US Inflation Breakeven Term Structure: The 5Y/10Y Curve, 2003–2026

Between 2010 and 2019, the 10-year inflation breakeven exceeded the 5-year breakeven in every single one of 120 months. Since April 2021, that configuration has reversed in 45 of 61 months — a persistence of inverted term structure with no precedent in the FRED breakeven series.

— Eco3min Research")

For two decades, US Treasury breakevens told a single story about inflation expectations: longer-dated paper consistently priced higher inflation than shorter-dated paper. Since 2021 that story has inverted, and stayed inverted. This page provides the complete monthly dataset and the empirical record of what changed.

The US Treasury breakeven inflation rate is the spread between a nominal Treasury yield and the yield of a Treasury Inflation-Protected Security (TIPS) of the same maturity, published daily and monthly by the Federal Reserve Bank of St. Louis as series T5YIE and T10YIE. This dataset documents the 5-year and 10-year breakeven rates from January 2003 through April 2026 — 280 monthly observations — together with the spread between them, regime classifications, and a comparison of breakeven values against subsequent realized CPI inflation. The data shows that the term structure direction of US breakevens has reversed since 2021 and stayed reversed, while the median breakeven level has remained close to the 2% Federal Reserve target. the Eco3min framework for TIPS and inflation linkers traces this mechanism across cycles.

From January 2010 to December 2019, the 10-year breakeven exceeded the 5-year breakeven in 120 of 120 months. Since April 2021, that ordering has reversed in 45 of 61 months (74%), with a peak inversion of +0.56 percentage points in March 2022. The median 5-year breakeven across the full sample remains 2.00%, close to the Federal Reserve’s stated target. Note: this dataset measures the market price of inflation insurance, not consumer or survey-based inflation expectations directly (see Methodology).

5-year breakeven (T5YIE)

10-year breakeven (T10YIE)

Spread (5Y − 10Y) — reversed

Months since Apr 2021 in Post-COVID phase

- The term structure has flipped. The 10-year breakeven exceeded the 5-year breakeven in 120 of 120 months between January 2010 and December 2019. Since April 2021, that ordering has reversed in 45 of 61 months — a persistence of inversion that did not occur during the Recovery/QE phase (0 of 80 months) or during the Liftoff cycle (0 of 51 months).

- The peak inversion was +0.56 percentage points in March 2022, with T5YIE at 3.41% (the highest single monthly value in the FRED T5YIE series since its inception in 2003) against T10YIE at 2.85%. Subsequent months have shown the spread compress toward zero without flipping back to the prior configuration: the mean post-COVID spread is +0.10pp, against −0.26pp during 2010–2019.

- The median anchor has not moved. Across the full 280-observation sample, the median 5-year breakeven is 2.00% and the median 10-year breakeven is 2.23% — both within the band typically described as “well-anchored” by Federal Reserve communications.

- Breakevens systematically underestimated realized inflation in 2020. The 5-year breakeven in March-May 2020 averaged approximately 0.73%; the realized annualized CPI growth over the following five years averaged 4.5% — a forecasting miss of roughly 3.8 percentage points annualized, the largest in the FRED T5YIE series. The systematic gap between priced breakevens and subsequent realized CPI is analysed in our study of the divergence between 10-year expectations and realized inflation.

- The Pre-GFC era was occasionally inverted. In 2003–2008, the 5-year exceeded the 10-year in 24 of 68 months (35%) — short-lived flips driven by oil-price episodes. The current regime is distinguished from those earlier inversions not by its existence but by its persistence: no prior 5-year window contains anything close to a 74% inversion frequency.

- Dataset specifications. 280 monthly observations spanning 23 years; 11 derived columns including spread sign, regime classification (±10bp threshold), GFC dysfunction flag, phase taxonomy (7 phases), forward CPI realization, and breakeven prediction error. Published under CC BY 4.0.

280 monthly observations · Jan 2003 – Apr 2026 · CC BY 4.0 ·

Methodology ·

Cite this dataset

Monthly observations

Months 2010–2019 with T10YIE > T5YIE

Post-COVID months with T5YIE > T10YIE

Maximum inversion (March 2022)

Median 5-year breakeven, full sample

Current spread (April 2026)

