The 2022 UK gilt crisis: an inflationary regime, a regional fracture

How, in 2022, the United States settled into an inflationary regime while global tightening fractured a hidden leverage structure in the UK bond market: a reading of the crisis through the Eco3min indicators.

In 2021-2022, the U.S. economy entered a measurable inflationary regime, and the Federal Reserve launched the fastest tightening since the early 1980s. This repricing of duration spread to global bond markets. In the United Kingdom, it put under strain a pension-fund liability-hedging structure — LDI — that an unfunded mini-budget tipped into a forced-selling spiral. The Bank of England bought long gilts to break the loop, even as it was tightening elsewhere.

In 2022, the Eco3min engine places the United States in an inflationary regime (neutral growth, high underlying inflation: G= I+). The fastest global tightening since the early 1980s fractured a hidden leverage structure in the gilt market: the Bank of England stepped in to break the spiral.

Timeline of the shift

The UK fracture played out over some twenty days, but it sits within a tightening that had begun six months earlier.

- 16 March 2022 — the Federal Reserve raises rates for the first time since 2018, opening the fastest tightening since the early 1980s.

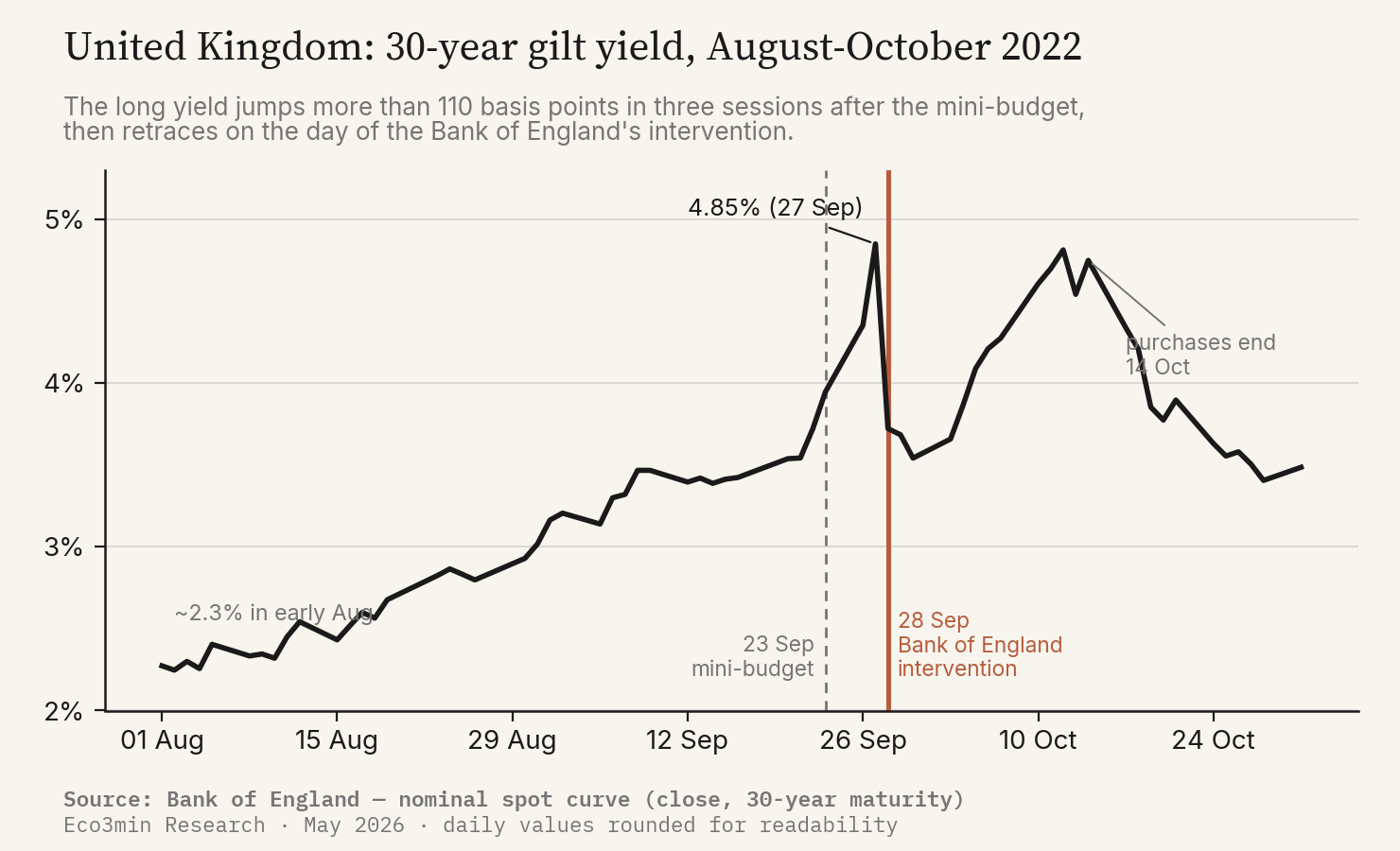

- 23 September 2022 — the UK “mini-budget” announces unfunded tax cuts on the order of £45 billion.

- 26 September 2022 — sterling falls to $1.07 at the close, its lowest closing level on record, after an intraday low also without precedent.

- 27 September 2022 — the 30-year gilt yield peaks at 4.85% at the close (spot curve, Bank of England).

- 28 September 2022 — the Bank of England announces temporary purchases of long gilts, up to £65 billion, on financial-stability grounds.

- 14 October 2022 — the purchase programme ends; on 17 October the new chancellor reverses most of the mini-budget.

The indicators before the crisis

By the spring of 2022, the Eco3min engine’s inputs traced an unambiguous regime: entrenched underlying inflation, growth close to trend, financial conditions still far from stress. The leverage that would break in September was already under strain: the UK long yield had more than doubled before any budgetary shock.

