Mortgage Credit Cycle: How Monetary Policy Transmits to Housing Prices

Between policy-rate hikes and housing price adjustments lies a frequently overlooked link: the credit cycle — the true echo chamber of monetary policy — whose own lags determine the timing and magnitude of the correction.

The housing market does not absorb rates — it absorbs the credit that results from them.

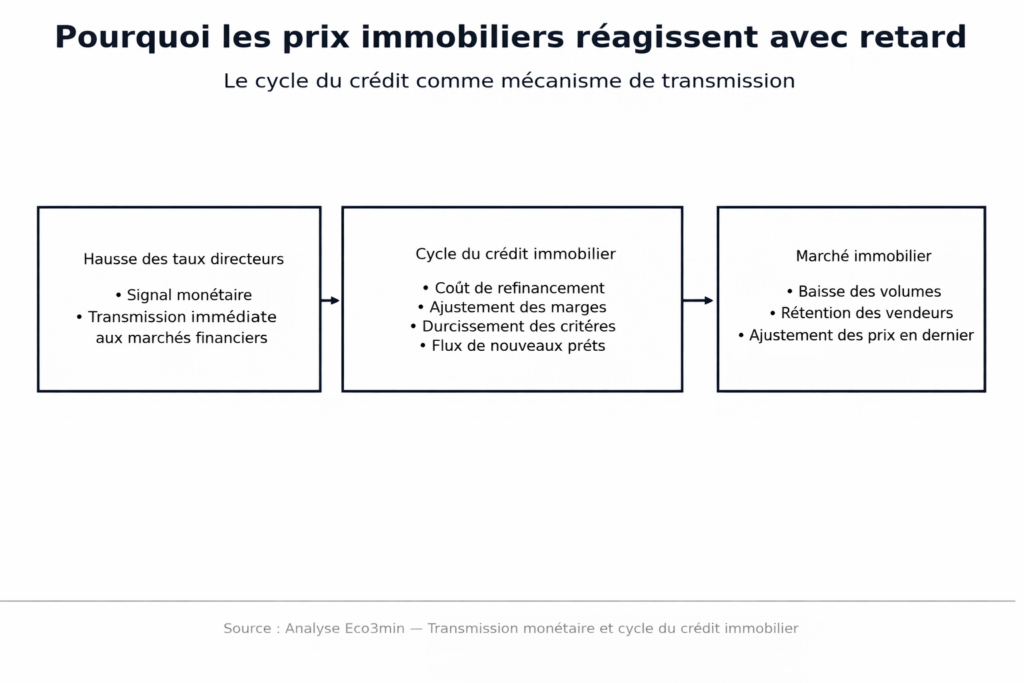

The mortgage credit cycle is the central transmission mechanism between monetary policy decisions and housing-price dynamics. Adjustment does not pass through policy rates themselves, but through effective financing conditions — credit volumes, lending standards, loan maturities — which follow their own timeline.

This distinction explains why housing prices remain resilient for quarters after major monetary tightening. The sequence is not rates → prices, but rates → credit → volumes → prices — each link operating with a structural lag unfamiliar to observers used to equity-market mechanics.

Since 2022, borrowing rates have doubled and transaction volumes have fallen by 20–30% — yet nominal prices have only eased modestly in most major metropolitan areas. This apparent paradox is not an anomaly: it is the signature of a housing market that does not directly absorb rate changes but the credit shifts they trigger. This dynamic fits within the broader framework of the mortgage credit cycle and connects with the analysis of monetary transmission to the real economy.

The housing market does not absorb rates — it absorbs the credit that results from them. Monetary policy transmission to housing prices follows a four-step sequence: policy-rate hikes → higher cost and contraction of credit flows → collapse in transaction volumes → delayed price adjustment. This structural lag explains why prices remain resilient for quarters after major tightening: volumes first, prices later is a structural market feature, not an anomaly. The mechanism is well documented (BIS, ECB, academic literature); the exact magnitude of further price adjustment in the current cycle — marked by constrained supply and fixed-rate credit structures — remains debated.

The central mechanism: how credit conditions housing prices

The transmission of monetary policy to the housing market follows a causal chain in which each link operates with its own lag — and it is the accumulation of these lags that produces the characteristic inertia of real-estate prices.

