Monetary Policy Transmission: Channels, Time Lags and Real-Economy Impact

Monetary policy does not act immediately or uniformly. Central bank decisions first alter financial variables — cost of credit, liquidity conditions, expectations — which only with delay and unevenly transmit to the real economy.

Monetary policy does not strike the economy — it soaks through it.

Monetary transmission is the process by which central bank decisions gradually diffuse into the real economy through financial conditions, credit, balance sheets and expectations.

This mechanism works with a lag and heterogeneously across agents and national financial structures, which makes cyclical diagnosis more complex than a simple reading of rate announcements.

When a central bank raises its policy rate the public debate often assumes a near-mechanical chain: borrowing becomes more expensive, demand slows, inflation falls. That sequence is technically correct — and profoundly misleading about timing. Because between the rate decision and its tangible effect on employment, output or consumption lie transmission lags measured in quarters, not weeks. The paradox is this: monetary policy is the most powerful macro tool available to advanced economies, yet its action is the slowest, the most indirect and the most unevenly distributed.

This delay is not a system defect — it is the system. Monetary policy does not directly pilot activity: it changes the conditions under which economic agents decide. Its action transits via credit, balance sheets, expectations and the exchange rate, each channel operating at its own speed and with its own intensity depending on the financial architecture of each economy. Confusing the announcement of a rate hike with its real effect leads to two symmetric errors: prematurely declaring victory when inflation moderates, or concluding failure when activity holds in the months following the tightening.

For a theoretical approach to monetary policy — seen as a system of incentives and constraints — see our deep-dive: Monetary policy: incentive framework and structural limits. This article focuses on the concrete mechanics of transmission: how, through which channels and at what speed monetary decisions ultimately affect the productive economy.

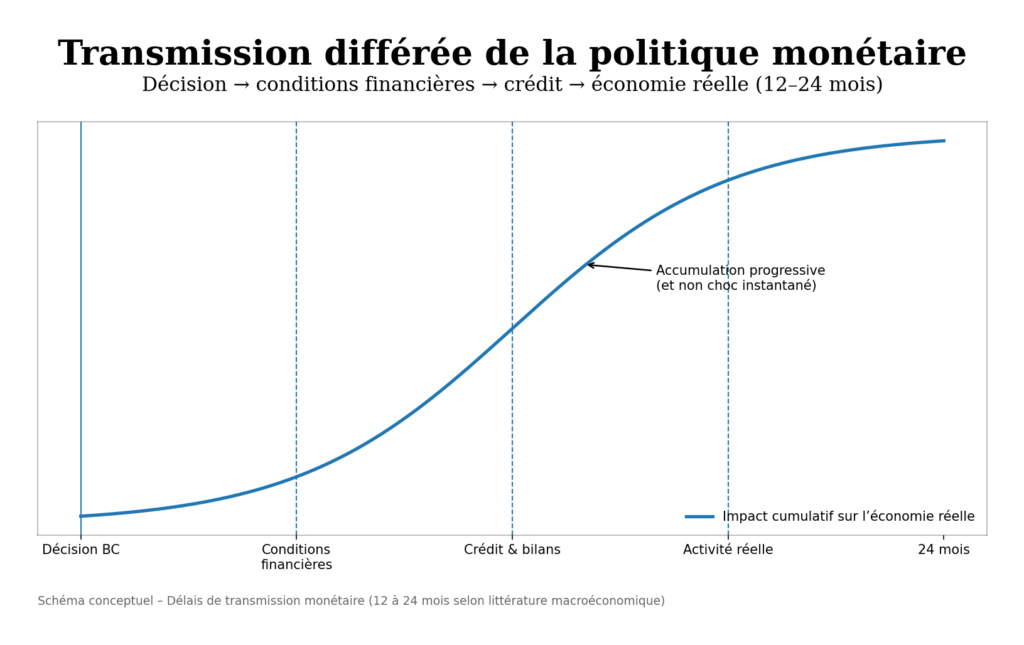

Monetary policy does not strike the economy — it soaks through it. Monetary transmission operates by accumulation across four principal channels (credit, balance sheets, expectations, exchange rate), with peak impact located between 12 and 24 months after the policy-rate inflection. This timing implies that the 2022–2023 tightening has not yet fully transmitted to the real economy in 2025–2026, contrary to some dominant readings. The accumulation transmission mechanism is well documented in the literature (BIS, ECB, Fed); precise calibration for the current cycle — marked by heterogeneous indebtedness structures and unprecedented geographic fragmentation — remains debated.

