WALCL: QE and QT Regimes 2008-2026, Evolution of Fed Balance-Sheet Doctrine

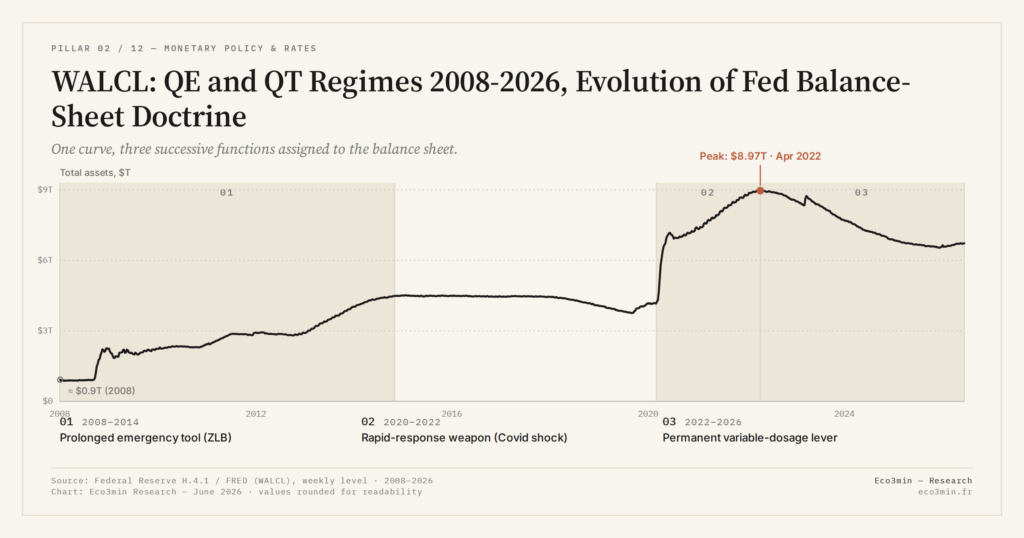

Over fifteen years, the Fed has shifted the function it assigns to its balance sheet: prolonged emergency tool against the ZLB (2008-2014), rapid-response weapon to the Covid shock (2020-2022), then permanent variable-dosage lever (2022-2026). Three distinct doctrinal regimes.

TL;DR

Across fifteen years the FOMC has assigned WALCL three different functions, a doctrinal shift legible in its Statements and vocabulary far more than in the chronology of its tools.

- Regime 1 (2008-2014) framed the balance sheet as exceptional and temporary, with FOMC language ("stimulating activity through lower long-term yields," "supporting the housing market") keeping it subordinate to the dual mandate.

- Regime 2 (2020-2022) doubled WALCL in three months, an unprecedented move, then dropped the "temporary" framing for "supporting the smooth functioning of markets," normalizing a permanently elevated Fed footprint.

- Regime 3 (2022-2026) was set by the May 2022 Principles for Reducing the Size of the Balance Sheet, targeting a terminal size aligned with the ample reserves regime adopted in January 2019, not a pre-2008 return.

- QE3 (September 2012) introduced open-ended purchases calibrated on labor-market conditions, making the balance sheet a data-dependent tool distinct from earlier fixed-target programs.

The balance sheet’s doctrinal evolution reads through FOMC Statements, successive Longer-Run Goals, and communication rhetoric, not through the chronology of operational tools.

The history of WALCL since 2008 is not a continuous chronology of purchases and sales: it is a succession of three distinct doctrinal regimes, each characterized by a different function the Fed assigns to its balance sheet. This doctrinal reading is explicitly distinct from the operational chronology of tools deployed 2002-2026, which enumerates programs (TALF, MMLF, PMCCF, BTFP, SRF) and their technical parameters. The two readings are complementary but distinct: one answers “What tools did the Fed use?”, the other answers “How did the Fed conceive its balance sheet as an instrument?”. the distinction between balance-sheet size and QE sets out the mechanism in detail.

