The 1997 Asian Financial Crisis: a Dollar Shortage Outside the US Core

In 1997, the collapse of emerging-Asia currencies was a shortage of dollars outside the United States, leaving US financial conditions untouched.

Short-term debt denominated in dollars, backed by currencies pegged to the dollar, turns a capital outflow into a currency shortage. When the peg breaks, the remaining debt doubles in weight and the flight feeds on itself.

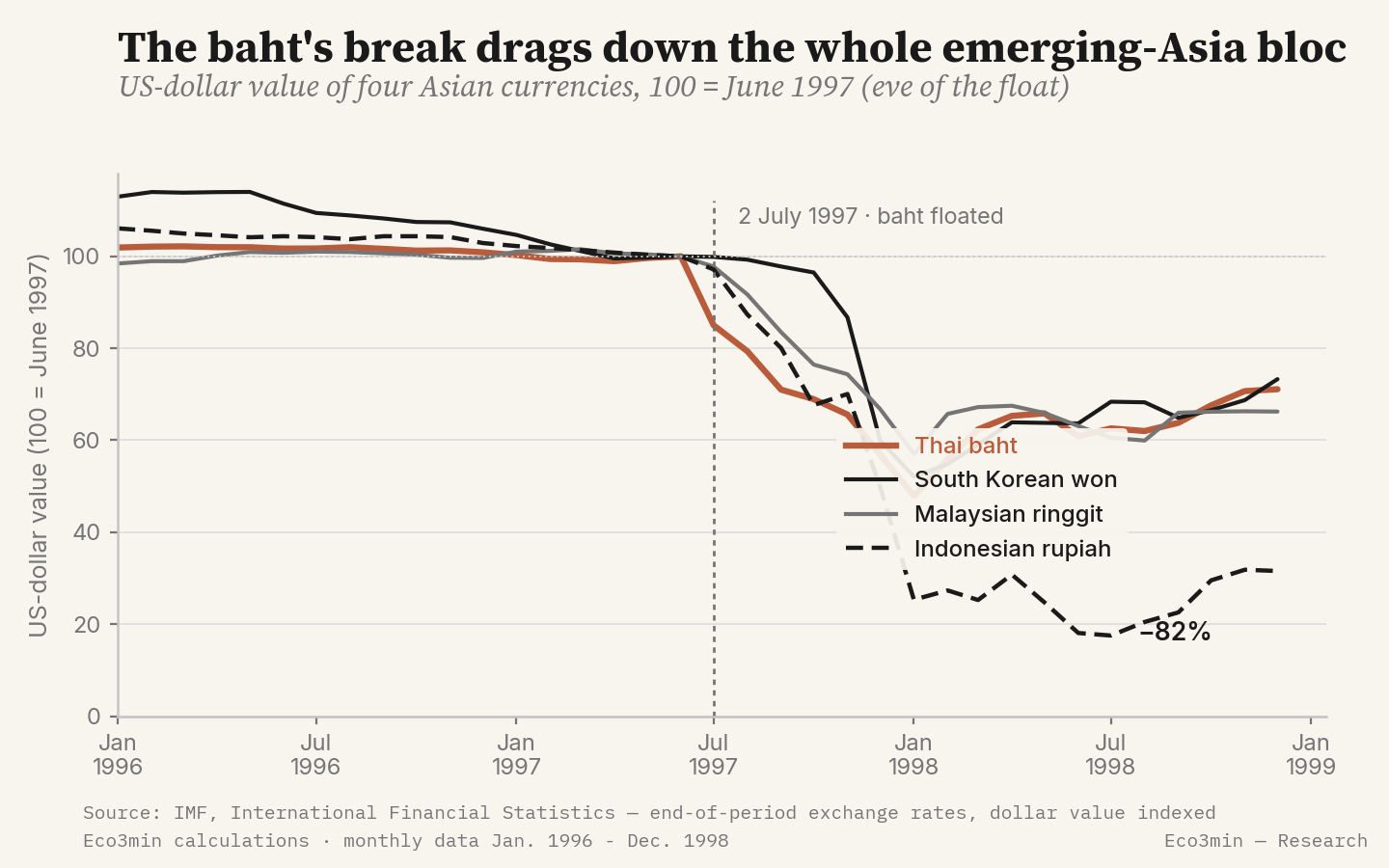

In July 1997, the abandonment of the baht’s dollar peg triggered a capital flight across emerging Asia: currencies collapsed, with the Indonesian rupiah losing more than 80% of its dollar value. The destination is a shortage of dollars (layer 2), concentrated outside the United States, which remained the safe haven, with no strain on its financial conditions.

