate balance sheets — bolstered by high profits in 2021–2023 — are the first buffer. Firms with cash reserves can sustain investment despite tighter bank credit by using internal funds or accessing bond markets. This protects large firms; SMEs reliant on bank credit do not enjoy the same shield. Excess household savings accumulated during the pandemic acted similarly but temporarily: ECB estimates (2025) suggest much of it has been depleted in the euro area, removing a protective factor. Fiscal impulses have partially compensated, but their cushioning effect is waning.

Non-linearities and threshold effects. Transmission via the credit channel is not linear. As long as bank margins stay above a minimal profitability threshold, institutions absorb compression without materially changing credit supply. But once that threshold is crossed, tightening accelerates abruptly — especially if banks anticipate portfolio-quality deterioration. Historical FDIC data show that credit contraction phases in the last five cycles were preceded by NIM declines below a ~3.0% threshold — a level recent data approach.

Credit-activity-credit feedback loop. Once triggered, credit contraction tends to be self-reinforcing: tighter credit slows activity, which weakens borrower quality, which prompts further bank tightening — the financial accelerator loop formalized by Bernanke & Gertler (1995). This feedback helps explain why recessions following inversion can be deeper than linear models predict: the shift from ordered slowdown to self-sustaining contraction is non-linear and often occurs at a point that standard indicators do not flag precisely.

Re-steepening as a complementary signal. Inversion is not the only relevant signal: re-steepening (return to a positive slope) often provides a more immediate indicator. Historically, recessions have more closely coincided with the re-steepening phase than with inversion itself — because re-steepening signals that markets now expect monetary easing in reaction to an already-underway slowdown. The 2Y–10Y spread re-steepened from mid-2024, moving back into positive territory — a signal that, in past cycles, coincided with recessionary effects materializing within the next 6–12 months.

Implications for reading the current cycle

If the credit-channel framework is valid, it changes how we interpret several ongoing dynamics.

For cyclical diagnosis. The 2022–2024 inversion — the longest in forty years — exerted unprecedented cumulative pressure on intermediation margins. The ongoing re-steepening does not signal the end of risk — in historical terms it signals the start of the materialization phase. Structural lags of macro indicators add further delay. The most relevant data to assess transmission sit in credit flows, lending standards (Bank Lending Survey) and bank margins — not in quarterly GDP, which records effects at the end of the chain.

For financial-market reading. One documented paradox is equities rising during inversion, then correcting on re-steepening — precisely when the causal mechanism begins producing real effects. This dynamic, analysed in the context of central banks and equity markets, implies the current re-steepening is a warning signal for valuations, especially in credit-sensitive segments (small caps, cyclicals, listed real estate). Market anticipation dynamics can mask real transmission for quarters.

For monetary policy. Inversion creates a structural dilemma for central banks: holding rates high to fight inflation compresses bank margins and chokes the credit channel — but easing too early risks rekindling inflation before disinflation is consolidated. This dilemma is harder because transmission occurs with delay: central banks decide on data that reflect past transmission, not its current state. Coupling with the broader monetary-policy and interest-rate framework confirms the dilemma is structurally insoluble.

Invalidation condition. This framework would be invalidated if rapid easing restored a normal positive slope and stabilized bank margins before credit contraction reached its peak impact — a “successful soft landing” scenario compatible with current data but not guaranteed. It would also be invalidated if a productivity shock (AI) or massive fiscal impulse offset credit contraction via alternative financing channels. Conversely, a return of inflation forcing prolonged high short rates would amplify margin compression and accelerate recessionary materialization.

Three horizons to monitor signal transmission

Short horizon (0–6 months): re-steepening is underway, which historically coincides with the start of recessionary effects materializing. Priority indicators: bank NIMs (FDIC, ECB), Bank Lending Survey (standards and tightening motives), corporate credit flows, and the evolution of the 10-year term premium (ACM model, New York Fed). Short-term risk is non-linear crystallization if NIMs fall below minimal profitability thresholds in the most exposed banks.

Cycle horizon (1–3 years): the decisive question is the speed at which the curve’s slope normalizes and whether it restores margins before the credit-activity loop fully engages. If easing is sufficient and bank balance sheets hold, a soft landing remains feasible — but credit slowdown will weigh on potential growth. Interaction with the real economic cycle and investment dynamics will determine whether adjustment remains orderly. Desynchronization of cycles adds complexity: U.S. and European curve signals are offset, making global reading ambiguous.

Structural horizon (5+ years): the current cycle tests the yield curve’s predictive power in a post-QE world. If the credit-channel mechanism holds despite novel buffers, it will validate the signal’s structural robustness over half a century of data. If instead a full soft landing occurs without recession, academic debate must determine whether buffers temporarily neutralized the credit channel or whether banking maturity transformation has structurally changed under a higher-rate regime. This raises questions about the structural limits of monetary policy.

The yield curve does not merely correlate with recessions — it causes them via the bank-credit channel. Inversion compresses intermediation margins, which triggers endogenous credit tightening and slows the real economy with a 6–24 month lag. Post-inversion resilience reflects the transmission delay, not signal invalidation. Current re-steepening historically signals imminent materialization — not normalization. Buffers (strong balance sheets, fiscal impulses) lengthen the lag and may reduce amplitude, but do not break the causal chain.

Robust: The inversion’s predictive power is documented across seven cycles since 1970 (Estrella & Mishkin, 1998; New York Fed). The causal channel via bank-margin compression and credit tightening is theoretically formalized (Bernanke & Blinder, 1988) and empirically supported by Bank Lending Surveys and NIM data (FDIC). Re-steepening as a materialization signal is consistent with the last five cycles.

Uncertain: The effectiveness of current buffers (post-2010 bank balance sheets, fiscal impulses, bond-market substitution for bank credit) to permanently break the causal chain is not decided. Precise calibration of the lag in the current cycle is uncertain — the 6–24 month amplitude makes precise dating impossible. The role of the term premium (compressed by past QE) in distorting the signal remains academically contested. A complete soft landing — the first exception in five decades — remains possible.

Regular monitoring of the weekly macro checkpoint allows this framework to be confronted with the latest bank-margin, credit and financial-condition data. Several trajectories remain open, but reading inversion through its causal mechanism — the credit channel — provides a more robust framework than observing the curve’s shape alone to anticipate the timing and intensity of transmission to the real economy.

- Yield-curve inversion does more than correlate with recessions — it identifies the causal mechanism: compression of bank intermediation margins triggers endogenous credit tightening that slows the real economy.

- The empirical record is unparalleled: 7 prolonged inversions out of 7 preceded an NBER recession since 1970, with a 6–24 month lag.

- Post-inversion cyclical resilience illustrates transmission lags (cyclical buffers), not signal invalidation. Buffers delay materialization; they do not neutralize the mechanism.

- Current re-steepening historically signals imminent materialization of recessionary effects — not normalization.

- This framework is invalidated if a complete soft landing occurs — the first exception in five decades — or if bond markets sufficiently substitute for bank credit to neutralize the transmission channel.

Mis à jour : 30 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.