Investment Discipline and Long-Term Portfolio Performance

Decision discipline is the most underestimated performance driver in portfolio management. Not as an abstract virtue, but as a concrete mechanism for reducing cumulative errors—an advantage whose value is measured in annual percentage points over a full market cycle.

How Decision Discipline Generates 3 to 4 Points of Annual Performance

Long-term performance depends more on mistakes avoided than on gains achieved.

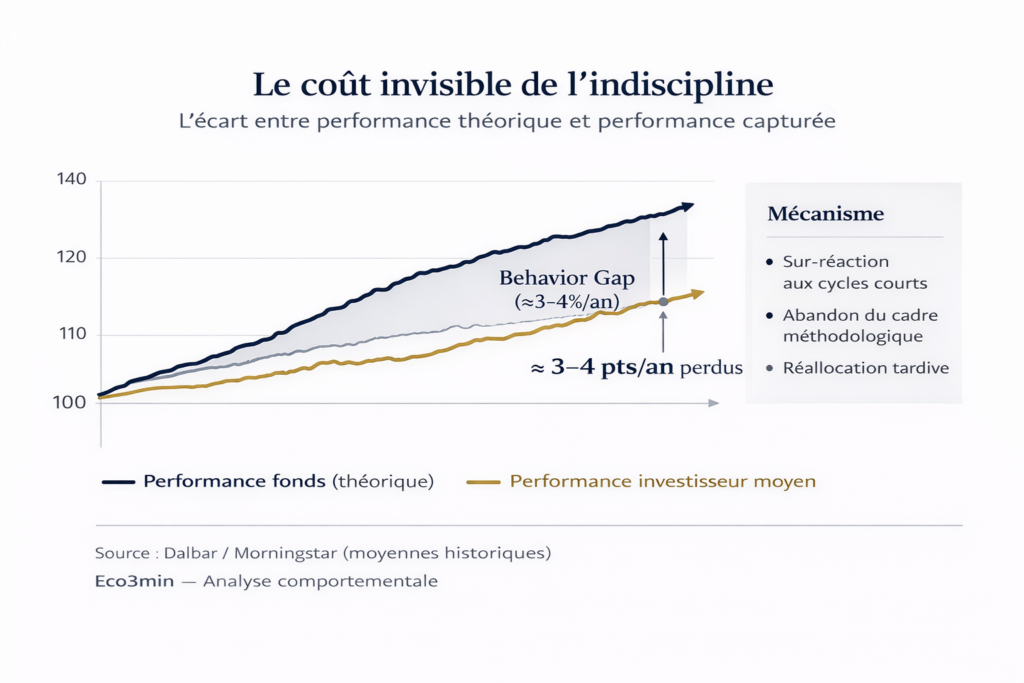

Empirical studies document a systematic gap of 3 to 4 annual percentage points between investment fund returns and the returns actually captured by investors. This gap—the “behavior gap”—primarily results from poor market timing decisions, excessive trading, and emotional reactions to market fluctuations. Decision discipline is not an alternative strategy: it is the meta-framework on which the robustness of all strategies depends.

This mechanism is even more decisive in the current cycle—marked by conflicting macroeconomic signals, frequent narrative reversals, and high regime volatility—where the temptation for constant adjustment reaches its peak. For asset allocators and portfolio managers, understanding that discipline creates value through subtraction (mistakes avoided) rather than addition (gains achieved) changes how performance and risk are assessed. This article analyzes the mechanisms through which decision consistency generates performance over a full cycle.

Some portfolios move through market cycles without ever attracting attention. Never celebrated during euphoric phases, never singled out during corrections, they accumulate performance periods with a consistency many would consider dull. Yet by the end of a full cycle, their cumulative return matches—if not exceeds—that of the most discussed strategies. This paradox is no accident: it reflects a mechanism documented by behavioral finance since the 1990s. According to Dalbar’s annual studies (Quantitative Analysis of Investor Behavior, 2025), the average investor in U.S. equity funds captured roughly 6.5% in annual returns over the past 20 years, versus about 10% for the S&P 500 over the same period—a cumulative wealth gap exceeding 50% over two decades, attributable almost entirely to timing and behavioral mistakes. Morningstar (Mind the Gap, 2024) confirms these magnitudes using a different methodology.