The distinction matters analytically. An identical WALCL trajectory in dollar value can reflect very different doctrines depending on the concepts mobilized by the FOMC in its Statements, Minutes, and Statement on Longer-Run Goals. Understanding these conceptual evolutions allows reading the Fed’s effective monetary stance via the balance sheet beyond the pure mechanics of purchases and sales.

Regime 1 (2008-2014): the balance sheet as prolonged emergency tool

The first regime’s doctrine is built progressively between November 2008 and October 2014, as the Fed develops a theoretical justification for the active use of its balance sheet. The central concept is the balance sheet as substitute for the policy rate at the effective lower bound. When the Fed Funds rate hit 0-0.25% in December 2008, the traditional transmission channel through rates was neutralized. The Fed then mobilized the size and composition of its balance sheet to continue acting on financial conditions.

The theoretical justification mobilizes two concepts developed in the central-bank academic literature: the portfolio rebalancing channel and the signaling channel. The first posits that long-duration asset purchases by the central bank push investors to reallocate their portfolios toward higher-yielding assets, compressing term premia across the curve. The second posits that purchase announcements signal a durable commitment to accommodative policy. Federal Reserve Board staff research, notably published between 2011 and 2014, formalizes these channels in official discourse.

The doctrine over these six years remains marked by an explicit characterization: the balance sheet is an exceptional and temporary instrument. FOMC Statements of the period regularly mention the prospect of returning to “a balance sheet of normal size” once the crisis has passed. Chair Bernanke develops this doctrine in several speeches, notably the August 2010 Jackson Hole address that justifies QE2 as “reflation insurance”, and the March 2012 Northwestern speech formalizing the concept of credit easing distinct from classical QE.

The doctrinal grammar of regime 1 also developed a specific vocabulary that recurs across FOMC communication: “stimulating economic activity through lower long-term yields”, “fostering improved labor market conditions”, “supporting the housing market”. These verbal formulations were intentional. They positioned the balance sheet as instrumentally subordinate to traditional dual-mandate objectives, not as an autonomous monetary instrument. This rhetorical subordination was itself part of the regime’s doctrinal architecture. A complementary angle: our reading of systemic financial conditions.

QE3, announced in September 2012, introduces a major doctrinal innovation: open-ended purchases. For the first time, the Fed does not set a total amount a priori but calibrates purchase pace on labor-market conditions. This doctrinal mutation makes the balance sheet a “data-dependent” monetary policy tool, structurally different from earlier programs with pure quantitative targets. The doctrine of “qualitative forward guidance” on the balance sheet, distinct from forward guidance on the policy rate, emerges then. To grasp how composition by instrument reflects these doctrinal inflections, see balance-sheet composition across each doctrinal regime.

Regime 2 (2020-2022): the balance sheet as rapid-response weapon

The second regime’s doctrine is built in practice over three months, between March and June 2020. Facing the Covid shock, the Fed abandons regime 1’s “exceptional and temporary tool” framing and explicitly establishes the balance sheet as a systemic weapon for rapid mobilization. Chair Powell’s March-April 2020 speeches — notably the April 9, 2020 “Whatever it takes” address and the August 2020 Jackson Hole speech on the new Average Inflation Targeting framework — enact a deep doctrinal mutation. Further detail: the 2020 Covid shock.

Several features characterize this regime. First, speed of mobilization becomes an explicit criterion: the Fed doubles WALCL in three months, an unprecedented event in its institutional history. Second, the diversity of deployed assets and facilities far exceeds the Treasuries and MBS of regime 1: the Fed becomes temporarily a direct credit actor to the non-bank private sector via 13(3) facilities of the Federal Reserve Act. Third, coordination with the US Treasury via the CARES Act introduces a fiscal-monetary dimension into balance-sheet doctrine that prior regimes did not have. Related figures: Our WALCL series.

