T10YIE and the 2022 Spike: What the Episode Revealed About the Fed’s Reaction Function

On April 21, 2022, T10YIE hit 2.99% — the highest level since July 2008. The episode constitutes the live-fire test of the Fed’s reaction function and remains, four years later, the implicit reference for every breakeven reading.

TL;DR

The 2022 breakeven spike reads as a regime-validation event: T10YIE topped at 2.99% and retraced rather than breaking toward the 4-5% de-anchoring zone.

- The drift followed Powell's November 30, 2021 Senate pivot away from 'transitory'; the 2.99% peak on April 21, 2022 was the highest since July 2008, just before Lehman.

- The New York Fed's decomposition showed only about one third of the simultaneous DGS10 rise came from the breakeven and two thirds from the real yield, so anti-inflation credibility stayed largely intact.

- The Fed answered with three qualitatively new moves: a first 75bp hike on June 15, 2022, Powell's 'until the job is done' Jackson Hole speech on August 26, and four straight 75bp hikes taking Fed funds from 1.00% to 4.00% in six months; the 2.5% tolerance threshold was crossed back down by mid-August.

This article traces the full chronology of the spike: 2021 context, January-April 2022 run-up, Fed response, return to anchoring. For the structural reading, see T10YIE as the 10-year expectations indicator.

1. The pre-spike context: 2021, the “transitory abandoned” pivot

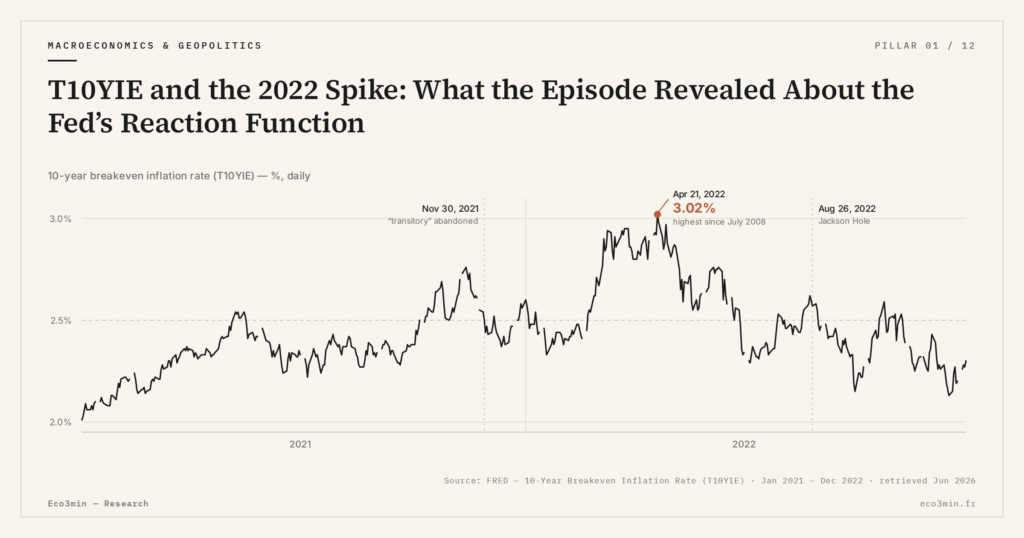

To understand the April 2022 spike, one must go back to 2021. By that time, US CPI inflation was accelerating progressively from the pandemic trough: 4.2% trailing in April 2021, 5.4% in June, 6.2% in October, 7.0% in December according to the Bureau of Labor Statistics. The Federal Reserve maintained throughout 2021 a public qualification of pressures as “transitory,” inherited from the July 2021 FOMC statement and several Powell interventions between summer and fall. During this period, T10YIE oscillated between 2.30% and 2.55%, slightly above the 2% target but without marked drift.

On November 30, 2021, Jerome Powell publicly abandoned the “transitory” qualification during testimony before the Senate. This was a major rhetorical pivot: the Fed officially recognized that inflation pressures were more persistent than anticipated and that tightening would have to occur. At that moment, T10YIE was at 2.55%. The market reaction was immediate: in the following weeks, the breakeven rose progressively to 2.70%, then 2.80% in March 2022, signaling that markets were embedding a more durable expectations drift risk.

Several external factors amplified the move. The post-2020 inflation cycle combined with specific shocks: the war in Ukraine launched on February 24, 2022 sent European energy prices surging and triggered a global confidence shock; post-COVID supply chains remained disrupted with persistent bottlenecks. The context therefore combined a monetary policy perceived as late and an accumulation of real shocks.

The first Fed funds hike — modest, 25 basis points — came on March 16, 2022, five months after the rhetorical pivot. At that date, T10YIE was at 2.87%. The 25-point hike was perceived as insufficient by markets given CPI inflation reaching 7.9% trailing in February 2022. This perception fueled the breakeven drift in the following weeks — it is in this window that the actual spike unfolded.

2. The spike sequence: January-April 2022

The precise chronological sequence is instructive. In early January 2022, T10YIE was trading around 2.55%. By end-January, the breakeven had already gained 5 basis points to reach 2.60%. In February, the war in Ukraine caused a 25-basis-point jump over two weeks, propelling T10YIE to 2.85%. By mid-March, after the first Fed hike judged timid, the breakeven sat at 2.92%. The final push came on April 18-21, 2022: T10YIE crossed 2.99% on April 21, its highest level since July 28, 2008 — that is, before the Lehman Brothers bankruptcy.