This observation fits within the broader framework of investment strategies, where discipline forms the invisible foundation—the meta-framework that determines the robustness of all approaches, whether factor-based, tactical, or passive.

- The gap between fund returns and investor-captured returns reaches 3 to 4 points per year—the “behavior gap”

- This gap mainly results from timing decisions, overtrading, and emotional reactions—not from an analytical deficit

- Discipline does not generate visible outperformance—it works through subtraction: reducing cumulative errors over a full cycle

Long-term performance depends more on mistakes avoided than on gains achieved. The “behavior gap”—the 3 to 4 annual point difference between theoretical returns and captured returns—represents the empirically measured cost of decision indiscipline. This cost results from three documented mechanisms: poor timing decisions (buying high, selling low), excessive trading activity (friction costs and cumulative errors), and emotional reactions to volatility (abandoning the framework under stress). Discipline is not a moral virtue—it is a concrete value-creation mechanism through error subtraction. This framework is documented in the work of Kahneman (2011), Thaler (2015), Dalbar studies (1990–2025), and Morningstar (Mind the Gap, 2024); its magnitude in the current cycle—marked by elevated regime volatility—may be greater than in previous cycles.

The Core Mechanism: How Indiscipline Destroys Value

The behavior gap is not an abstract concept: it rests on an identifiable causal chain, each link documented by behavioral finance and empirical performance data.

Ambiguous market signal (volatility, conflicting narratives) → Activation of cognitive biases (loss aversion, overconfidence, recency bias) → Timing decision (late entry / panic selling / rushed reallocation) → Friction costs + positioning error → Cumulative underperformance over the cycle

Measured cost: 3 to 4 annual percentage points. Over 20 years: more than 50% of wealth lost versus maintaining the initial allocation.

Trigger: cognitive biases as sources of systematic errors. The starting point is not an information deficit but a processing failure. Foundational work by Kahneman and Tversky (1979, “Prospect Theory”) and later Kahneman (2011, “Thinking, Fast and Slow”) documents cognitive biases that systematically affect financial decisions: loss aversion (the pain of loss is about 2.5 times stronger than the pleasure of an equivalent gain), recency bias (overweighting recent events in expectations), overconfidence (overestimating the ability to anticipate turning points), and the disposition effect (selling winners too early and holding losers too long). These biases are not individual anomalies—they are structural features of human cognition, present among professional and retail investors alike. Thaler and Sunstein (2008, “Nudge”) and Thaler (2015, “Misbehaving”) showed that these biases generate predictable and systematic investment decision errors.

Transmission channel: timing decisions as a vector of value destruction. Cognitive biases translate into timing decisions—the moment of buying, selling, or reallocating—that systematically destroy value. This mechanism is empirically documented by Dalbar studies (QAIB, 1990–2025): the average investor enters markets after rallies (attracted by recent performance—recency bias) and exits after declines (driven by loss aversion). This behavioral pattern—buy high, sell low—is the exact opposite of what rational strategy prescribes. Morningstar (Mind the Gap, 2024) refines this analysis fund by fund: the most volatile funds show a wider behavior gap (4–5 points) than less volatile funds (1–2 points), confirming that emotional bias is amplified by asset volatility. Misleading economic indicators and narrative reversals amplify this phenomenon by creating conflicting signals that prompt action.

Amplifier: excessive trading activity. Beyond timing, the frequency of decisions itself amplifies the behavior gap. A working paper by Barber and Odean (2000, “Trading Is Hazardous to Your Wealth,” Journal of Finance) shows that the most active investors underperform the least active by 6–7 annual percentage points—explained by transaction costs, selection errors, and the accumulation of timing mistakes across numerous decisions. Excessive activity is not a symptom of expertise—it is an empirically documented driver of value destruction. This mechanism intensifies during fragmented market phases (conflicting signals, regime volatility), when the temptation to react to every perceived shift is strongest.