The central mechanism: four channels, one accumulation process

Monetary policy transmission to the real economy follows a causal chain in which each link operates with its own delay and intensity.

Trigger: the change in policy rates. The starting point is a central bank decision — hike, cut or hold. That decision changes the cost at which commercial banks refinance with the central bank. But that reference rate is not what firms or households pay: it is a signal that propagates through the financial system in successive steps. The 2022–2023 tightening provides the recent illustration: the ECB brought its policy rate from 0% to 4% in fourteen months, and the Fed raised its rates from 0–0.25% to 5.25–5.50% between March 2022 and July 2023 — the fastest tightenings since the 1980s.

Main transmission channel: credit and financing conditions. The policy rate first affects interbank rates, then lending rates to firms and households, with a lag that ranges from a few weeks (money markets) to several quarters (fixed-rate mortgages). The ECB Bank Lending Survey (Q4 2025) reports a significant, persistent tightening of lending standards for both firms and households. New corporate credit flows in the euro area fell by about 15% between their 2022 peak and end-2025 (ECB data, December 2025). The credit channel is the most direct and best-documented vector — a foundational Fed working paper (Bernanke & Gertler, 1995) formalized how credit conditions amplify monetary impulses beyond their direct effect on rates.

Amplifier: the balance-sheet channel and leverage effects. Rate hikes not only raise borrowing costs: they also depress the market value of financial and real assets recorded on agents’ balance sheets. That depreciation reduces collateral values, which limits borrowing capacity, which slows investment and consumption, which further depresses asset values — a feedback loop described by the BIS (Borio & Lowe, 2002) under the “financial accelerator” concept. The magnitude of this effect depends on initial leverage: the more leveraged the economy, the stronger the balance-sheet amplification. According to Banque de France data (Q3 2025), non-financial corporate debt in France reached 160% of GDP — among the highest levels in the euro area — mechanically increasing France’s sensitivity to the balance-sheet channel.

Macro consequence: slowdown by accumulation. The combination of these channels produces a slowdown that does not appear as a one-off shock but as a cumulative pressure. Quarter after quarter, the stock of credit renews under tighter conditions, balance sheets deteriorate marginally, corporate margins compress, investment projects are postponed. The economy does not flip — it erodes. This dynamic explains why cyclical indicators can remain positive for several quarters after a major tightening before a tipping point is reached. The IMF (World Economic Outlook, October 2025) estimates that the peak impact of the 2022–2023 tightening on advanced-economy growth will occur between H2 2025 and H1 2026 — roughly three years after the start of the tightening cycle.

What the consensus underestimates: transmission is not finished

The dominant market reading, echoed by many leading indicators, holds that most effects of the 2022–2023 tightening are already absorbed. This interpretation rests on real signals: stabilization of core inflation, labor market resilience in most advanced economies, and steady consumption indicators. The diagnosis is not without merit.

Its limitation lies in an implicit assumption of rapid and largely complete transmission. But this assumption collides with a well-documented mechanism: in economies where a substantial share of debt is rate-resettable or maturing for refixing, transmission continues mechanically even without new policy hikes. Decisions made in 2022–2023 keep increasing financial burdens as loans are rolled over at current conditions. An ECB working paper (Altavilla, Burlon, Giannetti & Holton, 2022) shows that the pass-through speed from policy rates to effective lending rates varies by a factor of two to three across euro-area countries — meaning transmission is complete in some economies (Spain, Portugal) and only halfway in others (France, Germany).

The consensus is therefore correct to note short-term activity resilience, but that resilience is precisely consistent with an incomplete transmission process: the heaviest effects tend to appear in the second and third year after tightening, not in the first. Concluding that transmission is over because the economy has not yet strongly slowed confuses delay with absence of effect.

Assessing monetary policy effectiveness over a few months. Monetary transmission peaks between 12 and 24 months — sometimes longer in economies where debt is largely fixed-rate. A tightening that “shows no visible effect” after six months has not failed: it has not yet had time to act. Bank Lending Survey results and credit flow data are more reliable early indicators than quarterly GDP to evaluate transmission status.

| Reading “transmission complete” | Accumulation reading | |

|---|---|---|

| Implicit assumption | Rapid, homogeneous pass-through | Gradual, fragmented pass-through |

| Observed signal | Employment and consumption resilience | Progressive credit contraction and balance-sheet erosion |

| Analysis horizon | 6–12 months post-tightening | 12–36 months, with cumulative effects |

| Main risk | Underestimating residual inflation | Underestimating forthcoming slowdown |

| Preferred indicators | GDP, employment, headline inflation | Credit flows, spreads, Bank Lending Survey, balance sheets |

Asymmetries, fragmentation and non-linearities: why transmission is never uniform

The schematic Trigger → Transmission → Amplifier → Consequence describes the general mechanics, but the reality of monetary transmission is crossed by complexities that profoundly alter its effective trajectory.

