The Federal Reserve’s Balance Sheet (2002–2026): Three Episodes That Required New Operational Tools

The Fed’s balance sheet expanded ten-fold from 2007 to 2022. Three episodes — 2008, 2019, 2020 — each required tools that did not previously exist in the FRBNY operational toolkit.

: A Complete Operating History — Eco3min Research")

A weekly dataset tracking the full operating history of the Federal Reserve’s balance sheet from 2002 to present, with phase classification covering all expansion and contraction programs and identification of three episodes that required deployment of new operational tools.

The Federal Reserve’s total assets (FRED series WALCL) have been published weekly as part of the H.4.1 release since December 2002. Over 1,221 weekly observations, the balance sheet expanded from $720 billion in 2002 to a peak of $8.97 trillion in April 2022, then contracted to $6.71 trillion by May 2026. This page provides the complete operating chronology of that expansion and identifies the three discrete episodes during which the Federal Reserve activated lending, repo, or asset-purchase facilities that had not previously existed in the FRBNY operational toolkit: the 2007–2008 crisis facility buildout, the September 2019 reserve management operations, and the March 2020 pandemic facilities.

The Federal Reserve’s balance sheet expanded approximately ten-fold between August 2007 ($866B) and April 2022 ($8,966B). Three episodes — the 2007–2008 crisis facility buildout, the September 2019 reserve management operations, and the March 2020 pandemic response — required deployment of operational tools (lending facilities, repo operations, or asset-purchase mechanisms) that had not previously existed in the FRBNY toolkit. Note: this dataset measures the asset side of the Fed’s balance sheet. It does not measure net liquidity available to markets, transmission of monetary policy, or the composition of holdings. For the net-liquidity framework, see Methodology and our paired Net Liquidity Index study.

Fed Total Assets

vs. Pre-2008 Mean ($802B)

From 2022 Peak (−25.2%)

Phase (post-QT-2)

- The Federal Reserve’s balance sheet expanded approximately ten-fold between August 2007 ($866 billion) and April 2022 ($8,966 billion). Across 1,221 weekly observations from December 2002 to May 2026, three episodes — 2007–2008, September 2019, and March 2020 — required deployment of operational tools (lending facilities, repo operations, or asset-purchase mechanisms) that had not previously existed in the FRBNY toolkit.

- During the first episode (December 2007 to November 2008), the balance sheet expanded from $882 billion to $2,187 billion — a 148% increase in approximately eleven months — driven by activation of the Term Auction Facility (TAF), Primary Dealer Credit Facility (PDCF), AMLF, CPFF, and TALF, alongside extraordinary support operations including Maiden Lane I/II/III.

- During the third episode (March 2020 to June 2020), the balance sheet expanded by $2,414 billion in 15 weeks, including a single 4-week period (ending April 8, 2020) when assets increased by $1,771 billion — the fastest absolute expansion ever recorded in the series.

- The September 2019 episode is the smallest of the three in dollar magnitude (+$208 billion over 11 weeks) but represented the first restart of overnight repo operations since 2008 and the first creation of a “reserve management purchase” program, which the Chair publicly distinguished from QE.

- As of May 2026, the balance sheet stands at $6.71 trillion, 25% below the April 2022 peak and approximately 8.4× the mean pre-crisis level. QT-2 ended on December 1, 2025, following an FOMC announcement on October 29, 2025. Total QT-2 runoff: −$2.38 trillion over 1,281 days.

1,221 weekly observations · Wednesday level · Dec 2002 – May 2026 · CC BY 4.0 ·

Methodology ·

Cite this dataset

Weekly Obs.

Peak / Aug 2007

All-Time Peak (Apr 2022)

Operational Intervention Episodes

Weeks of Intervention (6.2%)

Fastest 4-Week Δ (Apr 2020)