The starting point: “miracles” funded in dollars

In the mid-1990s, Thailand, South Korea, Indonesia and Malaysia posted some of the highest growth rates in the world. Their funding rested on a common mechanism: currencies tightly pegged to the dollar, which brought the perceived exchange-rate risk down to almost nothing and attracted portfolio capital and short-term bank loans denominated in foreign currency.

That peg carried a hidden cost. Part of the external debt was short-term and dollar-denominated, while the assets it financed — real estate, industrial capacity — were domestic and in local currency. As long as the parity held, the mismatch stayed invisible. According to the long series of the Bank for International Settlements (BIS), cross-border bank claims on these economies rose sharply through 1996, the bulk of it at maturities under one year.

The global monetary backdrop tightened the constraint. After its 1995 low, the dollar appreciated steadily. A rising dollar makes a peg more expensive to defend and increases the weight of every foreign-currency payment for borrowers whose revenues remain in local currency. The vulnerability came not from excess inflation or a US rate cycle, but from a balance-sheet mismatch exposed to dollar availability.

Timeline of the regime shift

The episode unfolded over little more than a year, from the first float to the regional low.

- 2 July 1997 — after weeks of costly defence in reserves, the Bank of Thailand let the baht float. The dollar peg, effectively in place for more than a decade, was abandoned.

- August 1997 — the IMF arranged a programme of roughly USD 17 billion for Thailand. The pressure spread to Manila, Kuala Lumpur and Jakarta.

- 23-27 October 1997 — the Hong Kong dollar peg was defended through a spike in interbank rates; the shock briefly reached global stock markets, including Wall Street, before being absorbed.

- 3 December 1997 — the IMF granted South Korea the largest programme in its history at that date, roughly USD 58 billion; the won had collapsed in November-December.

- January 1998 — the Indonesian rupiah went into free fall despite an IMF programme signed in late 1997.

- Mid-1998 — the episode found its regional low. The contagion would then reach Russia in August, the starting point of a second shock of the same nature.

The indicators before the crisis

Read through the Eco3min grid, which measures the US and global regime, the 1997 episode sends no cyclical regime-shift signal for the United States. The only member of the “dollar shortage” signal set that tightens at the global scale is the value of the dollar itself.