The amplitude of the move deserves qualification. Over 3.5 months (January-April 2022), T10YIE gained 44 basis points. This is, in the modern history of the series, the fastest move recorded without involving a violent deflationary shock. Compared to the partial de-anchorings of the late 1970s — where 10-year expectations retrospectively estimated by the Cleveland Fed had exceeded 8% on multiple occasions — the 2022 spike remained very contained in absolute terms, but it constituted the live-fire test of the modern Fed reaction function in its inflation-targeting regime.

An important empirical dimension: the composition of the DGS10 rise during the same period was decomposed by the Federal Reserve Bank of New York in August 2022. On the nominal Treasury spike from 1.63% in January to 2.93% on April 21, 2022 (+130bp), only 44 basis points came from T10YIE — roughly one third. The majority of the nominal move was carried by the rise in DFII10 (expected real yield), not by expectations. For the technical detail of this analysis, see decomposing the 2022 DGS10 surge.

This 1/3 expectations – 2/3 real split is paradoxical at first glance: why did the Fed worry if the majority of the move came from expected real yields, that is, from tightening being correctly transmitted? The answer lies in the dynamics: what worried the Fed was not the level reached at 2.99%, but the speed of ascent and the risk that the breakeven would cross 3% and then 3.5%, the level beyond which the self-fulfilling mechanics of expectations become hard to reverse.

3. The Fed response: June 2022, Jackson Hole, hike sequence

The Fed response to the spike unfolded in three distinct but coordinated elements. The first is the first 75-basis-point hike on June 15, 2022 — an explicit break with the usual pattern of 25- or 50-basis-point hikes. This hike was decided when T10YIE had already retreated to 2.73% on June 14, that is 26 basis points below the April peak. The timing suggests the Fed was acting less on the current level than on the residual risk of resurgence.

The second element is Jerome Powell’s speech at Jackson Hole on August 26, 2022. Powell explicitly invoked a “painful” cost of disinflation and indicated that the Fed would tighten “until the job is done.” This communication marked a public tone shift: the Fed recognized that bringing expectations back under control would likely require a significant economic slowdown, and that it accepted this. Markets interpreted the speech as a multi-quarter commitment to maintain restrictive policy, regardless of short-term macro data. At the August 26 close, T10YIE was at 2.57%, that is 42 basis points below the April peak.

The third element is the sequence of four consecutive 75-basis-point hikes between June and November 2022. This pace — unprecedented in modern FOMC history — lifted the Fed funds rate from 1.00% to 4.00% in six months, equivalent to three years of classical tightening condensed. This acceleration was calibrated to demonstrate Fed determination and prevent any retest of the 3% zone by T10YIE. For the underlying theoretical framework, see the Fed reaction function triggered by expectations.

4. The return to anchoring and lessons of the episode

The return to T10YIE anchoring followed a measurable trajectory. After the April 21, 2022 peak, the breakeven retraced: 2.73% end-June, 2.57% at Jackson Hole, 2.40% end-August, 2.28% end-October, 2.21% end-December 2022. The 2.5% threshold — implicit Fed tolerance boundary — was crossed downward in mid-August 2022, four months after the peak. At that point, the Fed considered the emergency phase over and the remainder of tightening could be calibrated at the classical pace of 25-50 basis points per meeting.

The general lesson of the episode rests on three points. First: a 10-year breakeven can drift well before realized inflation poses a durable problem, because it embeds a 10-year projection that depends on Fed credibility, not on the current monthly CPI print. The Fed must therefore react on the breakeven even when realized CPI is temporarily contained. Second: the return to anchoring is faster than the drift, provided the Fed takes qualitatively new actions — the shift to 75 basis points per meeting being the paradigmatic example. Third: the breakeven does not mechanically revert to the 2.1% historical mean, but to an equilibrium level that depends on residual post-cycle expectations. For the reading of the post-episode regime, see return to anchoring and 2023-2026 stabilization.

A counterintuitive observation closes the episode: the mere fact that T10YIE topped at 2.99% rather than 4% or 5% constitutes, in central-banking history, a monetary policy success. A 44-basis-point move over 3.5 months is a test, not a failure. The comparison with the 1970s episodes — where 10-year expectations exceeded 8% — shows the magnitude of progress in central-bank credibility since inflation targeting. The 2022 episode should be read as a demonstration that the modern regime works, not as a warning that it fails. This finding is put in perspective by the structural drivers behind inflation.

One final dimension is worth flagging for the analyst: subsequent academic work — notably papers presented at the 2023 and 2024 Jackson Hole symposia — has converged on reading the 2022 spike as a regime-validation event rather than a regime-failure event. Federal Reserve Board research notes published in 2024 explicitly cite the episode as evidence that the inflation-targeting framework, combined with credible communication and willingness to accept a tightening cost, can contain even substantial inflation shocks without crossing into the de-anchoring zone. This academic consensus matters because it shapes how future episodes will be framed by the Fed in its own communication and how markets will calibrate their expectations of Fed reaction speed.

- The T10YIE peak at 2.99% on April 21, 2022 is the highest since July 2008. The 44-basis-point drift over 3.5 months followed Powell’s November 30, 2021 pivot abandoning the “transitory” qualification of post-COVID inflation.

- The DGS10 rise over the same period was decomposed by the NY Fed: only one third came from the breakeven (expectations), two thirds from the real yield (transmitted Fed tightening). Anti-inflation credibility remained largely intact.

- The Fed response unfolded in three stages: first 75bp hike on June 15, 2022 (pattern break), Powell’s August 26 Jackson Hole speech, sequence of four consecutive 75bp hikes lifting Fed funds from 1.00% to 4.00% in six months.

- The implicit 2.5% Fed tolerance threshold was crossed downward in mid-August 2022, four months after the peak. Return to anchoring is faster than the drift when the Fed acts with qualitatively new tools.

Last updated — 21 June 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…