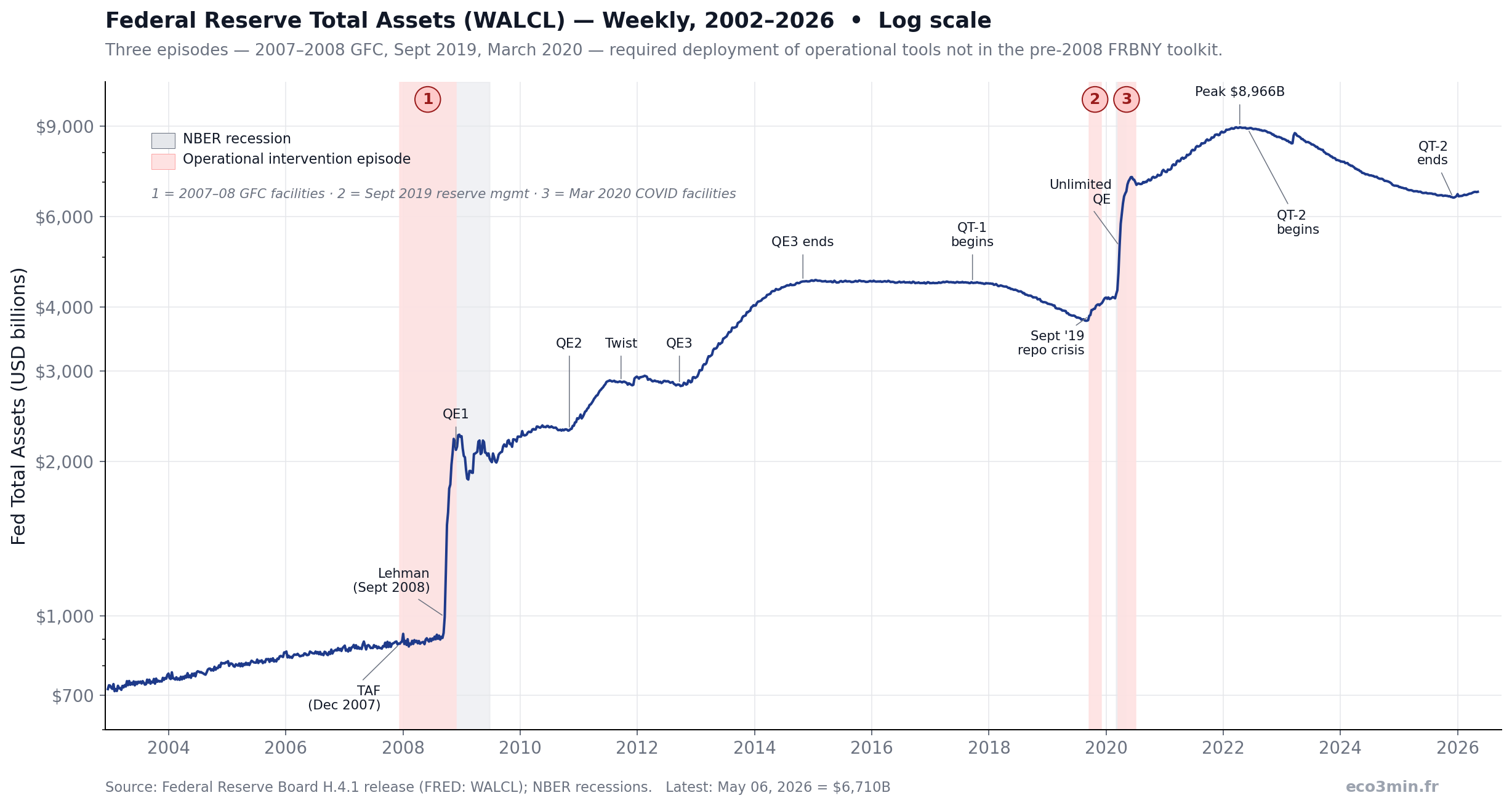

Chart: Federal Reserve Total Assets — Weekly, December 2002 to May 2026 (Log Scale)

Federal Reserve Total Assets (WALCL) — Weekly, 2002–2026

Three episodes of operational intervention — 2008, 2019, and 2020 — interrupt the broader QE/QT cycle and define the modern expansion of the balance sheet. That broader regime sequence is traced in the evolution of the Fed’s QE and QT regimes since 2008.

On a log scale, the three operational intervention episodes (shaded) are visible as the steepest segments of the expansion curve. The September 2019 episode is the smallest visible step; the COVID episode is the largest, including the single fastest absolute weekly expansion ever recorded.

Sources: Federal Reserve Board (H.4.1 release, FRED series WALCL); NBER recession dates. Chart: Eco3min Research.

{kind=link}

How to Read This Chart

The y-axis displays total Federal Reserve assets in U.S. dollars, on a logarithmic scale. A log scale is used because the series spans more than twelve-fold from minimum ($713 billion in early 2003) to peak ($8,966 billion in April 2022); on a linear scale, all detail from 2002 through 2008 would be visually compressed into a flat line near the x-axis. The supplementary linear view below preserves the magnitude impression for readers who prefer it.

The x-axis is calendar time, weekly observations on the Wednesday closing level. Shaded vertical bands mark the three operational intervention episodes (in red) and NBER recession periods (in gray). Labelled vertical lines mark each balance sheet program announcement: TAF (Dec 2007), QE1 (Nov 2008), QE2 (Nov 2010), Operation Twist (Sept 2011), QE3 (Sept 2012), QT-1 onset (Oct 2017), Sept 2019 reserve management operations, COVID emergency response (Mar 2020), QT-2 (Jun 2022), and the QT-2 conclusion (Dec 2025).

The full underlying weekly series is available as our paired dataset page. For the analytical framework that combines WALCL with Treasury cash balances and reverse repo operations, see our Net Liquidity Index study.