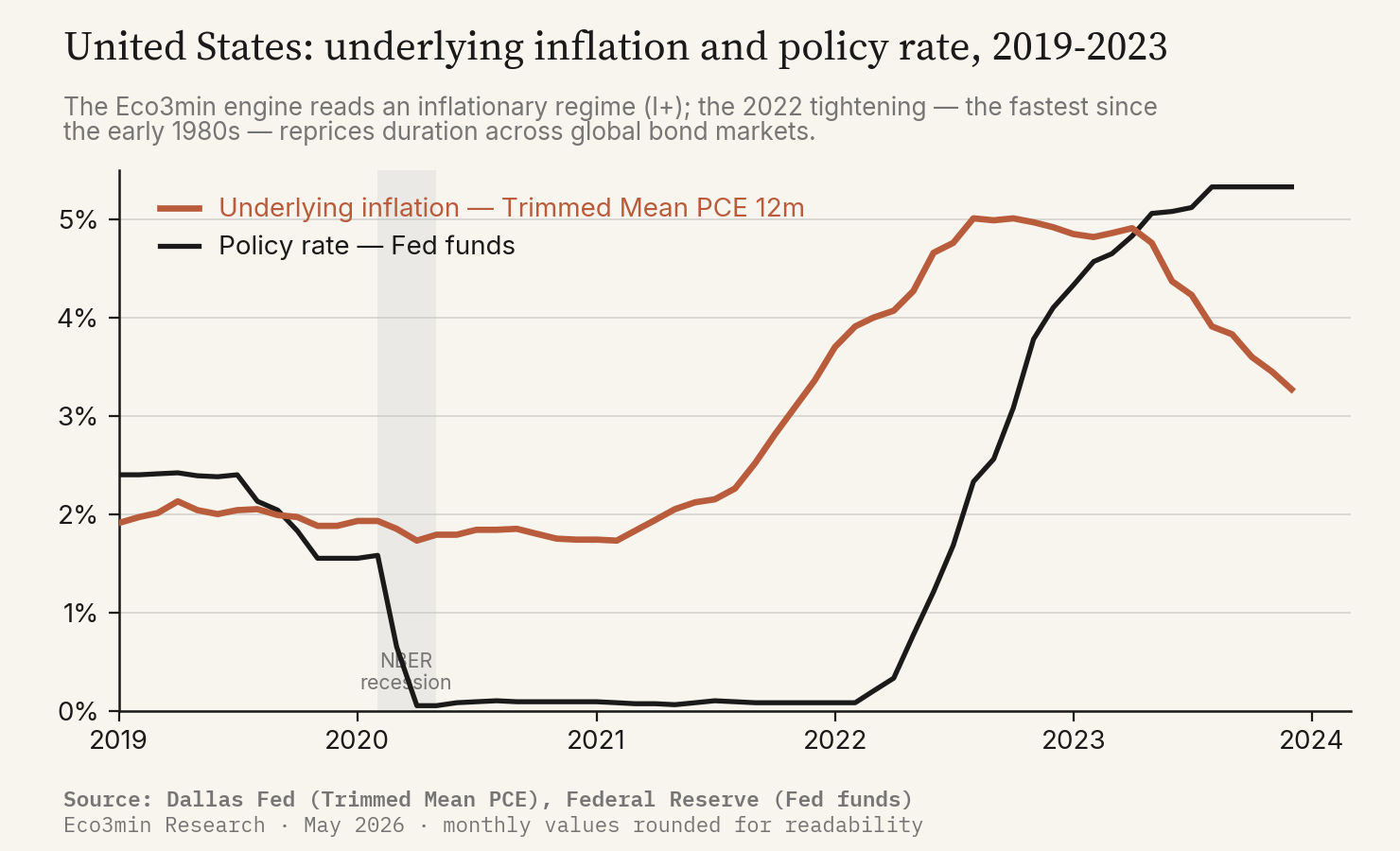

The Trimmed Mean PCE (12-month, Dallas Fed) is above 2.75% and still rising in the first half of 2022: the engine’s inflation axis is at I+.

Trimmed Mean PCEThe CFNAI-MA3 (Chicago Fed) hovers around −0.22: growth slightly below trend, never in contraction territory. The growth axis stays neutral (G=).

CFNAI-MA3The federal funds rate lifts off from near 0% in March 2022 and gains about 4 points over the year: the fastest pace of tightening since the early 1980s.

Federal funds rateThe 30-year gilt yield moves from around 1.2% in early January 2022 to 3.7% on the eve of the mini-budget (Bank of England). Long duration is already heavily repriced.

30-year gilt (to confirm)The dominant signal is not a stress gauge lighting up, but a cost of capital rising everywhere at once. The engine reads high underlying inflation in the United States; the monetary-policy response that follows lifts the yield demanded on long duration, and this repricing does not stop at the U.S. border. The UK gilt absorbs it before the crisis — a weak signal that markets read at the time as mere normalisation, rather than as a leverage structure being placed under constraint.

One reading nuance is worth setting out. The engine’s inflation axis tracks underlying inflation, the Trimmed Mean PCE, not the more volatile headline measure. In 2022 the two point the same way, but it is the persistence of the underlying component, not the energy shock alone, that fixes the state at I+. The tightening that follows is therefore not a response to a transitory spike: it targets entrenched inflation, which explains its scale and duration, and, by extension, the continuing pressure on long duration through the year.

The regime shift

The word “shift” calls for a clarification here. The U.S. regime does not change during the gilt crisis: it is already inflationary before September 2022. The transition measured by the engine is earlier — it is the entry into the inflationary regime of 2021-2022. What the UK fracture reveals is the channel through which that regime, and the tightening it calls for, produce a regional break in leverage.

Over 2022, the Eco3min classifier returns the state Inflationary Pressure (G= I+): neutral growth (CFNAI-MA3 around −0.22, never in contraction territory), high underlying inflation (Trimmed Mean PCE above 2.75%). This reading is literal: it follows from the engine’s U.S. inputs (growth, inflation, financial conditions), within the window in which it has been backtested (2003 onward).