Trigger: policy-rate hikes and higher bank refinancing costs. The starting point is a monetary-policy decision that changes banks’ funding costs. This signal first transmits to interbank rates, then to borrowing conditions offered to households — but with filters: each institution’s funding structure, risk appetite and prudential constraints. The ECB raised its deposit rate from -0.5% to 4% between July 2022 and September 2023. Euro-area mortgage rates followed, rising from about 1.3% on average in early 2022 to over 3.8% by late 2023 (ECB Statistical Data Warehouse) — a tripling in eighteen months. But this increase in mortgage rates alone does not determine housing-price adjustment: what matters is its impact on the volume and conditions of credit actually granted.

Transmission channel: contraction in credit flows. The pivotal mechanism is the contraction in new mortgage lending. In the euro area, new housing-loan flows fell by roughly 35% between their 2022 peak and late 2023, then stabilized at historically low levels through 2024–2025 (ECB data, December 2025). This channel operates with a 3–6 month lag relative to mortgage-rate increases, as tighter lending standards gradually materialize in banks’ decisions. An ECB working paper (Kok, Mirza, Móré & Pancaro, 2016) formalizes this mechanism, showing that lending standards — not just rates — are the primary monetary-transmission channel to housing markets. The ECB Bank Lending Survey (Q4 2025) confirms continued tightening of mortgage credit standards, with stricter down-payment requirements and maximum debt-to-income ratios.

Amplifier: balance-sheet channel and structural volume–price asymmetry. Credit contraction triggers a characteristic asymmetric sequence in housing markets: transaction volumes collapse before prices adjust. This lag stems from a behavioral mechanism documented by the BIS (annual report 2024): sellers adjust price expectations downward with significant inertia — a phenomenon known as “downward nominal rigidity.” Data from French notaries and Eurostat for 2023–2025 illustrate this asymmetry: transaction volumes fell 20–35% depending on the market, while nominal prices declined only 3–8% in most major euro-area cities. Amplification comes from the balance-sheet channel: even modest price declines reduce collateral values, which limits borrowing capacity for potential buyers, further compressing transactions and exerting additional pressure on prices — a feedback loop that self-sustains as long as credit conditions remain restrictive.

Macro consequence: slow, cumulative and structurally incomplete adjustment. The combination of these channels produces a housing adjustment fundamentally different from equity corrections: it is slow (spread over 2–5 years), asymmetric (volumes absorb the initial shock), and often incomplete in nominal terms (real prices — inflation-adjusted — may fall significantly without large nominal declines, an “invisible” correction documented by the IMF in financial stability reports). This pattern implies that most price adjustment may occur not through abrupt nominal drops but through gradual real erosion over several years.

- Euro-area mortgage rates: ×3 in 18 months (~1.3% early 2022 → ~3.8% late 2023). Source: ECB Statistical Data Warehouse.

- New housing-loan flows: –35% between the 2022 peak and late 2023. Source: ECB, December 2025.

- Transaction volumes: –20% to –35% across markets since 2022. Sources: French notaries, Eurostat.

- Nominal prices: –3% to –8% in major euro-area metro areas. Source: Eurostat quarterly indices.

- Real prices (inflation-adjusted): –10% to –15% cumulatively since 2022. Sources: Eurostat, Eco3min calculations.

What the consensus gets right — and the correction it underestimates

The dominant housing-market narrative, supported by most sector analysts and real-estate surveys, rests on an apparently reasonable diagnosis: the worst of the adjustment is behind us. Mortgage rates have stabilized, new-loan flows show tentative recovery, and nominal prices are holding — interpreted as a price floor. This reading has merit: stabilizing mortgage rates are indeed a necessary condition for market normalization.

Its limitation lies in confusing flow stabilization with cycle normalization. Mortgage credit has stopped contracting — but remains historically weak. Lending standards remain restrictive. And the volume → price correction mechanism is structurally lagged: prices adjust last, not first. The IMF (Global Financial Stability Report, October 2025) notes that housing-price corrections historically follow credit contraction with a 4–8 quarter lag in advanced economies — placing the potential price-correction peak between late 2025 and 2027 in the current cycle. This mechanism explains why housing-price declines, when they materialize, always surprise by their slowness — and why “housing crisis” diagnoses consistently arrive after the fact.