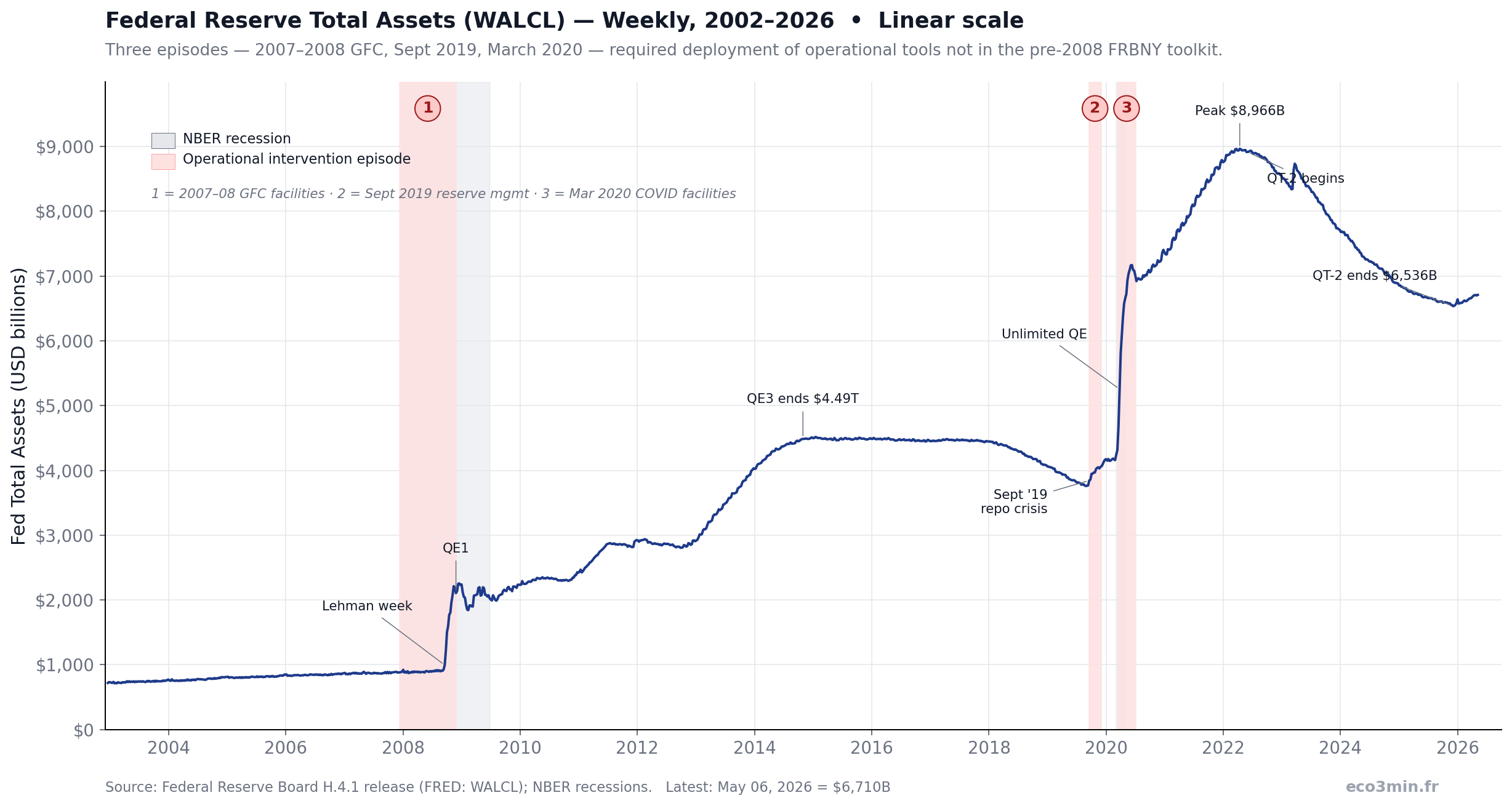

Supplementary View: Linear Scale

Federal Reserve Total Assets — Linear Scale, 2002–2026

On a linear scale, the pre-2008 era appears flat; the magnitude of the COVID expansion (+$4.3T in 24 months) dominates the visual.

— Eco3min Research")

Sources: FRED (WALCL). Chart: Eco3min Research.

{kind=link}

What WALCL Measures, and What It Does Not

The dominant retail framing describes the Fed’s balance sheet as “money printing” or “liquidity for markets.” Both descriptions are imprecise. WALCL is an accounting measure of one side of the consolidated balance sheet — total assets held by the Federal Reserve System, less inter-District eliminations. Whether bank reserves are created or destroyed depends on what the offsetting liabilities do.

Over the 2002–2026 sample, the total has moved from $720 billion to a peak of $8,966 billion and back to $6,710 billion. The composition of those assets has changed in parallel — from a portfolio of approximately 87% Treasury securities and small currency-management lending pre-2008, to a portfolio that briefly included $1.7 trillion of liquidity-facility lending in 2008, $2.7 trillion of agency MBS at its peak, and standing repo operations.

What this dataset measures. WALCL is the total of the Fed’s asset holdings — Treasury securities, agency MBS, lending under emergency facilities, repo agreements, and other items — published as part of the weekly H.4.1 release. It is reported as a Wednesday level in millions of U.S. dollars.

What this dataset does not measure. WALCL does not measure: (i) the net liquidity available to financial markets — that requires subtracting the Treasury General Account and reverse repurchase agreements (see our Net Liquidity Index study for the WALCL − TGA − RRP framework); (ii) the composition of holdings (Treasuries vs. MBS vs. facility loans) — the relevant series for that decomposition is TREAST for Treasuries () and WSHOMCB for MBS (); (iii) the effectiveness of monetary policy transmission to credit, employment, or inflation outcomes; (iv) the distributional consequences of large-scale asset purchases.

This page restricts itself to a single empirical question: how did the asset side of the Fed’s balance sheet evolve from 2002 to 2026, and during which discrete episodes did the Federal Reserve activate operational tools that did not previously exist? The forward returns table below uses the full sample to characterize equity returns conditional on balance sheet phase; it is descriptive, not causal.

WALCL grew approximately ten-fold between August 2007 and April 2022 ($866B → $8,966B). Three discrete episodes account for the activation of every operational tool not in the pre-2008 toolkit: 2007–2008 (lending facilities), September 2019 (repo operations + bill purchases), and March 2020 (pandemic facilities including PMCCF, SMCCF, MLF, MSLP). All other expansion programs (QE1, QE2, Twist, QE3, COVID-unlimited-QE) reused existing operational machinery.

The Three Operational Interventions, In Detail

Each episode is defined by the Federal Reserve’s deployment of a lending, repo, or asset-purchase facility that had not previously existed in the FRBNY operational toolkit. Each episode terminates when the deployed facilities are either superseded by an established program (e.g., QE) or wound down. The selection criterion, formal threshold, and sensitivity analysis are documented in the Methodology.

Episode 1 · The Crisis Facility Buildout (December 2007 – November 2008)

The Term Auction Facility (TAF), announced on December 12, 2007, was the first new lending tool. It was followed in March 2008 by the Primary Dealer Credit Facility (PDCF) and Term Securities Lending Facility (TSLF) in response to the Bear Stearns weekend; in September 2008 by the Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF) and Commercial Paper Funding Facility (CPFF); and in November 2008 by the Term Asset-Backed Securities Loan Facility (TALF). The Federal Reserve also extended approximately $30 billion in financing to facilitate the JPMorgan-Bear Stearns transaction and approximately $85 billion (initial) to AIG, structured through the Maiden Lane I/II/III LLCs.

Across the eleven months of this episode, WALCL increased from $882 billion to $2,187 billion — a 148% rise. A single six-week period (September 3, 2008 to October 15, 2008) accounts for an expansion from $905 billion to $1,771 billion — a 96% rise driven primarily by lending under the new facilities, with the announcement of the initial $600 billion QE1 program on November 25, 2008 effectively superseding the facility-led expansion.

The 2007–2008 episode introduced seven previously non-existent lending facilities (TAF, PDCF, TSLF, AMLF, CPFF, TALF, plus the Maiden Lane LLCs). Of the 50 weekly observations in the episode, 47 (94%) overlap an NBER recession period.

Episode 2 · September 2019 Reserve Management Operations (September 17 – November 30, 2019)

On the morning of September 16–17, 2019, the overnight Secured Overnight Financing Rate (SOFR) spiked from approximately 2.2% to an intraday high near 10%, well above the Federal Funds rate’s upper bound of 2.25%. The Federal Reserve Bank of New York announced the same day that it would conduct overnight repurchase operations — the first such operations since the 2008 GFC. On October 11, 2019, Federal Reserve Chair Jerome Powell announced an open market purchase program of Treasury bills at an initial pace of approximately $60 billion per month, which he explicitly distinguished from quantitative easing, characterizing it as “reserve management purchases” ().

Over the eleven weeks of this episode, WALCL increased from $3,845 billion to $4,053 billion, an expansion of $208 billion (+5.4%). The expansion was small in absolute terms relative to the other two episodes but operationally distinct in that it represented the first deployment of overnight repo operations as a standing tool in over a decade. The episode is conventionally interpreted in the academic literature as evidence that bank reserves had become scarce relative to the demand created by Treasury issuance, dealer balance sheet constraints, and the growth of money market mutual fund assets ().