The overlay, for its part, stays neutral. Financial conditions as measured by the Chicago Fed’s NFCI do not turn restrictive, and none of the three signals of the dollar-funding-shortage regime (broad dollar, financial conditions, high-yield credit spreads) aligns durably. The strong dollar of 2022 stems from a rate differential, not from a drying-up of dollar funding — unlike 1997, 1998 or 2008. The gilt crisis does not activate the Dollar Shortage channel: it stays contained within the sphere of the gilt and sterling.

The UK regime, by contrast, is not an engine output. UK inflation peaks at 11.1% in October 2022 (ONS): this is contextual colour, not a computed state. The classifier reads U.S. and global inputs, not the UK price index — and this page’s “measured” mark applies to the U.S. regime, never to the regime of the United Kingdom.

The transmission chain is then mechanical. UK defined-benefit pension funds hedge their long-term liabilities through so-called LDI strategies, backed by leveraged gilt positions. The rise in long yields depreciates the gilts serving as collateral, triggers margin calls, and forces the funds to sell gilts to meet them. Those sales push yields higher, amplifying the next round of margin calls: the loop is self-reinforcing. The mini-budget of 23 September, by adding a fiscal-credibility shock to already-strained duration, turned this spiral from a theoretical risk into a dislocation within a few sessions.

The cyclical destination of this crisis is thus the inflationary meta-regime of the Eco3min Atlas (the inflationary regime). This page describes the sequence of the regional shift; the Atlas page describes the destination state.

The central-bank response

The gilt crisis placed the Bank of England in a rare position: buying in the bond market at the very moment it was tightening policy. On 28 September it announced temporary purchases of long gilts, capped at £65 billion and calibrated up to £5 billion per session, over thirteen working days from 28 September to 14 October. Actual purchases stayed well below the cap — on the order of £19 billion, according to the Bank of England. The stated objective was not to cap yields, but to restore market functioning and break the forced-selling spiral.

The path of yields illuminates the reach, and the limit, of that intervention. The 30-year gilt retraced about 113 basis points on the day of the announcement, from 4.85% on 27 September to 3.72% on the 28th. But it climbed back toward 4.75% by the programme’s expiry on 14 October. Durable relief came only after the budgetary reversal of 17 October. The operation therefore halted the liquidity mechanism (the forced selling) without controlling the level of rates, which remained governed by the credibility of the fiscal path and by the broader monetary tightening. The distinction between financial stability and the monetary stance, which the central bank was keen to maintain, can be read directly in the curve.

In the background, the Federal Reserve pursued its tightening without inflection: the channel that had repriced global long duration, and set the stage for the UK fracture, did not close. The Bank of England, for its part, resumed its own tightening once the dislocation was contained.

The European Central Bank followed a parallel path (end of net asset purchases and first rate hikes in the summer of 2022) without the UK dislocation turning into a euro-area funding strain. The perimeter of the intervention is telling: a central bank bought its own sovereign’s bonds to restore a market, whereas dollar-shortage crises call instead for international coordination and the reopening of swap lines. Nothing of the sort in 2022, which confirms, on the central-bank side, the regional character of the episode.

Assets and markets

The shock concentrated on two UK assets: the long gilt and sterling. The 30-year gilt, starting from around 2.3% in early August, jumped more than 110 basis points in three sessions after the mini-budget to peak at 4.85% on 27 September. Sterling, already weakened by the rate gap with the United States, fell to $1.07 at the close on 26 September — a record closing low. The gilt’s retracement on the day of the intervention, as sharp as the rise that preceded it, measures the size of the “forced selling” component in the dislocation.