Consequence: a massive cumulative gap over a full cycle. The combination of these channels produces a cumulative gap whose magnitude is striking: 3 to 4 points annually, compounded over 20 years, represents a wealth differential exceeding 50%. An investor who simply maintained their initial allocation in an S&P 500 index fund from 2005 to 2025 would have accumulated roughly twice the wealth of the average investor measured by Dalbar—without any active decisions, macro analysis, or tactical adjustments. This result does not prove that analysis is useless—it shows that the value of discipline (mistakes avoided) exceeds that of analysis (gains achieved) for most investors.

Same market exposure. Two behaviors. Structurally divergent outcomes.

- Disciplined approach: broad index exposure maintained long term, systematic rebalancing, no discretionary decisions.

- Discretionary approach: market entries and exits based on macro news flow, sentiment, and recent performance.

Long-term observed orders of magnitude:

• U.S. equity market performance: ≈10% annualized

• Average investor performance: ≈6–7% annualized

Behavior gap: ≈3–4 points per year (“behavior gap”).

Compounding effect: a major wealth differential over 20 years.

Sources: Dalbar — Quantitative Analysis of Investor Behavior (2025); Morningstar — Mind the Gap (2024). Index: S&P 500.

The gap primarily results from timing decisions and overtrading, not from insufficient exposure to risky assets.

- Average annual behavior gap: 3 to 4 percentage points in U.S. equity markets (past 20 years). Source: Dalbar QAIB, 2025.

- Average investor vs S&P 500 return: ~6.5% vs ~10% annualized over 20 years. Source: Dalbar, 2025.

- Cumulative wealth lost: > 50% over 20 years (compounding effect). Source: Eco3min calculations based on Dalbar.

- Overtrading: most active investors underperform least active by 6–7 points/year. Source: Barber & Odean, 2000, Journal of Finance.

- Volatility and behavior gap: most volatile funds show 4–5 point gaps vs 1–2 points for least volatile. Source: Morningstar Mind the Gap, 2024.

What the Consensus Celebrates — and the Invisible Value It Ignores

The dominant narrative around investment performance, promoted by the asset management industry and echoed by financial media, focuses on outperformance: alpha, stock picking, market timing, tactical allocation. The story celebrates the “star” manager who anticipates turning points, the strategist who identifies the right sector at the right time, the analyst who spots undervalued gems. This narrative is not unfounded—alpha exists and is documented in academic literature—but it is rare, unstable, and difficult to reproduce.

What this narrative systematically ignores is the value of what is not done. Long-term performance is built as much on mistakes avoided as on gains achieved. Yet avoided mistakes are invisible: they appear in no performance report, no fund ranking, no market newsletter. The portfolio that was not panic-sold in March 2020, not overexposed to growth stocks in late 2021, not massively reallocated into commodities in 2022—these non-decisions created more value than most active trades, yet their contribution is structurally invisible in standard metrics.

The consensus conflates two fundamentally distinct sources of performance: performance by addition (gains achieved through active decisions) and performance by subtraction (value preserved by avoiding mistakes). Empirical data (Dalbar, Morningstar, Barber & Odean) show that for most investors, the latter overwhelmingly dominates the former—a result that challenges the skill hierarchy presented by the industry.

Interpreting discipline as inertia or an admission of analytical weakness. Decision discipline is not the absence of decisions—it is the deliberate choice not to react to signals that do not justify changing the framework. In fragmented market environments (conflicting signals, narrative reversals), the temptation for constant adjustment peaks—and it is precisely during these phases that discipline creates the most value. Markets penalize inconsistency more severely than the absence of brilliant anticipation.