The September 2019 episode is the smallest of the three by dollar magnitude (+$208B over 11 weeks) and ended without superseding into a new QE program. It was, however, the first reactivation of overnight repo as a standing operational tool since 2008, and the first introduction of the “reserve management purchases” framework which the Chair publicly distinguished from QE.

Episode 3 · The Pandemic Facility Activation (March 15 – June 30, 2020)

Between March 15 and March 23, 2020, the Federal Reserve announced the largest sequence of new operational tools in its history. The list included the reactivation of the CPFF and PDCF (last used in 2008), the new Primary Market Corporate Credit Facility (PMCCF), the Secondary Market Corporate Credit Facility (SMCCF), the Money Market Mutual Fund Liquidity Facility (MMLF), the Term Asset-Backed Securities Loan Facility (TALF, reactivated), the Municipal Liquidity Facility (MLF), the Main Street Lending Program (MSLP), and an unlimited Treasury and agency MBS purchase commitment. The SMCCF and PMCCF were operationally novel in that they provided for direct Federal Reserve purchase of corporate bonds — a tool the central bank had not previously deployed in the United States — using Treasury-provided indemnification under the CARES Act. On this point: The Eco3min framework on how QT and monetary plumbing shape market liquidity.

Across the fifteen weeks of this episode, WALCL increased from $4,668 billion to $7,082 billion — an expansion of $2,414 billion, or 52%. A single 4-week period (week ending April 8, 2020) accounts for an increase of $1,771 billion, the fastest absolute 4-week expansion in the entire 1,221-observation series. By comparison, the previous record (set during the GFC episode, week ending October 15, 2008) was $776 billion, less than half the COVID-era pace.

The March 2020 episode produced both the fastest absolute expansion ever recorded (+$1,771B in 4 weeks ending April 8) and the introduction of direct Federal Reserve corporate bond purchases (PMCCF/SMCCF), operationalized under Treasury indemnification provisions of the CARES Act.

Comparison Table

| Episode | Window | Weeks | WALCL Δ (USD bn) | % Change | Fastest 4-week Δ | New Operational Tools |

|---|---|---|---|---|---|---|

| 1. GFC facilities | Dec 12, 2007 – Nov 19, 2008 | 50 | +$1,305 | +148% | +$776 (Oct 15, 2008) | TAF, PDCF, TSLF, AMLF, CPFF, TALF, Maiden Lane I/II/III |

| 2. Sept 2019 reserve mgmt | Sept 17 – Nov 27, 2019 | 11 | +$208 | +5.4% | +$184 (Oct 2, 2019) | Standing overnight repo (first since 2008), bill purchase program (“reserve management purchases”) |

| 3. Pandemic facilities | Mar 18 – Jun 24, 2020 | 15 | +$2,414 | +52% | +$1,771 (Apr 8, 2020) | PMCCF, SMCCF, MMLF, MLF, MSLP, reactivated CPFF/PDCF/TALF, unlimited UST/MBS |

Tool Innovation as the Central Banking Norm: A Steelman

A legitimate analytical qualification of the framing above is that the three episodes can equally be read as evidence of the Federal Reserve responding effectively to novel stress configurations, rather than evidence of repeated system fragility. New tools are how central banking has historically operated. The Bank of England developed the discount window in the 19th century in response to recurrent banking panics. The European Central Bank designed OMT and TLTRO in response to the 2010–2012 sovereign debt crisis. The deployment of new tools is the default response of a central bank confronted with a new transmission failure.

On this reading, each of the three episodes documents a successful intervention rather than a near-failure. The 2008 facilities are widely credited in the academic literature with preventing a wholesale-funding-driven contraction that the Fed itself later estimated would have produced output losses comparable in magnitude to the 1929–1933 episode (). The September 2019 operations restored repo market function within 48 hours of the SOFR spike. The March 2020 facilities prevented a Treasury market dysfunction event that BIS staff economists subsequently described as the most acute liquidity disruption in the cash Treasury market in recent decades ().

The narrower factual claim of this page is therefore: three discrete episodes during which the Federal Reserve deployed operational facilities that had not previously existed in the FRBNY toolkit. Whether those interventions reflect institutional fragility, institutional capacity, or both is a question on which this dataset is silent.

In each of the three episodes, the operational interventions appear to have restored the targeted market function rapidly. SOFR returned to the Federal Funds corridor within 48 hours of the September 2019 operations. The Treasury bid-ask spread for off-the-run 30-year bonds — which had widened from approximately 1 basis point to over 20 basis points during the week of March 12, 2020 () — returned to pre-crisis ranges within four weeks of the SMCCF and unlimited QE announcements.

Forward Equity Returns by Balance Sheet Phase

The table below summarizes S&P 500 forward 6-month and 12-month returns conditional on the Fed balance sheet phase prevailing at the observation date. Phases are grouped into five broad regimes; the full mapping is documented in the Methodology. These are descriptive statistics, not causal estimates. The relationship between balance sheet phase and equity returns is mediated by many other variables (real rates, credit conditions, inflation regime, geopolitical events).

| Balance Sheet Regime | n | Median 6m | Median 12m | IQR (P25–P75) | % Positive 12m | Median 12m MDD |

|---|---|---|---|---|---|---|

| Pre-2008 (small BS) | 260 | +5.3% | +8.7% | +4.0% to +13.0% | 82% | −7.0% |

| Active Expansion (QE / Facilities) | 426 | +7.0% | +12.6% | +1.4% to +21.5% | 77% | −9.6% |

| Maintenance / Stable BS | 199 | +5.8% | +12.7% | +2.6% to +16.8% | 82% | −8.2% |

| Active Contraction (QT) | 258 | +6.6% | +14.6% | +7.1% to +22.1% | 93% | −12.3% |

| Reserve Management Sept 2019 (small n) | 26 | −3.0% | +15.6% | +14.6% to +16.6% | 100% | −29.2% |

The descriptive statistics offer no support for the popular framing that QE phases are systematically associated with higher equity returns than QT phases. Median 12-month returns are higher during Active Contraction regimes (+14.6%, n=258) than during Active Expansion regimes (+12.6%, n=426). This is a confounding result driven by the specific timing of the QT periods (2017–2019 bull market; 2022–2025 AI-driven bull market) and should not be read as a causal claim. The point is the opposite: the balance sheet phase is a poor stand-alone predictor of equity returns.