Fixed-rate vs variable-rate asymmetry. Debt structure determines transmission speed far more than the policy rate level. In economies where mortgages are predominantly variable-rate (Spain, UK, some Nordic countries), tightening transmits immediately to household payments within months. In economies dominated by fixed-rate debt (France, US, Germany), transmission works via new credit flows and rollovers — a process stretched over years. ECB data (Dec 2025) show the share of variable-rate mortgages in new flows ranges from 15% (France) to 85% (Finland) — a gap that makes any uniform impact reading for the euro area meaningless. A detailed analysis of monetary transmission delays and delayed effects clarifies these structural differences.

Geographic fragmentation of transmission. The euro area exemplifies fragmented transmission: a single monetary policy faces economies with highly divergent financial structures, indebtedness levels and housing markets. The spread in effective lending rates to firms ranged from 80 to 150 bps between core and periphery countries at end-2025 (ECB data) — a differential reflecting variable transmission intensity within a single monetary union. This fragmentation interacts with the desynchronization of economic cycles across regions, creating situations where the same policy is simultaneously too restrictive for some economies and too lenient for others.

Non-linearities and threshold effects. Monetary transmission is not proportional. Below a certain financial pressure level, households and firms absorb higher borrowing costs via margins or precautionary savings. Beyond a threshold — dependent on initial leverage, loan maturity profiles and income levels — behaviour flips non-linearly: firms cancel projects rather than shrink them; households delay house purchases rather than seek cheaper alternatives. The ECB credit survey (Q4 2025) indicates the share of firms delaying investment reached levels comparable to end-2019 — a threshold historically preceding marked contractions in gross fixed capital formation. Monetary policy thus acts as a cumulative pressure whose delayed effects crystallize abruptly when a financial tolerance threshold is breached. See restrictive monetary policy: mechanisms and delayed effects.

The role of expectations as accelerator or brake. Monetary expectations are ambiguous: if agents expect future easing, financial conditions loosen ahead of actual cuts (long rates fall, spreads compress), attenuating current transmission. Conversely, if “higher for longer” expectations anchor, the restrictive effect amplifies beyond what the policy rate alone implies. The role of monetary expectations in transmission explains why financial conditions can diverge significantly from the policy-rate signal — a phenomenon the current cycle vividly illustrates.

Measuring transmission: beyond the policy rate

If the policy rate is the trigger, it is a poor indicator of the tightening actually borne by the economy. Distinguishing nominal vs real rates provides one example: a 4% policy rate with 5% inflation is accommodative in real terms, while the same nominal rate with 2% inflation is clearly restrictive. Yet even the real rate captures only a fraction of reality.

The most relevant indicators to assess where transmission truly stands lie downstream of the policy rate: flows of new credit and volume of renegotiations (which measure how fast the debt stock re-prices at new conditions); the ratio of loan payments to household disposable income (which captures actual financial pressure); corporate funding spreads (which reflect credit risk pricing); early default indicators — payment delays, impaired loans — which signal when financial pressure starts converting into real losses.

The Federal Reserve Bank of St. Louis financial conditions series (National Financial Conditions Index) offers a long perspective: in the last six US tightening cycles, financial conditions continued tightening on average 8 to 14 months after the last rate hike — a lag confirming that the end of a hiking cycle is not the end of transmission, only the start of its most intense phase.

Implications for reading the current monetary cycle

If the cumulative transmission framework is relevant, it alters the reading of several ongoing dynamics.

For monetary policy interpretation. The 2022–2023 tightening, due to its speed and magnitude, is a historic monetary shock whose transmission remains structurally incomplete. The decisions made two to three years ago continue to diffuse through the economy as the stock of debt renews under new terms. The ECB, in its December 2025 bulletin, estimated that a gap persists between policy rates and effective financing conditions — a sign of incomplete transmission. The real-rate framework confirms that the degree of effective restriction depends more on financing conditions than on the headline policy rate alone.