| “Performance by addition” view | “Performance by subtraction” view | |

|---|---|---|

| Source of value | Gains achieved (alpha, timing, selection) | Mistakes avoided (non-reaction, process consistency) |

| Visibility | High (rankings, communication, media) | None (not captured by standard metrics) |

| Repeatability | Low (alpha unstable, non-persistent) | High (formalized process, cycle-consistent) |

| Cost of absence | Potential opportunity cost | 3–4 annual points of value destruction (behavior gap) |

| Required skillset | Analysis, anticipation, conviction | Process discipline, consistency, tolerance for discomfort |

The consensus conflates two fundamentally distinct sources of performance: performance by addition (gains achieved through active decisions) and performance by subtraction (value preserved by avoiding mistakes). Empirical evidence (Dalbar, Morningstar, Barber & Odean) shows that, for the majority of investors, the latter overwhelmingly dominates the former—a finding that challenges the hierarchy of skills as presented by the asset management industry.

Interpreting discipline as inertia or as an admission of analytical weakness. Decision discipline is not the absence of decisions—it is the deliberate choice not to react to signals that do not justify a change in framework. In fragmented market environments (conflicting signals, narrative reversals), the temptation to adjust continuously is at its peak—and it is precisely in these phases that discipline creates the most value. Markets penalize inconsistency more severely than the absence of brilliant anticipation.

| “Performance by addition” view | “Performance by subtraction” view | |

|---|---|---|

| Source of value | Gains achieved (alpha, timing, selection) | Mistakes avoided (non-reaction, process consistency) |

| Visibility | High (rankings, marketing, media) | None (absent from standard metrics) |

| Repeatability | Low (alpha is unstable, non-persistent) | High (formalized process, cycle-consistent) |

| Cost of absence | Potential opportunity loss | 3–4 annual percentage points of value destruction (behavior gap) |

| Required skillset | Analysis, anticipation, conviction | Process discipline, consistency, tolerance for discomfort |

Cognitive Biases, Market Phases, and the Macro Environment: What Makes Discipline Harder

The behavior gap mechanism is amplified by contextual factors that alter its intensity depending on the phase of the cycle and the market environment.

Fragmented market phases as the strongest amplifier. Contrary to intuition, discipline does not make the greatest difference during clear-cut crises. The most destructive environments for undisciplined investors are characterized by rapid sequences of contradictions: failed rebounds, technical pullbacks without follow-through, diverging macro signals, and repeated narrative reversals. This type of configuration—similar to the 2022–2025 period, marked by constant revisions to rate expectations and sentiment swings—encourages frequent reallocations, each carrying friction costs and error risk. Regime volatility (uncertainty about the framework itself) then exceeds price volatility (fluctuations within a stable framework)—and it is this regime volatility that generates the most costly mistakes. Monetary policy inflections, notably through the channel of real interest rates, amplify this cognitive instability by altering the valuation framework itself.

The institutional dimension of the behavior gap. The behavior gap is not limited to individual investors. Morningstar studies show it also affects institutional investors—pension funds, endowments, insurers—albeit to a lesser extent (1–2 percentage points annually). The causes are partly different: benchmark pressure, quarterly reporting constraints, investment committees reacting to recent performance, and mandates enforcing procyclical reallocations. Institutional frameworks designed to control risk can paradoxically amplify the behavior gap by institutionalizing short-term reactions.

Interaction with the macro cycle. The behavior gap is not constant throughout the economic cycle. It widens during turning points (when dominant narratives shift and investors reallocate massively) and narrows during established trend phases (when holding positions feels comfortable). The current cycle—marked by positive real rates, incomplete monetary normalization, and conflicting cyclical signals—creates an environment particularly conducive to a wider behavior gap. Interaction with the lagged effects of restrictive monetary policy creates a disconnect between macro signals (ongoing slowdown) and market performance (resilient indices), prompting contradictory reallocations.

Discipline as a Meta-Strategy: The Invisible Foundation of All Approaches

Discipline is not an alternative investment strategy to factor, momentum, value, or hedging approaches. It is the meta-framework on which all these strategies depend to deliver durable results. Tactical allocation, quantitative approaches, and defensive strategies only generate performance when embedded in a stable, formalized decision framework maintained consistently over time. Choosing a strategy is an investment decision; maintaining it through cycles is a higher-order structural decision.