Methodological notes: Forward returns use overlapping 26-week and 52-week windows, which inflates effective autocorrelation; the 95% confidence intervals are wider than the bare standard errors would suggest. The “Reserve Management” regime (n=26) is dominated by the September 2019 episode, which leads directly into the COVID drawdown — the median MDD of −29% reflects this single confounding event, not a stable regime characteristic. Pre-2008 returns end before May 2007 to ensure the 52-week forward window does not overlap the Crisis Facility Buildout period.

Past distributions are not predictive of future outcomes. Regime-conditional statistics describe historical patterns, not expected returns.

- ▸ Reserve scarcity threshold: the September 2019 episode was triggered when bank reserves fell to approximately $1.4 trillion. Current reserve levels (as of May 2026, approximately $3.0 trillion ) are above that 2019 level but declining as ongoing MBS runoff continues. If reserves were to approach $2.5 trillion, the regime would historically have been associated with elevated repo market volatility.

- ▸ MBS runoff continuation: the FOMC’s October 29, 2025 announcement ceased Treasury runoff but left agency MBS runoff in place. As of April 2026, the Fed held approximately $1.99 trillion in MBS (), down from $2.71 trillion at QT-2 onset. The pace of MBS runoff is sensitive to refinancing activity; sustained mortgage rates above 6.5% slow runoff materially. See our 30-Year Mortgage Rate dataset.

- ▸ Next H.4.1 release: Thursday, May 14, 2026, 4:30 PM ET. The H.4.1 (“Factors Affecting Reserve Balances”) is published weekly and is the primary source for WALCL updates.

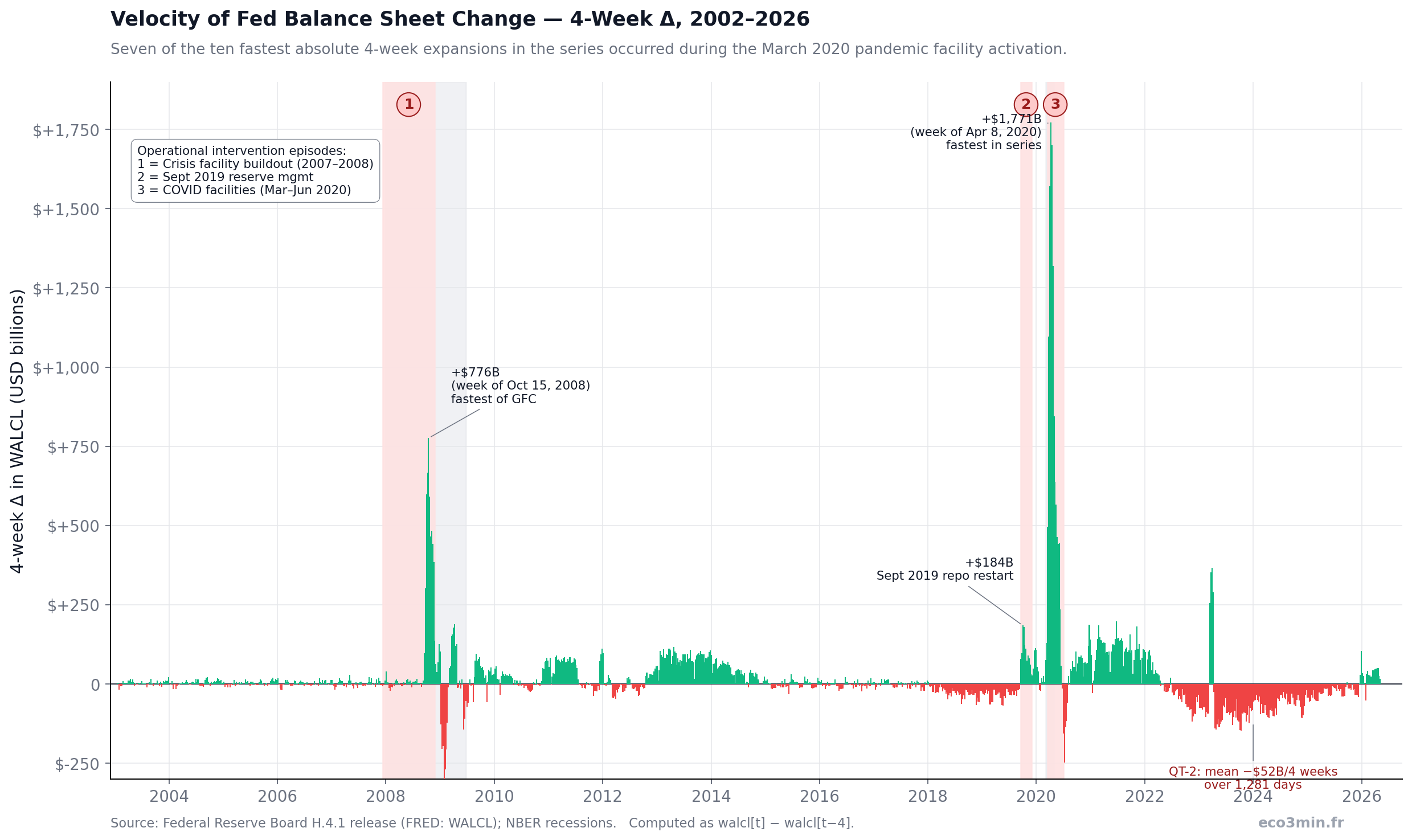

Expansion and Contraction Velocity

Weekly 4-Week Δ in Fed Balance Sheet (USD billions) — 2002–2026

Seven of the ten fastest absolute 4-week expansions in the entire series occurred during the March 2020 pandemic facility activation.

The April 2020 expansion ($1,771 billion in 4 weeks, week ending April 8) exceeded the GFC peak ($776 billion in 4 weeks, week ending October 15, 2008) by a factor of 2.3×. QT-2 produced a sustained but modest negative profile, averaging −$52 billion per 4-week window over 1,281 days.

Sources: FRED (WALCL). Chart: Eco3min Research.

{kind=link}

Regime Classification by Velocity

Crisis pace. Observed only during the GFC and COVID episodes. 26 weekly observations in the full sample.