The revised Statement on Longer-Run Goals and Monetary Policy Strategy of August 2020 is the institutional expression of this mutation. The framework explicitly adopts a “broad-based and inclusive” maximum employment goal, modifying the Fed’s reaction function and indirectly justifying more active balance-sheet use in supporting monetary transmission. Regime 2 doctrine treats the balance sheet no longer as an exception but as a tool available at any time according to the cycle, without the prior presumption of returning to a pre-2008 baseline.

A subtle but important doctrinal shift accompanies regime 2: the abandonment of the language of “temporary” measures. The April 2020 FOMC Statement and subsequent communications speak instead of “supporting the smooth functioning of markets” and “promoting the flow of credit to households and businesses”. The verbal architecture shifts from time-bound exception to functional necessity. This linguistic mutation is part of what makes regime 2 distinct from a simple amplification of regime 1: it normalizes the idea of a permanently elevated Fed footprint.

Reading the three regimes as a mere intensification of the same instrument misses the doctrinal mutation that occurred. WALCL size has grown; but the function the Fed assigns to it within its toolkit has changed three times. Conflating quantitative evolution with conceptual evolution leads to overestimating doctrinal continuity and underestimating breaks.

Regime 3 (2022-2026): the balance sheet as permanent variable-dosage lever

The third regime’s doctrine is institutionalized through the Principles for Reducing the Size of the Balance Sheet published by the FOMC in May 2022. This document explicitly enacts two things: the Fed no longer aims at a return to a “normal-size balance sheet” pre-2008, but at a terminal size consistent with the ample reserves regime it formally adopted in January 2019; and the balance sheet becomes a variable-dosage tool, modulable according to cycle conditions rather than mobilized in a binary QE/QT regime.

The May 2024 cap modulation (-$95 billion to -$60 billion per month) is the doctrinal application of this principle: the Fed slows its QT not because it reverses course, but because it adjusts the dosage based on the gap between observed reserves and the targeted “ample” floor. This dosage logic is conceptually distinct from the binary QE/QT programs of prior periods.

An additional doctrinal feature of regime 3 is forward-looking transparency on the balance-sheet trajectory. The FOMC Minutes since 2022 explicitly document thresholds, conditions, monitored indicators. Chair Powell, in several speeches including May 2024, indicates that the end of runoff will be announced “well before” reserves reach a critical level. This anticipative communication contrasts with the abrupt end of QT1 in September 2019, which had been presented as a reactive response to repo tensions. For the practical implementation of this regime on the 2022-2026 runoff, see the current QT phase and projected endpoint.

Regime 3 doctrine does not resolve all open questions. The academic debate on the “right” terminal balance-sheet level remains active, and FOMC Minutes reflect internal divergences on landing pace. The official doctrine privileges a gradual approach grounded in empirical observation of repo-stress indicators, which itself constitutes a break from regime 1’s confidence in the structural stability of the pre-2008 baseline. Monetary transmission and system plumbing are now explicit doctrinal constraints, not residuals to manage in emergency.

Historical analysis of the three regimes finally illuminates a prospective question: what will the balance-sheet doctrine be in a potential regime 4? If the Fed is recalled to emergency by a new systemic crisis, will it again mobilize the balance sheet in regime 2 logic (rapid response), or will it have sufficiently institutionalized regime 3 (variable dosage) to handle the crisis without doctrinal break? The answer is not determined by operational tools alone: it will depend on the function the Fed assigns to the balance sheet in the Statements of the coming crisis. The 70-year track record of Fed Funds decisions documents historical precedents useful for anticipating this question.

Internal FOMC doctrinal tensions deserve a final note. The Minutes from the 2022-2025 period reveal recurrent divergences among members on the appropriate runoff pace, the targeted reserves floor, and the trade-off between QT duration and market-stress risks. These tensions are not anecdotal: they reflect that regime 3 doctrine, even institutionalized, has not resolved all conceptual trade-offs. The conception of the balance sheet as a permanent variable-dosage lever is shared, but the concrete calibration of the dosage remains an object of internal debate.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…