The consensus is therefore right to note credit stabilization but confuses stabilization with normalization. Credit stabilized at a restrictive level is not accommodative — it sustains pressure on volumes and, by extension, on prices even without further deterioration. The gap between the normalization narrative and the reality of a still-constrained credit cycle is where underappreciated correction risk lies.

Equating stabilized mortgage rates with housing-market normalization. Nominal price resilience amid collapsed volumes does not signal a floor — it signals an illiquid market where prices are set by marginal transactions. Real adjustment occurs through volumes first (collapsed), real prices next (declining once inflation-adjusted), and nominal prices last. Data from French notaries, Eurostat and inflation-adjusted price indices are the most relevant indicators to assess the true state of correction.

| “Floor reached” reading | Credit-cycle reading | |

|---|---|---|

| Core assumption | Rate stabilization marks the end of adjustment | Price adjustment follows credit contraction with a 4–8 quarter lag |

| Invoked signal | Nominal price resilience, mortgage-rate stabilization | Collapsed volumes, restrictive lending standards, credit stabilized at low levels |

| Analysis horizon | 6–12 months (current data) | 12–36 months (full volume → price cycle) |

| Main risk | Missing the rebound if credit restarts | Underestimating further real correction |

| Key variable | Mortgage rates, nominal prices | Credit flows, lending standards, real (inflation-adjusted) prices |

Bank balance sheets, regulation and structural rigidities: why housing never adjusts like financial markets

The general transmission framework hides complexities that explain why housing markets follow dynamics profoundly different from financial markets.

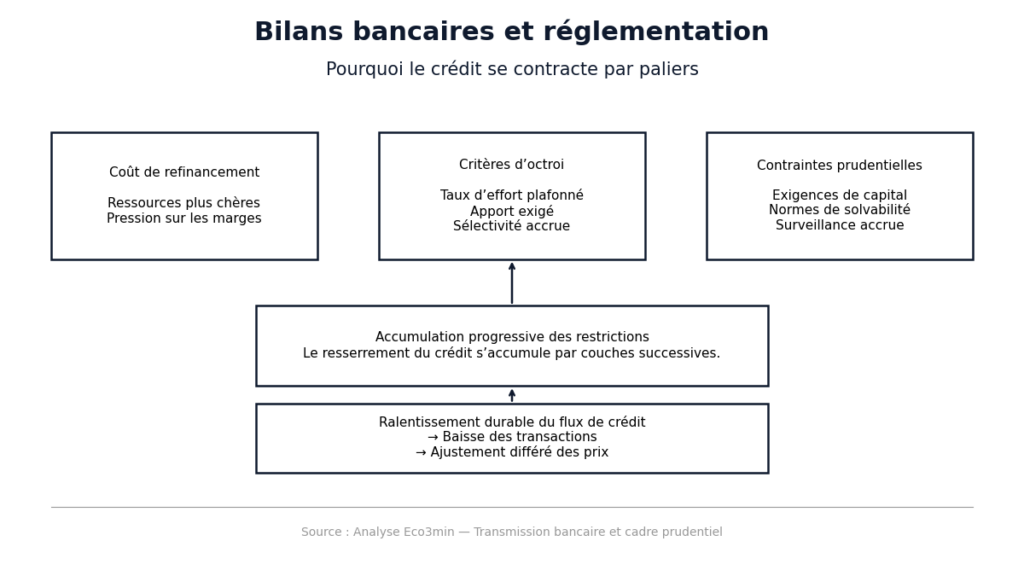

Bank balance sheets as echo chambers. Bank balance-sheet health is an overlooked but decisive transmission link. When rates rise rapidly, banks face higher funding costs and tighter trade-offs — interest-rate risk on bond portfolios, default risk on loan books. This adjustment mechanism accumulates stepwise. Intermediation margins reshape, lending standards tighten gradually, and certain borrower categories — first-time buyers, low down-payment applicants — are excluded first. ECB data (December 2025) show tightening was more pronounced for mortgage lending than for corporate credit — consistent with real estate’s heavy weight on European bank balance sheets (about 40% of total outstanding loans, Banque de France data).