The contrast with the violence of the bond shock lies in what did not spread. Equities and credit outside the United Kingdom did not break; volatility stayed concentrated on long gilts and sterling. Above all, the dollar-funding channel, the one that had turned 1997, 1998 and 2008 into global crises, did not activate: the Federal Reserve’s swap lines were not drawn in crisis volumes, and currency-funding spreads stayed away from stress peaks. It is precisely that absence which justifies, on the Eco3min side, an overlay that stayed neutral despite the intensity of the UK episode. The dislocation was acute, but narrow.

The trajectories and levels described here are retrospective, for historical analysis. They are neither a projection nor an investment recommendation, and past performance is not a reliable indicator of future performance.

What was different this time

The inflationary neighbourhood of the Crisis Hub is thin: apart from the 1973 oil shock, structurally distant, no other crisis in the hub shares the meta-regime destination of 2022. The most illuminating comparable is therefore external to the Crisis Hub: the 1994 bond rout, the “Great Bond Massacre”, chosen for its similarity of mechanism (a rapid central-bank tightening detonates a hidden rate-leverage structure), not for any identity of regime in the Eco3min sense.

As in 1994, the starting point is a sharp monetary tightening that reprices the long end of the curve and blows up leverage structures sensitive to rates. In 1994, the Federal Reserve raised its policy rate from about 3% to 5.5% over the year, the 30-year Treasury yield moved from 6.25% in late 1993 to a peak of 8.08% in November 1994, and several leveraged positions blew up — the bankruptcy of Orange County in December 1994, for a loss on the order of $1.7 billion, remains the illustration. The lineage with 2022 is direct.

Three structural factors nonetheless set the gilt crisis apart from 1994.

- The inflation backdrop. 1994 was a pre-emptive tightening in moderate inflation, on the order of 3%. 2022 was a measured inflationary regime, with UK inflation at 11%: the tightening responded to entrenched, not anticipated, inflation. The room central banks had to wait was not the same.

- The nature of the leverage. In 1994, leverage was dispersed — local authorities, hedge funds, derivatives positions. In 2022 it was concentrated and tied to pension liabilities, through LDI, and its collateral was the sovereign gilt itself: forced selling struck directly the very asset whose fall triggered the margin calls, hence the self-reinforcing character of the spiral.

- The central-bank response. In 1994, the Federal Reserve let the market adjust without a financial-stability intervention. In 2022, the Bank of England bought gilts on financial-stability grounds while tightening — a tension between two mandates that 1994 did not face.

What invalidated the analogy is measurable. In 1994, the shock spread as losses drawn out over time, without a breakdown in market functioning. In 2022, the LDI mechanism threatened to halt the gilt market within days and forced a central bank in the middle of tightening to buy bonds — the opposite of its stance. Leverage concentrated on sovereign collateral turned a duration repricing into a near-breakdown in liquidity, where 1994 had stayed a price adjustment.

One qualification is needed so as not to over-read. The comparison bears on the transmission mechanism, not on regime status: 1994 is not classified by the Eco3min engine and is not covered by the Crisis Hub. It serves as a structural reference point, to be checked against the primary sources of the period.

The Eco3min engine reads a U.S. inflationary regime in 2022; the gilt crisis remains a regional break in leverage, outside its measurement.

Where this crisis leads

The gilt crisis sits within a measured inflationary regime on the U.S. side, with no dollar-shortage overlay. The Atlas page describes its stable state; this page adds the sequence by which the tightening born of that regime fractured a regional pocket of leverage.

Over 2022, the United States is measured in an inflationary regime (G= I+): neutral growth, high underlying inflation. UK inflation at 11% remains contextual colour, not an engine output.

Atlas — inflationary regimeSources

- Bank of England — gilt yield curves (daily data), statements and financial-stability operations, September-October 2022.

- Federal Reserve (federal funds rate); Dallas Fed (Trimmed Mean PCE); Chicago Fed (NFCI).

- Office for National Statistics (ONS) — UK consumer price index, October 2022.

- Eco3min data: Trimmed Mean PCE, CFNAI-MA3, NFCI, federal funds rate, 30-year gilt yield, sterling/dollar exchange rate.

Last updated — 31 May 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.