In practice, this framework is defined as much by what it forbids as by what it prescribes. Discipline manifests through the deliberate refusal to increase exposure when favorable signals accumulate (resistance to confirmation bias), strict adherence to rules when relative performance temporarily disappoints (tolerance for discomfort), and the conscious decision not to fully exploit favorable phases (preference for consistency over maximization). This framework can be operationalized through portfolio risk management mechanisms that formalize intervention thresholds, rebalancing rules, and tolerance criteria.

Implications for Reading the Current Cycle

For portfolio management. The 2025–2026 environment—conflicting macro signals, high regime volatility, frequent narrative reversals—creates conditions where the behavior gap is mechanically wider than during established trend cycles. The value of discipline is highest precisely when it is hardest to maintain. Morningstar data show that funds with the lowest turnover ratios (a proxy for discipline) outperform high-turnover funds by 1–2 percentage points annually on average, net of fees—a gap that widens in fragmented market phases.

For performance assessment. Fund rankings and manager league tables measure performance by addition (alpha, absolute returns) but structurally ignore performance by subtraction (mistakes avoided). This metric asymmetry creates a systematic bias favoring highly visible active strategies over disciplined low-turnover approaches. Market anticipation dynamics confirm that the anticipation mechanism (markets turning before the data) makes timing decisions structurally unfavorable for the average investor—because inflection points occur when the dominant narrative is most persuasive in the opposite direction.

For building investment processes. The behavior gap framework implies that the investment process (how and when decisions are made) matters more than decision content (what to buy or sell). A mediocre process applied with discipline will outperform an excellent process applied erratically—a counterintuitive but empirically documented result. Quality criteria for a disciplined process are observable: explicit allocation rules, predefined intervention thresholds, fixed rebalancing frequency, documented exception criteria, and bias-control mechanisms (pre-commitment, decision committees, decision journals).

Invalidation condition. This analytical framework loses relevance in a market configuration where a structural shock (abrupt monetary regime shift, systemic crisis, technological disruption) renders the initial allocation framework fundamentally obsolete—not merely uncomfortable. Discipline does not protect against an analytical framework that remains wrong for too long: a disciplined process built on false assumptions will produce consistently poor results. The validity condition is that the underlying framework remains relevant—requiring periodic framework reviews distinct from tactical adjustments within the framework. Analysis of the real economic cycle provides tools to assess whether a regime change justifies a framework revision.

Three Time Horizons for Investment Discipline

Short-term horizon (0–6 months): discipline is measured by the ability not to react to contradictory signals in the current cycle. Internal discipline indicators to monitor: portfolio turnover frequency, deviation between actual and target allocation, and the number of decisions triggered by isolated data releases versus those executed under the predefined process. The short-term risk is a widening behavior gap if divergence between resilient markets and deteriorating macro signals leads to hasty reallocations.

Cycle horizon (1–3 years): the structural issue is the ability to maintain the allocation framework through a full cycle turn—from the end of monetary tightening to the materialization of its lagged effects. Historical data show the behavior gap widens by an additional 1–2 points during turning phases (Dalbar, 2025). Investors who maintain their framework through the cycle trough mechanically capture the rebound that follows—the rebound undisciplined investors miss because they sold during stress phases.

Structural horizon (5 years and beyond): discipline is a necessary (but not sufficient) condition for capturing compounded returns over a full cycle. The compounding effect on the behavior gap is massive: 3.5 annual points compounded over 20 years represent a wealth differential exceeding 100% (a doubling). At this horizon, investment discipline is not a performance issue—it is a wealth formation issue. Regular monitoring of the weekly macro dashboard provides a consistent framework to distinguish signals that justify framework revision from fluctuations that can be absorbed without adjustment.

