Why Central Banks Make Recurring Policy Errors

Central banks are not omniscient. Lagged data, model dependence and the inflation/unemployment asymmetry produce recurring errors that often only become visible after the cycle has turned.

This tag analyses central bank communication and its impact on market expectations. Forward guidance — signalling the future path of rates — has become a monetary policy tool in its own right. It also covers the gaps between what markets anticipate and what central banks deliver. These surprises often generate significant market moves.

Central banks are not omniscient. Lagged data, model dependence and the inflation/unemployment asymmetry produce recurring errors that often only become visible after the cycle has turned.

Monetary policy acts in large part through the expectations it generates. Decisions and communications from central banks reshape financial conditions before policy rates move or economic effects become visible. TL;DR Central-bank communication now reshapes financial conditions before any rate moves,…

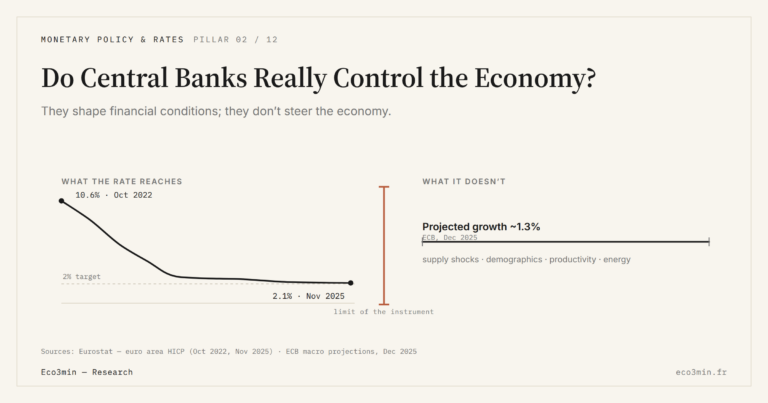

Central bank action influences the economy but remains constrained by private behavior and financial structure. The 2022-2025 ECB cycle illustrates both the reach and the limits of the rate instrument.

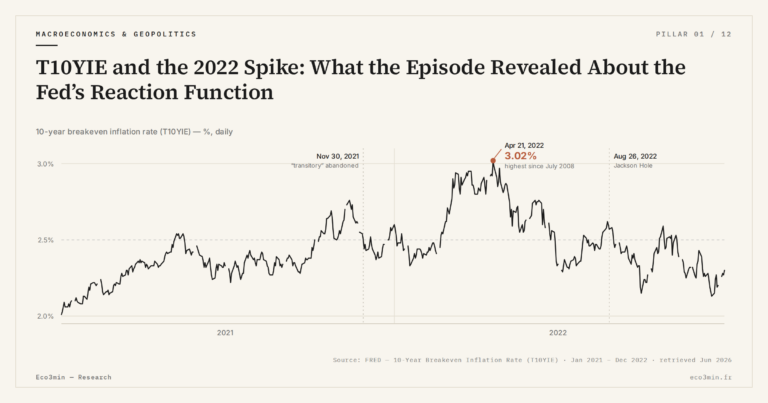

On April 21, 2022, T10YIE hit 2.99% — the highest level since July 2008. The episode constitutes the live-fire test of the Fed’s reaction function and remains, four years later, the implicit reference for every breakeven reading. TL;DR The 2022…

T10YIE has become the reference measure of long-term market-implied inflation expectations. Yet it is the regime reading, not the absolute level, that makes it the central indicator for understanding current Federal Reserve policy. TL;DR Averaging 2.11% from 2003 to 2025…