Active expansion (standard QE pace). Observed throughout QE1, QE2, QE3, COVID maintenance phase. 272 weekly observations.

Maintenance / stable BS. Observed during Operation Twist (designed to be size-neutral), QE pauses, the long 2014–2017 plateau, and reinvestment phases. 707 weekly observations.

Active contraction. Observed only during QT-1 and QT-2. 212 weekly observations across both programs.

Historical Turning Points

December 12, 2007 — Term Auction Facility announcement

The TAF was the first new lending tool introduced in response to the August 2007 freeze of the asset-backed commercial paper market. WALCL on the announcement date stood at $881.8 billion. The facility was structured as an auction-priced lending program with eligible collateral broader than the standing discount window. The Federal Reserve did not yet describe its actions as “extraordinary.”

September 17, 2008 — Lehman week / AIG bridge / AMLF

The week of Lehman Brothers’ bankruptcy (Monday, September 15, 2008) and the AIG conservatorship (Tuesday, September 16) saw WALCL increase from $925.7 billion (September 10) to $995.1 billion on the Wednesday observation. The Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF) was announced September 19. Across the four weeks following Lehman, WALCL increased by $776 billion to reach $1,770.8 billion by October 15 — the fastest 4-week expansion of the GFC episode.

November 25, 2008 — QE1 announcement

The initial QE1 program ($600 billion in MBS and agency debt purchases) was announced on a Tuesday. The Wednesday observation that week saw WALCL at $2,106.1 billion — approximately 2.4× the August 2007 level. QE1 was subsequently expanded on March 18, 2009, to include $300 billion of long-term Treasury purchases. WALCL on March 18, 2009 stood at $2,066.9 billion. The closing observation of the active purchase period (April 28, 2010) was $2,330.5 billion.

September 17, 2019 — Repo crisis week

The Wednesday observation for the week of the SOFR spike showed WALCL at $3,844.7 billion. Overnight repo operations were announced and conducted by the New York Fed beginning the same morning. Chair Powell’s bill purchase program announcement on October 11, 2019 was followed by an observation on October 9 of $3,950.0 billion. The episode terminated by end-November 2019 at WALCL of $4,052.9 billion.

March 25, 2020 — Unlimited QE week

The “unlimited” QE announcement of March 23, 2020 was followed by a Wednesday observation of $5,254.3 billion — an increase of $1,096 billion in the four weeks since February 26, 2020. The 4-week expansion peaked at $1,771 billion for the week ending April 8, 2020 (WALCL of $6,083.1 billion). By the close of the pandemic facility episode on June 24, 2020, WALCL stood at $7,082.3 billion — an increase of $2,414 billion over fifteen weeks.

April 13, 2022 — All-time peak

WALCL reached its all-time peak of $8,965.5 billion. The first rate hike of the post-COVID tightening cycle had occurred on March 16, 2022. The FOMC’s plans for balance sheet reduction (QT-2) were finalized at the May 2022 meeting, and runoff began on June 1, 2022.

December 3, 2025 — QT-2 conclusion (first Wednesday after)

The FOMC announced on October 29, 2025 that securities runoff would cease effective December 1, 2025. The first weekly observation after the cessation showed WALCL at $6,535.8 billion — a decline of $2,379 billion from the QT-2 start level of $8,915 billion (June 1, 2022) over 1,281 days. The runoff schedule had been progressively slowed: from $95 billion/month combined cap initially, to $60 billion in mid-2024, to $40 billion in April 2025, to $25 billion in mid-2025 ().

May 6, 2026 — Current observation

WALCL stands at $6,709.5 billion, approximately 25.2% below the April 2022 peak and approximately 8.4× the pre-2008 mean ($802 billion). The current phase is “Reinvestment / Steady-State” — Treasury runoff ceased December 1, 2025; agency MBS proceeds continue to be reinvested into Treasury bills under the policy announced October 29, 2025. The year-over-year change in WALCL is approximately zero, consistent with the policy intent.

Methodology

This dataset compiles the weekly Wednesday level of total Federal Reserve System assets from December 18, 2002 to May 6, 2026, with proprietary phase classification and an operational-intervention indicator constructed from primary-source FOMC and FRBNY announcements.

Source Series

Source: Federal Reserve Board H.4.1 release. Weekly, Wednesday level.

Units: Millions of U.S. dollars (converted to billions in this dataset).

Operational Intervention Selection Criterion

Federal Reserve activated a lending, repo, or asset-purchase facility that had not previously

existed in the FRBNY operational toolkit as of the start of that period.

Episode starts on the announcement date of the first qualifying new facility.

Episode ends on the earlier of:

(a) the announcement date of a successor program that supersedes facility-led

expansion (e.g., QE1 announcement supersedes Episode 1), or

(b) the formal termination or final tapering of all qualifying facilities.

Applied mechanically to the 2002–2026 sample, the criterion identifies exactly three episodes:

- Episode 1 (Dec 12, 2007 – Nov 24, 2008): Initiated by TAF (Dec 12, 2007). New facilities introduced during the episode: TAF, PDCF, TSLF, AMLF, CPFF, TALF, and Maiden Lane I/II/III. Terminated by the QE1 announcement (Nov 25, 2008), which superseded facility-led expansion with a Treasury/MBS purchase program operating through existing System Open Market Account machinery.

- Episode 2 (Sept 17, 2019 – Nov 30, 2019): Initiated by FRBNY restart of overnight repo operations (Sept 17, 2019, first since 2008). Joined by the “reserve management purchase” bill purchase program (announced Oct 11, 2019). Terminated administratively at end-November 2019; transitions into the COVID episode in early March 2020.

- Episode 3 (Mar 15, 2020 – Jun 30, 2020): Initiated by the Mar 15, 2020 emergency rate cut and concurrent facility announcements. New facilities introduced: PMCCF, SMCCF, MMLF, MLF, MSLP. Reactivated facilities: CPFF, PDCF, TALF. Terminated on Jun 30, 2020 (formal end of new facility lending; existing positions ran off through 2021).