Regulation as amplifier or shock absorber. Beyond rates and bank health, the regulatory framework acts as a credit-cycle multiplier. France’s High Council for Financial Stability capped borrowers’ debt-service ratios at 35% and loan maturities at 25 years — constraints that, layered onto high-rate conditions, lock the credit cycle far longer than a simple rate shock. Interaction between prudential constraints (Basel III capital requirements) and monetary tightening creates a scissors effect: banks are simultaneously pushed to tighten by monetary policy and constrained by prudential ratios that limit easing capacity — even if rate signals reverse. This regulatory lock-in mechanism is specific to housing and has no equivalent in financial markets.

Nominal rigidity and the illusion of stability. Downward nominal rigidity in housing prices — documented by an NBER working paper (Genesove & Mayer, 2001) and confirmed in the current cycle — creates an illusion of stability. Sellers prefer to withdraw listings rather than accept discounts, shrinking supply and artificially sustaining nominal prices. The result is a market where posted prices hold but liquidity collapses — published prices reflect only marginal transactions. Real adjustment then occurs through two channels invisible in nominal indices: real-price correction via inflation erosion (around 2–4 percentage points per year in 2023–2025) and quality deterioration (units selling at posted prices skew higher-end, biasing indices upward).

Geographic desynchronization. The desynchronization of cycles across major economies is amplified in housing. Debt structures determine transmission speed more than rate levels: markets dominated by variable-rate lending (Spain, UK, Nordic countries) absorbed the rate shock faster, with larger nominal price corrections (7–15% depending on market, Eurostat data). Markets dominated by fixed-rate lending (France, Germany) are still digesting the shock, with adjustment mainly concentrated in volumes. The same monetary policy thus produces housing cycles staggered by 12–24 months across euro-area countries.

Measuring the mortgage credit cycle: beyond mortgage rates

Mortgage rates are the most cited indicator but a poor signal of the cycle’s real state. More relevant indicators lie downstream: monthly new housing-loan flows measure effective financing dynamics; bank approval rates (share of accepted applications) capture tightening or easing beyond rates alone; average loan maturity signals structural inertia (longer maturities partially offset higher rates, capped maturities signal exhausted adjustment margins); the spread between mortgage rates and risk-free rates measures the real cost of housing finance beyond policy signals.

Long-run Banque de France data on housing-loan flows provide historical perspective: across the last four French housing cycles (1991, 2001, 2008, 2022), credit-flow contraction preceded price corrections by an average of 4–8 quarters. Credit signals housing-cycle turning points well before prices confirm them — a pattern reinforced by the distinction between nominal and real rates: stable borrowing rates combined with falling inflation mean rising real rates, increasing financing restrictiveness even without new hikes.

Implications for reading the current housing market

If the credit-cycle framework is relevant, it changes the reading of several ongoing dynamics.

For market diagnosis. Nominal price resilience amid collapsed volumes does not signal market strength — it signals an illiquid market undergoing incomplete adjustment. The analytical framework of the real cost of money confirms that the effective financial constraint on potential buyers remains high: with mortgage rates around 3.5–4% and falling inflation, the real cost of housing finance is at its highest since 2008. The real cost of homeownership — measured by mortgage payments relative to disposable income — has risen about 30% since 2021, reflecting both rate increases and nominal price resilience. If credit conditions do not ease significantly — in volumes and lending standards, not just rates — downward price pressure will persist, with adjustment continuing mainly through real erosion and progressive deterioration in less liquid segments (commercial real estate, peri-urban areas, energy-inefficient housing).

For monetary policy reading. Potential monetary easing (policy-rate cuts) does not transmit symmetrically to the mortgage credit cycle. Downside transmission is structurally slower than upside transmission because banks maintain restrictive standards while default risk remains high and regulatory frameworks constrain flexibility. This asymmetric lag — formalized in ECB pass-through research — implies that a 100-basis-point rate cut would revive the mortgage credit cycle only after a 6–12 month delay, and only if accompanied by easing lending standards. The monetary channel interacts with the economic cycle timing to determine the speed of market normalization.

For structural dynamics. The current cycle overlaps with structural trends reshaping housing markets: energy transition (devaluing inefficient homes and creating a “green premium”), demographics (aging populations, evolving household structures), and post-pandemic geographic reconfiguration (remote work, migration to mid-sized cities). These forces create cycle-specific singularities that prevent mechanical extrapolation of past corrections. The analysis fits within the broader perspective of housing cycles, rates and the economy.