Long-term performance depends more on mistakes avoided than gains achieved. The behavior gap—3 to 4 annual percentage points of value destruction due to decision indiscipline—is the largest and most invisible cost borne by most investors. Discipline does not produce spectacular outperformance: it operates by subtraction, reducing the accumulation of timing errors, overtrading, and emotional reactions. Its value is highest during fragmented market phases (conflicting signals, regime volatility)—precisely when it is hardest to maintain. A mediocre process applied consistently will outperform an excellent process applied erratically—the most counterintuitive and best-documented finding of behavioral finance.

Robust: The 3–4 percentage point annual behavior gap has been documented by Dalbar since 1990 across more than 30 years of data. Underlying cognitive biases (loss aversion, recency bias, overconfidence) are formalized by Prospect Theory (Kahneman & Tversky, 1979) and confirmed by decades of experimentation. The destructive effect of overtrading is documented by Barber & Odean (2000). The correlation between asset volatility and behavior gap magnitude is confirmed by Morningstar (Mind the Gap, 2024).

Uncertain: The exact magnitude of the behavior gap in the current cycle depends on the intensity of conflicting signals and the duration of the transition phase. The transferability of results (primarily measured in US markets) to other geographies is partial—market structures, investment cultures, and regulatory frameworks differ. The ability of automation (robo-advisors, automatic rebalancing) to structurally reduce the behavior gap remains under evaluation—early data suggest reduction but not elimination. The distinction between “productive discipline” (maintaining a relevant framework) and “costly stubbornness” (maintaining an obsolete framework) remains a judgment that cannot be fully formalized algorithmically.

Reading performance through the behavior gap—rather than active outperformance—provides a more robust analytical framework to assess the real contribution of investment discipline and identify the conditions under which it creates the most value. This framework forms the invisible foundation of investment strategies—the meta-framework on which the robustness of all approaches depends.

- The behavior gap—the 3–4 annual percentage point difference between fund returns and investor-captured returns—is the empirically measured cost of decision indiscipline. Over 20 years: more than 50% of wealth lost.

- Long-term performance depends more on mistakes avoided (non-reaction, consistency) than on gains achieved (timing, selection)—a counterintuitive result documented over 30 years of data.

- Discipline is not the absence of decisions—it is the deliberate choice not to react to signals that do not justify a framework change. Markets penalize inconsistency more severely than the absence of brilliant anticipation.

- The behavior gap widens in fragmented market phases (conflicting signals, regime volatility)—precisely when discipline is hardest to maintain and most value-creating.

- This framework is invalidated if a regime shift renders the allocation framework fundamentally obsolete (not merely uncomfortable)—discipline applied to a flawed framework produces consistently poor results.

Frequently Asked Questions About Investment Discipline

Does investment discipline mean never changing a portfolio?

No. Discipline does not mean inertia—it means that changes follow predefined rules (scheduled rebalancing, deviation thresholds, periodic framework reviews) rather than reactions to market events. The key distinction is between systematic adjustments (process-driven) and discretionary adjustments (emotion- or narrative-driven).

Does the behavior gap also affect professional investors?

Yes, though to a lesser extent. Morningstar studies show a 1–2 annual percentage point behavior gap among institutional investors. Causes are partly different (benchmark pressure, reporting constraints, procyclical committees), but the core mechanism—reaction to recent performance and overactivity—remains the same.

Do robo-advisors eliminate the behavior gap?

Early evidence suggests automated rebalancing reduces the behavior gap (by removing emotional decisions) but does not eliminate it—because investors still retain the ability to close accounts or change settings during stress periods. Robo-advisors treat the symptom (overactivity) but not the cause (cognitive biases), which reappear at a higher level (the decision to stay with or leave the robo-advisor).

When does discipline become costly stubbornness?

Discipline creates value when the underlying allocation framework remains relevant and fluctuations reflect normal cycle noise. It becomes stubbornness when a fundamental regime shift (not a fluctuation) renders the framework obsolete. The distinction is analytical, not emotional: it depends on assessing whether structural assumptions (rate regime, cycle phase, economic structure) have changed—not whether markets have moved in an uncomfortable direction.

Mis à jour : 20 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.