Sensitivity. The criterion would identify the same three episodes if the definition were broadened to “new or reactivated emergency facility that had not been in active use during the preceding three years.” It would not pick up additional episodes if narrowed to “facility involving direct Federal Reserve purchase of private-sector securities” (which would exclude Episode 1, leaving only Episode 3). Restricting the criterion to “new facility that had never existed at any prior point in Federal Reserve history” would retain Episode 1 (all listed facilities were genuinely new) and Episode 3 (PMCCF/SMCCF/MSLP were new) but would exclude Episode 2 (overnight repo had existed pre-2008).

Phase Classification

Each weekly observation is assigned to one of 15 mutually exclusive phases based on the date of the most recent FOMC announcement governing balance sheet operations. The phase boundaries are documented in the CSV column phase_id. The phase assignment is announcement-date based and does not look forward — it can be reproduced in real time on each Wednesday.

Phases are grouped into five broad regimes for the forward-returns table:

- Pre-2008 Regime (small BS): Pre-Crisis phase only (Dec 2002 – Dec 11, 2007).

- Active Expansion (QE / Facilities): Crisis-Facility-Buildout, QE1, QE2, Operation-Twist (despite size neutrality, included by FOMC framing), QE3, COVID-Unlimited-QE.

- Maintenance / Stable BS: Post-QE1-Maintenance, Pause-Pre-Twist, Maintenance-2014-2017, Pandemic-Maintenance, Reinvestment-Steady-State.

- Active Contraction (QT): QT-1, QT-2.

- Reserve Management Sept 2019: Reserve-Mgmt-Plus-Bills phase only (small-n caveat applies).

Forward Returns

S&P 500 forward returns are computed using daily closing prices (Yahoo Finance ticker ^GSPC) matched to each WALCL Wednesday by forward-fill from the most recent prior trading day. Forward 6-month returns use a 26-week look-ahead; forward 12-month returns use a 52-week look-ahead. The “Median 12m MDD” column reports the median maximum drawdown of the S&P 500 over the 52 weeks following each observation, computed as the minimum peak-to-trough percentage decline within the forward window. NaN values for the most recent observations where the forward window has not elapsed.

Dataset Design

| Variable | Type | Unit | Source | Calculation |

|---|---|---|---|---|

date | date | YYYY-MM-DD | FRED | Wednesday level date |

walcl_usd_bn | float | USD billions | FRED (WALCL) | Direct (millions ÷ 1000) |

delta_4wk_usd_bn | float | USD billions | derived | walcl[t] − walcl[t−4] |

delta_13wk_usd_bn | float | USD billions | derived | walcl[t] − walcl[t−13] |

delta_52wk_usd_bn | float | USD billions | derived | walcl[t] − walcl[t−52] |

walcl_yoy_pct | float | % | derived | 100 × (walcl[t] / walcl[t−52] − 1) |

multiple_of_pre_crisis | float | ratio | derived | walcl[t] / 802.4 (pre-crisis mean 2002–2007) |

phase_id | categorical | — | Eco3min classification | 15 phases (see above) |

operational_intervention_active | boolean | — | Eco3min classification | True during 3 episode windows |

operational_intervention_label | str | — | Eco3min classification | Episode-1/2/3 labels |

nber_recession | boolean | — | FRED (USREC, ffilled) | NBER monthly indicator, weekly forward-fill |

sp500_wed | float | index | Yahoo (^GSPC) | Close on Wed or last prior trading day |

sp500_fwd_6m_pct | float | % | derived | 100 × (sp500[t+26] / sp500[t] − 1) |

sp500_fwd_12m_pct | float | % | derived | 100 × (sp500[t+52] / sp500[t] − 1) |

sp500_fwd_12m_mdd | float | % | derived | Min peak-to-trough drawdown over [t, t+52] |

Python Reproduction Code

# Reproduce this dataset from primary sources import pandas as pd import pandas_datareader.data as web import yfinance as yf # 1. Fetch WALCL weekly Wednesday from FRED walcl = web.DataReader("WALCL", "fred", "2002-12-01") walcl = walcl.rename(columns={"WALCL": "walcl_usd_m"}) walcl["walcl_usd_bn"] = walcl["walcl_usd_m"] / 1000 # 2. Fetch NBER recession indicator (monthly) usrec = web.DataReader("USREC", "fred", "2002-01-01") # 3. Fetch S&P 500 daily sp = yf.download("^GSPC", start="2002-12-01", auto_adjust=False) sp = sp["Close"].rename("sp500") # 4. Compute deltas and YoY walcl["delta_4wk_usd_bn"] = walcl["walcl_usd_bn"] - walcl["walcl_usd_bn"].shift(4) walcl["walcl_yoy_pct"] = 100 * (walcl["walcl_usd_bn"] / walcl["walcl_usd_bn"].shift(52) - 1) # 5. Assign phases by announcement date (see paper for full list) phases = [ ("2002-12-18", "Pre-Crisis"), ("2007-12-12", "Crisis-Facility-Buildout"), ("2008-11-25", "QE1"), # ... (full list in paper Methodology) ] # Apply phase assignment by date matching # 6. Flag operational intervention windows # Episode 1: 2007-12-12 to 2008-11-24 # Episode 2: 2019-09-17 to 2019-11-30 # Episode 3: 2020-03-15 to 2020-06-30

Dataset Download & Reproducibility

1,221 weekly observations · Weekly Wednesday level · December 18, 2002 to May 6, 2026 · Licensed under CC BY 4.0.

Data Sources & References

- Primary Board of Governors of the Federal Reserve System, “Factors Affecting Reserve Balances of Depository Institutions” (Statistical Release H.4.1). FRED series WALCL: “Assets: Total Assets (Less Eliminations from Consolidation): Wednesday Level”. Retrieved May 12, 2026.

- Primary Federal Reserve Bank of New York, “Statement Regarding Repurchase Operations,” September 17, 2019; subsequent operations through November 30, 2019.

- Primary Federal Reserve Board, “Federal Reserve issues FOMC statement,” October 11, 2019 (announcing reserve management purchases of Treasury bills).

- Primary Federal Reserve Board, FOMC statements and press releases: March 15, 2020; March 23, 2020 (unlimited QE and primary/secondary corporate credit facilities); October 29, 2025 (cessation of QT-2 securities runoff, effective December 1, 2025).

- Research Ben S. Bernanke (2018), “The Real Effects of the Financial Crisis,” Brookings Papers on Economic Activity, Fall 2018.