Invalidation condition. This framework loses relevance if rapid and massive monetary easing, combined with regulatory relaxation (higher debt-service caps, longer allowed maturities), sharply revives credit flows and interrupts the correction sequence. An exogenous demand shock — large-scale homeownership support programs, migration surges concentrated in specific areas — could also alter trajectories. Conversely, a deeper-than-expected recession, rising defaults on existing loans or contagion from commercial real-estate stress would amplify and accelerate residential price adjustment, turning an orderly correction into an outright housing crisis.

Three time horizons to monitor the housing cycle

Short horizon (0–6 months): mortgage credit flows show signs of stabilization at low levels. Transaction volumes remain depressed. Nominal prices appear resilient, but real (inflation-adjusted) prices continue to erode. Priority indicators: Bank Lending Survey (mortgage standards), monthly housing-loan flows (Banque de France, ECB), and inflation-adjusted price indices (INSEE, Eurostat). The short-term risk is accelerated correction in the most fragile segments if labor markets weaken.

Cycle horizon (1–3 years): the decisive question is the speed of credit-flow normalization. If lending standards ease significantly — requiring both policy-rate cuts and looser bank criteria — the cycle could turn upward within 18–24 months. Otherwise, real-erosion correction will persist, with growing divergence across markets (tight markets more resilient than slack ones, energy-efficient housing outperforming inefficient stock). The structural dynamics of the economic cycle will determine whether adjustment remains contained or becomes more pronounced.

Structural horizon (5+ years): the current cycle tests housing markets’ ability to adapt to structurally higher interest-rate regimes than during 2010–2020. If the real cost of housing capital remains durably above 2%, valuation multiples (price-to-income, price-to-rent ratios) must converge toward lower historical norms — an adjustment that may take 5–10 years and occur mainly through real erosion rather than abrupt nominal declines. This outlook raises questions about potential growth and households’ investment capacity in a normalized cost-of-capital environment.

The housing market does not absorb rates — it absorbs the credit that results from them, with structural lags of several quarters at each transmission step. The sequence rates → credit → volumes → prices is a constant of housing cycles, and the current cycle is no exception. Nominal price resilience masks substantial adjustment already visible in real terms and volumes. The consensus confuses stabilization with normalization: credit stabilized at restrictive levels sustains pressure even without further deterioration. The most likely correction is not nominal collapse but progressive real erosion — the type of adjustment nominal price indices detect last.

Robust: The transmission sequence rates → credit → volumes → prices is documented across decades of data and academic literature (BIS, ECB, IMF GFSR). The 4–8 quarter lag between credit contraction and price correction is a convergent estimate. Volume–price asymmetry (volumes adjust before prices) is a consistent feature of housing cycles. Downward nominal rigidity is well documented (Genesove & Mayer, 2001).

Uncertain: The exact magnitude of further price correction remains debated — it depends on credit trajectories, regulatory evolution and local supply-demand balances. The impact of the energy transition on price differentiation (green premium) is materializing but hard to quantify. The speed of transmission of potential monetary easing to the mortgage credit cycle is uncertain — asymmetric lag (slower downside transmission) is documented but its calibration in the current cycle remains open.

Regular monitoring of the weekly macro checkpoint allows this framework to be tested against the latest credit, volume and price data. Several trajectories remain open, but reading the housing market through its credit cycle — rather than policy rates alone — provides a more robust framework to anticipate the timing and nature of adjustment ahead.

- The housing market does not absorb rates — it absorbs the credit that results from them. The transmission sequence rates → credit → volumes → prices is the structural constant of housing cycles.

- Transaction volumes absorb most of the initial shock (–20% to –35% in the euro area since 2022), while nominal prices adjust last — a 4–8 quarter lag that creates an illusion of resilience.

- The real correction is already substantial: inflation-adjusted housing prices in the euro area have declined significantly, even where nominal prices appear stable.

- The credit cycle is amplified by three structural factors — bank balance sheets, the regulatory framework (HCSF, Basel III) and downward nominal rigidity — that extend adjustment duration.

- This framework is invalidated if massive monetary easing combined with regulatory relaxation sharply revives credit flows, or if an exogenous demand shock alters the supply-financing balance.

Mis à jour : 30 March 2026

This article provides economic and financial analysis for informational purposes only. It does not constitute investment advice or a personalized recommendation. Any investment decision remains the sole responsibility of the reader.