For credit and balance-sheet analysis. Progressive credit volume contraction, slowing residential investment and mounting pressure on household budgets are early signals of an ongoing transmission. The balance-sheet channel in particular deserves close monitoring: falling real estate asset values in several European economies compress collateral and restrict SME financing, a mechanism that unfolds with a 12–18 month lag relative to property price declines. The monetary cycle interacts with the timing of the economic cycle, and the same policy produces radically different effects depending on the cycle phase in which it is applied.

For equities and valuation. Equity markets respond to shifts in financial conditions and rate expectations before monetary transmission affects the real economy — a phasing that creates sometimes durable divergences between market valuation and macro trajectory. This mechanism, analyzed in our banks, central banks and equity markets framework, implies markets can price easing while the restrictive effects of the prior tightening still diffuse in the real economy.

Invalidation condition. This cumulative transmission framework loses relevance if a rapid, massive easing (200 bps or more within 12 months) interrupts transmission before its peak, or if large targeted fiscal support neutralizes financial pressure on the most exposed agents. A positive productivity shock (AI-driven acceleration) could also offset monetary pressure by supporting corporate margins and incomes. Conversely, an exogenous energy price shock or a sovereign-debt confidence crisis would amplify and accelerate transmission.

Three time horizons to track transmission

Short horizon (0–6 months): the 2022–2023 tightening continues to diffuse via credit rollovers and balance-sheet erosion. Priority indicators: new credit flows, the ECB Bank Lending Survey, and corporate payment delays. Euro-area PMIs (~48–49 at end-2025) and contracting corporate credit signal active transmission. Short-term risk is a non-linear tipping if financial pressure crosses thresholds in the most indebted economies.

Cycle horizon (1–3 years): the tightening’s macro peak should materialize on this horizon per IMF and BIS estimates. The central question is the speed at which central banks will begin easing and whether that easing suffices to stop the cumulative dynamic. Transmission fragmentation within the euro area will create growing divergences between member economies. The interplay with the structural cycle dynamics will determine whether the slowdown remains orderly or becomes more pronounced.

Structural horizon (5+ years): the current cycle tests central banks’ ability to engineer disinflation without causing lasting damage to productive capacity. If tightening induces prolonged underinvestment — supported by potential growth data — its effects will exceed the cyclical episode and alter long-term trajectories. Monetary policy, by design a cyclical tool, could thus have structural consequences — raising the question of central banks’ limits. This logic feeds the broader reflection on monetary policy and its interaction with economic cycles.

Monetary transmission works by accumulation, not by shock. The 2022–2023 rate decisions continue to diffuse into the real economy through credit, balance sheets and expectations, independently of any pause or inversion in policy rates. Lack of a sharp slowdown does not mean monetary policy is ineffective — it means its structurally slow and uneven transmission process has not yet reached peak impact. Evaluating policy over too short an horizon systematically underestimates its effects.

Robust: The accumulation transmission mechanism (credit → balance sheets → real activity) is documented across decades of academic and institutional literature (Bernanke & Gertler, 1995; Borio & Lowe, 2002; BIS annual reports). The 12–24 month transmission lag is a convergent estimate from ECB, Fed and IMF work. Transmission fragmentation within the euro area is observable in effective lending rate data.

Uncertain: Exact calibration of peak impact in the current cycle is debated — estimates range from 18 to 36 months depending on models and national debt structures. The net effect of easing expectations (which loosen conditions before actual cuts) on transmission intensity is hard to quantify. The possibility of a non-linear shock (abrupt tipping after long resilience) is plausible but its timing is unpredictable.

Regular monitoring via the weekly macro bulletin allows confrontation of this framework with the latest credit, balance-sheet and financial condition data. Multiple trajectories remain possible, but reading monetary transmission through accumulation mechanisms — rather than immediate reaction to announcements — provides a more robust framework for handling cyclical surprises.

- Monetary policy does not strike the economy — it soaks through it. Transmission operates by accumulation across credit, balance sheets, expectations and exchange rate, with peak impact 12–24 months after the policy inflection.

- The 2022–2023 tightening has not yet produced its full effects: short-term resilience is compatible with an incomplete transmission process, not with its absence.

- Transmission fragmentation — between fixed and variable rates, and between core and peripheral countries — precludes a uniform impact reading for the euro area.

- Credit flows, balance-sheet metrics and financial-condition indicators are more informative than quarterly GDP to assess the true state of monetary transmission.

- This framework is invalidated if rapid monetary easing or massive fiscal support interrupts transmission before peak impact.

Mis à jour : 30 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.