- Research Andreas Schrimpf, Hyun Song Shin, Vladyslav Sushko (2020), “Leverage and margin spirals in fixed income markets during the Covid-19 crisis,” BIS Bulletin No. 2, April 2020.

- Research Darrell Duffie (2020), “Still the World’s Safe Haven? Redesigning the U.S. Treasury Market After the COVID-19 Crisis,” Hutchins Center Working Paper #62, Brookings Institution.

- Research Gara Afonso, Marco Cipriani, Adam Copeland, Anna Kovner, Gabriele La Spada, Antoine Martin (2020), “The Market Events of Mid-September 2019,” NY Fed Staff Reports No. 918.

- Reference Lorie K. Logan (2019), Speech at the 2019 U.S. Treasury Market Conference, FRBNY, September 23, 2019 (on reserve scarcity and Treasury market structure).

- Reference National Bureau of Economic Research, Business Cycle Dating Committee: US recession dates (FRED series USREC).

Methodological Limitations

- The H.4.1 release format and accounting treatment changed in 2002 and again in 2009 (consolidation of Maiden Lane and other Section 13(3) facilities). Pre-2002 WALCL data is published only in summary form and is not directly comparable. This is why the dataset begins December 18, 2002.

- The “operational intervention” classification reflects an editorial judgment about which facilities count as “new tools.” Borderline cases (e.g., classifying Operation Twist as expansion despite size-neutrality; treating the 2019 bill purchase program as separate from QE despite identical purchase mechanics) are documented in the Methodology. A reasonable analyst could redraw the boundaries.

- Phase IDs are assigned at the announcement date of the relevant FOMC statement. Actual implementation lagged announcement by a median of approximately 2 weeks. For high-frequency analysis, the announcement-date assignment may introduce small timing errors in regime classification.

- Forward returns are computed over overlapping windows (26 and 52 weeks), which inflates effective autocorrelation. Confidence intervals on regime-conditional medians are wider than naive standard errors suggest.

- The “Reserve Management Sept 2019” regime has only 26 weekly observations (n < 30 threshold for stable inference) and is dominated by the COVID drawdown that immediately followed. Forward-return statistics for this regime should be treated as descriptive of a single episode, not as a stable conditional distribution.

- NBER recession dates are subject to retrospective redating. The recession indicator forward-fills the monthly USREC series to weekly frequency; observations within 2–4 weeks of a recession boundary may be ambiguously classified.

Frequently Asked Questions

What is the current size of the Fed’s balance sheet?

As of the Wednesday observation for May 6, 2026, the Federal Reserve’s total assets (FRED series WALCL) stand at $6.71 trillion. This is approximately 25% below the April 13, 2022 peak of $8.97 trillion and approximately 8.4× the pre-2008 mean level of $802 billion. The current phase is “Reinvestment / Steady-State” — Treasury securities runoff ceased on December 1, 2025 following the FOMC’s October 29, 2025 announcement; agency MBS proceeds are being reinvested into Treasury bills.

Why does this dataset start in December 2002?

The H.4.1 release in its current format and consolidation methodology began publication on December 18, 2002. Pre-2002 balance sheet data is available from the Federal Reserve in archived paper releases, but the accounting treatment of factors affecting reserve balances differs in ways that complicate direct comparison. To preserve dataset integrity, we begin the series with the first publication under the modern format.

Does an expanding Fed balance sheet automatically mean rising equity prices?

The descriptive statistics in this dataset do not support that claim. Over the 2002–2026 sample, the median 12-month forward S&P 500 return is actually higher during Active Contraction (QT) phases (+14.6%, n=258) than during Active Expansion (QE / Facilities) phases (+12.6%, n=426). This counterintuitive result is driven by the specific timing of the QT periods (2017–2019 and 2022–2025, both bull markets) and should not be interpreted causally — but it is sufficient to falsify the simple “QE = stocks up” framing. The relationship between balance sheet phase and equity returns is mediated by many other variables. For an analytical framework that combines WALCL with offsetting liabilities, see our Net Liquidity Index study.

How is “operational intervention episode” defined? Why exactly three?

The selection criterion is documented in the Methodology: a period during which the Federal Reserve activated a lending, repo, or asset-purchase facility that had not previously existed in the FRBNY operational toolkit at the start of that period. Applied mechanically to the December 2002 – May 2026 sample, the criterion identifies exactly three episodes: December 2007 – November 2008 (TAF, PDCF, TSLF, AMLF, CPFF, TALF, Maiden Lane); September – November 2019 (overnight repo restart + reserve management bill purchases); March – June 2020 (PMCCF, SMCCF, MMLF, MLF, MSLP plus reactivations). QE1, QE2, QE3, Operation Twist, and COVID-unlimited-QE do not qualify under this criterion because they reused existing SOMA purchase machinery — they were new programs, not new tools. The sensitivity analysis in the Methodology shows the count is robust to reasonable alternative definitions.

What is the difference between WALCL and “Net Liquidity”?

WALCL measures the asset side of the Fed’s consolidated balance sheet — total securities holdings, lending under facilities, and other assets. “Net Liquidity” is a derived composite that subtracts two large Fed liabilities — the Treasury General Account (TGA, FRED series WTREGEN) and overnight reverse repurchase agreements (ON RRP, FRED series RRPONTSYD) — from WALCL. The intuition is that cash held at the Fed by the Treasury, or parked overnight by money market funds, is not circulating in private credit markets. Empirically, net liquidity has historically tracked equity prices more closely than WALCL alone. See our paired Net Liquidity Index study for the full framework. This page restricts itself to documenting WALCL itself and does not endorse a causal interpretation of either WALCL or net liquidity as a market driver.

Did QT-2 cause repo market stress in 2025, similar to September 2019?

Available evidence suggests yes — but at a magnitude well below the 2019 episode. Through Q3–Q4 2025, the spread between SOFR and the Fed’s reverse repo rate widened on multiple occasions, and the Standing Repo Facility (created in July 2021 specifically to prevent a repeat of September 2019) saw elevated usage. The FOMC’s October 29, 2025 announcement to cease securities runoff explicitly cited “money market conditions suggesting that reserve levels were approaching the ample level” as a justification. The Standing Repo Facility’s existence meant that, unlike in 2019, no new operational tool was required to address the stress — which is why the period of late 2025 does not qualify as a fourth “operational intervention episode” under this dataset’s criterion.

Source

Related Eco3min Research

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.