Do Central Banks Really Control the Economy?

Central bank action influences the economy but remains constrained by private behavior and financial structure. The 2022-2025 ECB cycle illustrates both the reach and the limits of the rate instrument.

Central bank action influences the economy but remains constrained by private behavior and financial structure.

TL;DR

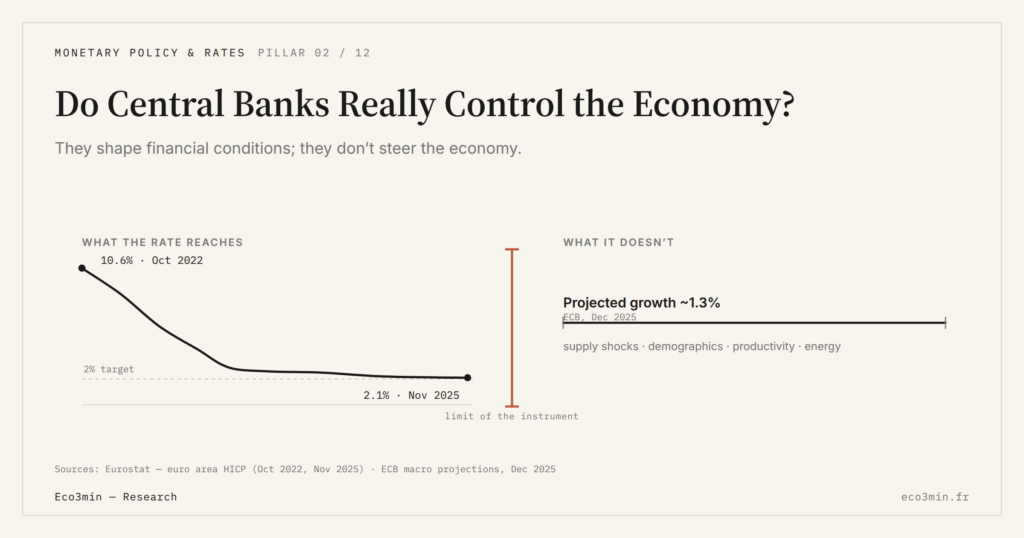

The ECB's 450bp tightening pulled euro-area inflation from 10.6% (Oct 2022) to ~2.4% by late 2025, yet potential growth stayed near 1.3%: monetary policy steers financing conditions, not structural growth.

- The 2022–2025 tightening worked, but with side effects: contracting mortgage credit, slower productive investment, and strain on public finances.

- Rates cannot fix structural imbalances — competitiveness gaps, underinvestment, demographics, energy dependence — nor primary supply shocks; the 2021–22 surge came largely from supply-chain disruption and the energy spike.

- Credibility amplifies policy: when agents trust the inflation target they self-adjust (wage moderation, anchored expectations); lost credibility forces sharper action and lengthens transmission.

Central banks are often perceived as all-powerful pilots of the economy. This view overstates their capacity for action in a decentralized system. Monetary decisions modify financial conditions but do not determine private choices or productive structure. Examining these limits helps place monetary policy at its proper scale. For a concrete application to savings and investment decisions, see the impact of policy rates on household wealth.

The objection is familiar: if central banks “control” the economy, why didn’t they prevent the 2022 inflation surge, the 2008 crisis, or Japan’s 1990s stagnation? The reasoning is spelled out in this question on central banks gold accumulation. The answer lies in a confusion between influence and control. Monetary policy acts on the conditions under which agents make their decisions — it does not make those decisions for them. Further on this: a central bank capping long rates.

What Monetary Policy Can Actually Achieve

Central banks have a powerful but indirect lever: the cost and availability of money. By setting the policy rate, they influence the price of bank refinancing, which then transmits to lending rates, bond yields and asset valuations. The multiplicity of channels through which this influence propagates explains both its reach and its limits.

Over the 2022-2025 period, the ECB demonstrated that sufficiently determined tightening eventually slows demand and bends the price trajectory. Euro area inflation moved from a 10.6% peak in October 2022 to around 2.4% by late 2025 (Eurostat data). But this result required a cumulative 450 basis point hike over fourteen months, followed by an extended hold — and was accompanied by unintended side effects: contraction in mortgage credit, slower productive investment, strain on public finances.

Areas Beyond the Reach of the Monetary Instrument

Monetary policy cannot correct structural imbalances. A competitiveness gap, chronic underinvestment in infrastructure, unfavorable demographics, or excessive energy dependence all escape the rate instrument. These factors determine long-run potential growth, which monetary policy can only accompany or temporarily slow. Worth reading alongside: our account of how higher rates compress margins over time.

It also does not control supply shocks. The 2021-2022 inflation surge largely came from supply chain disruptions and the energy price spike — phenomena over which interest rates have no direct grip. The ECB tightened to contain second-round effects, but could not act on the primary causes of inflation.

The impression that monetary decisions remain ineffective in the short run partly stems from this confusion: monetary policy is expected to solve problems that fall outside its scope. According to the ECB’s macroeconomic projections (December 2025), euro area potential growth was estimated at ≈1.3% — a figure reflecting structural constraints on which the policy rate has no influence.

Attributing to central banks responsibility for outcomes that depend on factors beyond their reach. Monetary policy does not autonomously create growth or employment. It modifies the financing conditions under which private and public decisions are made. Assigning it direct control over the economy misreads the nature of its instrument.

The Paradox: The More They Are Trusted, the More Effective They Become

Central bank effectiveness rests partly on the credibility of their commitment. If economic agents believe the institution will return inflation to its target, they spontaneously adjust their behavior — wage moderation, stable price expectations, calibrated investment decisions. This self-fulfilling dimension is fundamental: credibility amplifies the effect of monetary policy without requiring additional action.

Conversely, a loss of credibility forces the central bank to act more sharply to obtain the same result. The propagation time of monetary decisions through the real economy lengthens when expectations are unanchored, because agents factor in doubt about the future trajectory. The institutional and communication framework of monetary authorities aims precisely to preserve this credibility — an intangible but decisive resource.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…

Inverted Yield Curve: Reading a Regime Signal Without Immediate Effect

The inverted yield curve operates as a regime signal, not a timing tool. Its lagged effects are constitutive…