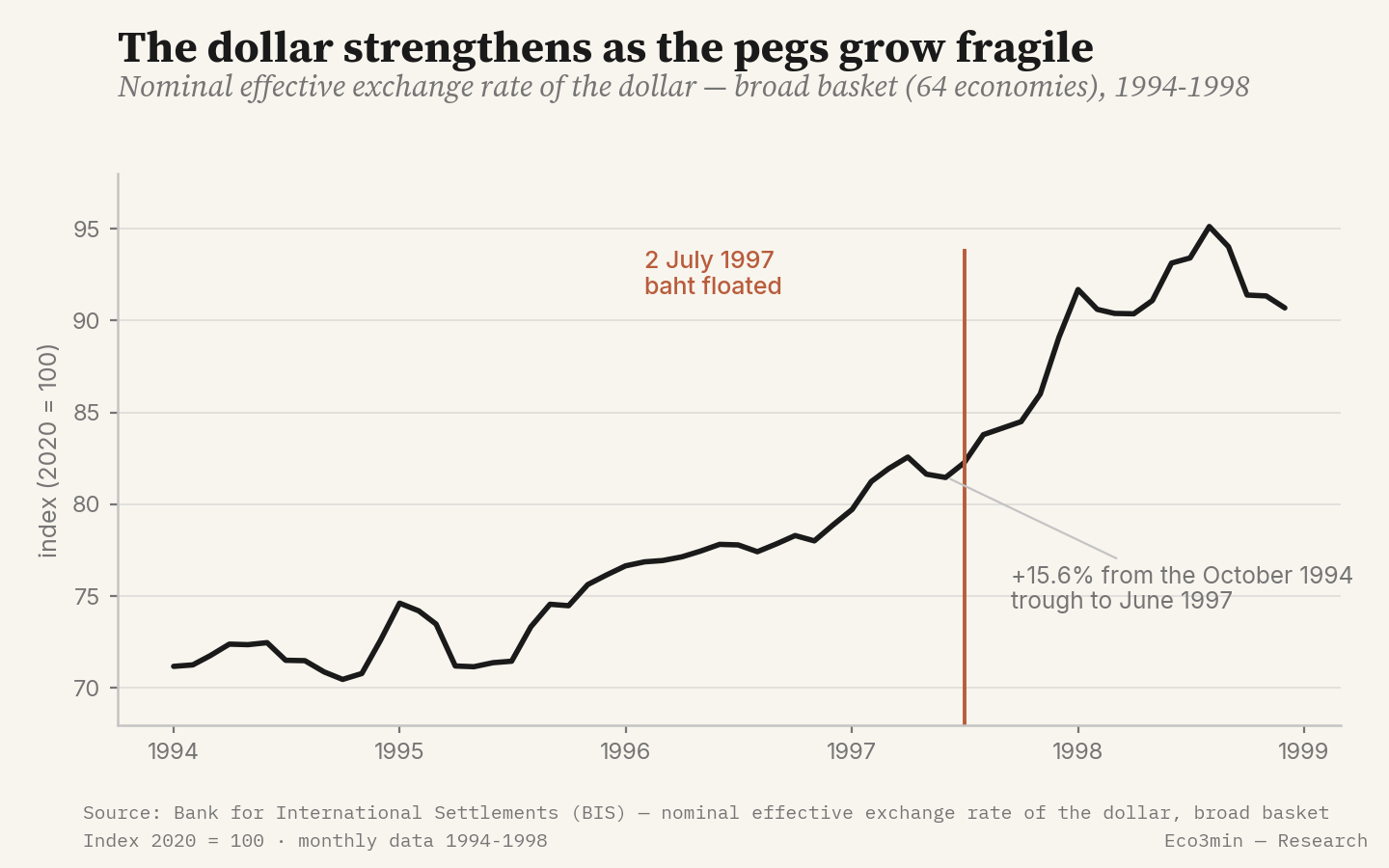

Measured by the BIS nominal effective exchange rate, the dollar strengthened by 15.6% between its October 1994 trough and June 1997, then continued to rise through the crisis. This is the closest analogue to the first signal in Eco3min’s Dollar Shortage overlay (the appreciation of the broad dollar), reconstructed here from a series that predates the one the engine uses (see the next section).

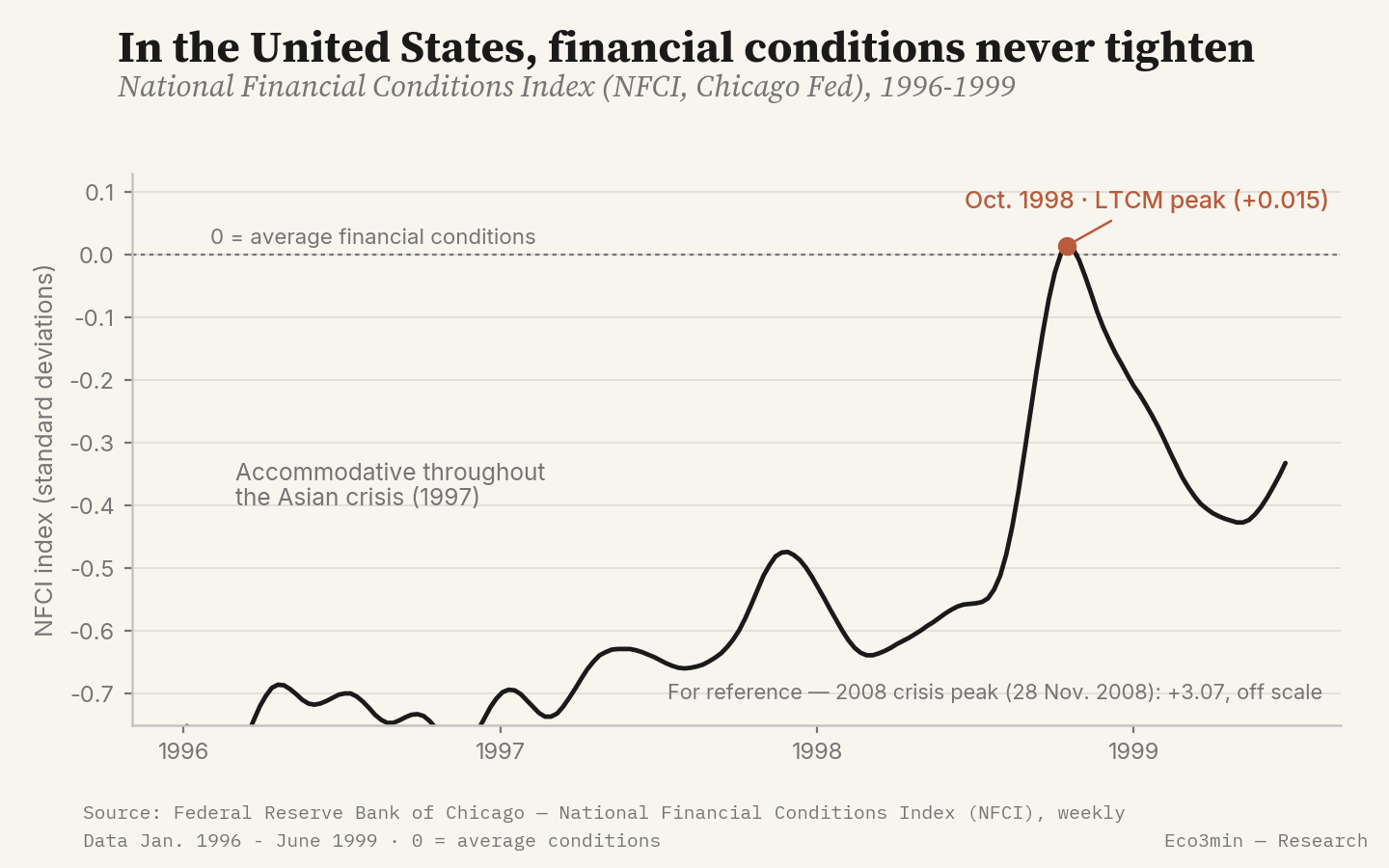

The other documented member of the set, the US National Financial Conditions Index (NFCI, Chicago Fed), gives no warning on the US side: it stays in accommodative territory throughout the Asian phase. The dollar shortage lodged in emerging-market balance sheets, where short-term debt met the collapse of exchange rates, a place that US-centred indicators do not capture.

The regime shift: through which channels

The dominant reading remembers 1997 as a contagion of speculative attacks, sometimes attributed to institutional weaknesses specific to each country. That reading describes the trigger well, the common thread less so.

That common thread is dollar availability. Once the baht was floating, creditors reassessed every economy with a similar profile: short-term dollar debt, a pegged currency, limited reserves. The withdrawal of funding forced sales of the local currency, which drove the exchange rate down, which in turn increased the weight of the remaining dollar debt and accelerated the next withdrawal. The cascade did not follow a border, it followed a balance-sheet structure.

The scale is measurable. Between their pre-float level (June 1997) and their low, the four currencies lost a major share of their dollar value, according to the IMF’s end-of-period rates (International Financial Statistics). South Korea, the most developed economy in the group, saw the won move from roughly 890 to more than 1,700 per dollar within a few weeks in late 1997.

One qualification is needed, however. Eco3min’s US/global grid captures this dollar shortage only indirectly: the broad-dollar signal used here is a pre-2006 substitute, the high-yield credit spread of the period is not retained in the Eco3min database, and the NFCI, a US conditions indicator, never tightened. The signal set is therefore partial. The page reports a destination framework (a layer-2 Dollar Shortage overlay), not a monthly verdict computed by the engine. The vulnerability was real and regional: it lay in the debt structure and peg choice of the affected economies, which the US lens does not see directly.

Central banks and the IMF: no dollar backstop

The 1997 response does not resemble that of 2008 or 2020. No Federal Reserve dollar swap line was opened toward Asia: foreign central banks’ access to dollars, the central mechanism of later crises, did not yet exist as a systematic facility. The currency shortage therefore drained through two more rudimentary channels.

The first is the depletion of reserves. Asian central banks ran down their foreign-exchange reserves defending untenable parities, until they had to float. The second is conditional IMF funding: according to the Fund, the programmes for Thailand (August 1997), Indonesia (November 1997) and Korea (December 1997) totalled more than USD 110 billion in commitments.

In return, these programmes imposed high interest rates and fiscal discipline, a conditionality whose procyclical effect on economies already in recession remains one of the most debated aspects of the episode. The Federal Reserve, for its part, reacted only from September 1998, with 75 basis points of cuts across three moves; but those cuts responded to the failure of a highly leveraged US fund, the next shock, not to Asia in 1997.

Assets and markets: the US safe haven

The rotation of assets confirms the geography of the shock. The capital leaving emerging Asia did not disappear: it retreated to quality, namely to US government bonds and the dollar. Emerging-market equities and currencies collapsed; the US bond market, for its part, benefited from the inflow, and US equities went through 1997 in positive territory.

The contrast is clear in the figures. The NFCI stayed negative, hence accommodative, throughout 1997 (−0.65 in July, −0.48 in December, according to the Chicago Fed). It only edged toward neutral in October 1998, at +0.015, at the height of the Russian episode and the failure of the LTCM fund. Across the whole of 1997 as well as late 1998, the index never crossed in any week the +0.30 threshold that triggers, on the US side, the Dollar Shortage signal. For reference, that same index would peak at +3.07 on 28 November 2008.

The exchange-rate moves and index levels described here characterise a past episode, drawn from IMF, BIS and Chicago Fed data. They constitute neither a forecast nor a recommendation to buy, sell or hedge, and past performance does not prejudge future performance.

What was different: 1997 versus 1998

The Russian crisis and the LTCM failure, in 1998, belong to the same destination regime, a shortage of dollars (layer 2). Both episodes share a drying-up of dollar funding, a flight to quality and a forced-deleveraging dynamic. Three differences nonetheless explain why the analogy quickly reaches its limit.

- The locus. In 1997, the shock originated in emerging real economies, through their short-term external debt. In 1998, it concentrated on a highly leveraged US financial actor whose positions directly threatened banking counterparties at the core of the system.

- The transmission to the United States. In 1997, the United States was a safe haven: capital flowed in, government bonds richened, financial conditions stayed accommodative. In 1998, the dollar shortage reached the US core through leverage and position correlation, and tightened domestic conditions for the first time in the sequence.

- The response. In 1997, the mechanism was external and conditional: IMF programmes for sovereign states. In 1998, it was internal and fast: a recapitalisation of LTCM organised by the Federal Reserve Bank of New York among private creditors, accompanied by rate cuts.

What invalidated the analogy was precisely the point of entry of the missing dollar into the financial system: external and absorbable in 1997, internal and systemic in 1998.

The 1997 Asian crisis was a dollar shortage with no US stress: the rupiah lost 82% of its value while the NFCI stayed accommodative.

Where this crisis leads

In Eco3min’s mapping of regimes, 1997 belongs to a layer-2 overlay: the dollar shortage regime. This page describes the sequence of the shift; the Atlas page describes the destination state.

A drying-up of access to dollar funding outside the US system, independent of the state of the US growth-and-inflation cycle. The classification is reconstructed, not measured live: the engine’s signal set is only partially available for 1997, and its sole US-centred member never activated.

Atlas — the dollar shortage regimeSources

- IMF, International Financial Statistics — monthly exchange rates (Thailand, South Korea, Indonesia, Malaysia).

- IMF — 1997 assistance programmes (Thailand, Indonesia, South Korea).

- Bank for International Settlements — nominal effective exchange rate of the dollar (broad basket).

- Federal Reserve Bank of Chicago — National Financial Conditions Index (NFCI).

- Eco3min data: broad dollar index, NFCI.

Last updated — 31 May 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.