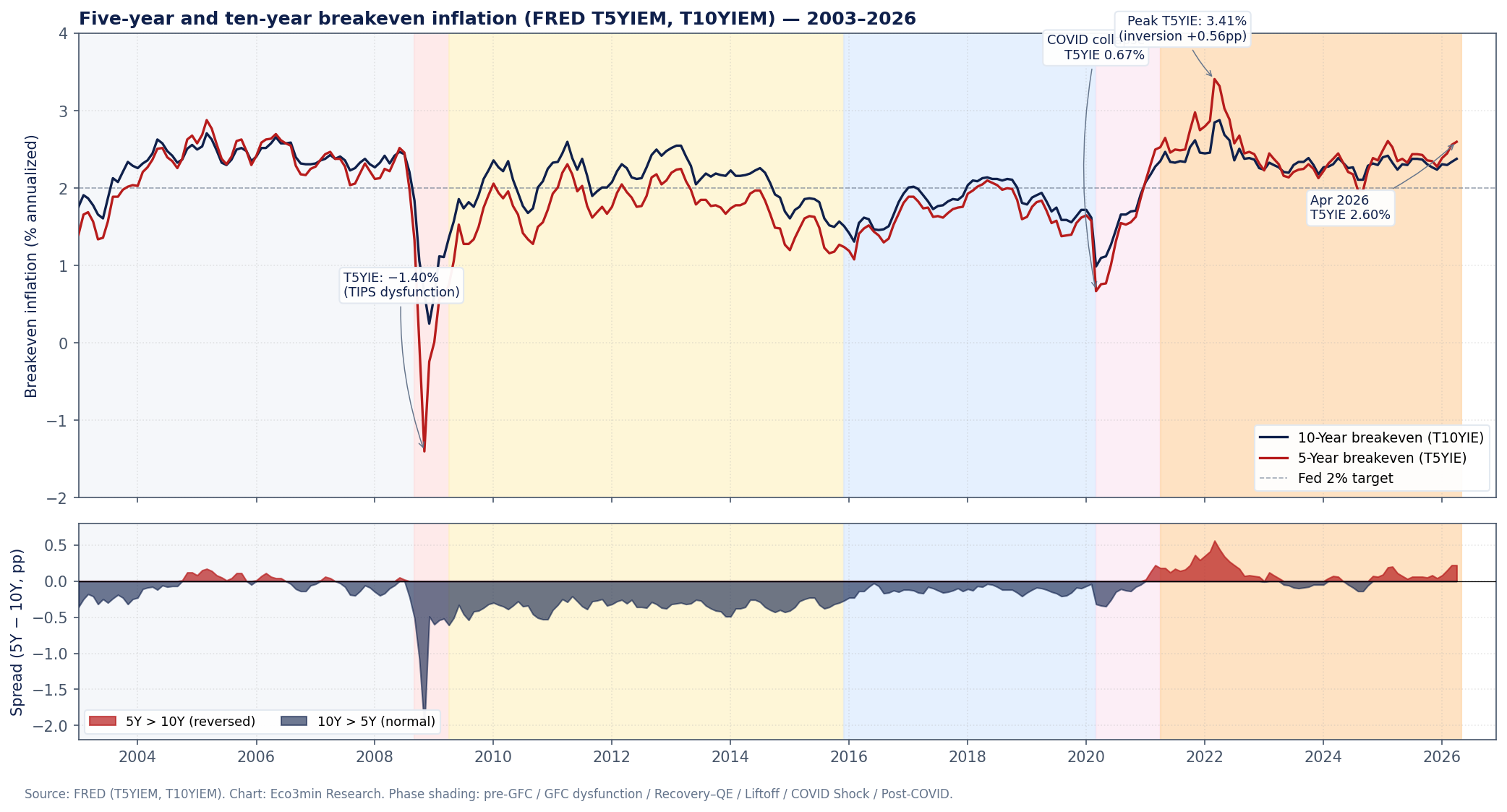

Chart: Five-Year and Ten-Year Breakeven Inflation, 2003–2026

US Treasury breakeven inflation: 5-year and 10-year, monthly 2003–2026

The two breakeven series tracked each other within roughly 50 basis points for two decades. Since 2021, the 5-year has moved decisively above the 10-year and has stayed there.

The spread band in the lower panel is almost entirely below zero from 2010 to early 2021, then mostly above zero from April 2021 onwards. The November 2008 negative outlier (−2.04pp) reflects TIPS market liquidity dysfunction during the Lehman aftermath, not a regime-comparable observation.

Sources: Federal Reserve Bank of St. Louis (T5YIEM, T10YIEM). Chart: Eco3min Research.

{kind=link}

How to Read This Chart

The upper panel plots the 5-year (red) and 10-year (navy) breakeven inflation rates as reported by FRED, monthly closing values. The horizontal dashed line marks the 2% target the Federal Reserve formally adopted in January 2012. Background shading divides the sample into six analytical phases: Pre-GFC (2003-01 to 2008-08), GFC Dysfunction (2008-09 to 2009-03, a brief episode of TIPS market illiquidity discussed below), Recovery/QE (2009-04 to 2015-11), Liftoff (2015-12 to 2020-02), COVID Shock (2020-03 to 2021-03), and Post-COVID (2021-04 onwards).

The lower panel plots the spread between the two — T5YIE minus T10YIE. When the spread is below zero (navy fill), the term structure is in its conventional configuration: investors price more inflation in the distant future than in the near future. When the spread is above zero (red fill), the configuration has reversed: near-term inflation is priced higher than long-term inflation. The visual pattern is the page’s central empirical finding. For methodology, including the regime classification thresholds and the treatment of the GFC dysfunction window, see the Methodology section.

The Decade Without an Inversion

The standard description of US inflation expectations in the 2010s, repeated across central bank communications and market commentary, runs something like this: long-term expectations remained anchored near 2%, while short-term expectations responded to oil-price shocks, occasional growth surprises, and the gradual recovery from the financial crisis. In this telling, the breakeven curve is upward-sloping in the long run because investors demand compensation for inflation risk over longer horizons, and that risk premium translates into a higher 10-year breakeven than 5-year breakeven.

The data confirms the upward slope for the full decade following the GFC dysfunction. From January 2010 through December 2019, the 10-year breakeven exceeded the 5-year breakeven in every single one of 120 monthly observations. The mean spread (T5YIE minus T10YIE) was −0.26 percentage points; the median was −0.27pp. Not a single month flipped. Extending the window to include the immediate post-dysfunction recovery (from April 2009) and the pre-COVID Liftoff cycle through February 2020 yields the same result: 129 of 129 months with T10YIE above T5YIE.

Since April 2021, the configuration has reversed. The 5-year has exceeded the 10-year in 45 of 61 months — a frequency of 73.8% — with an additional one month at zero. The peak inversion of +0.56pp was reached in March 2022, the same month T5YIE itself peaked at 3.41% (the highest single monthly value in the FRED T5YIE series since its inception in January 2003). The mean spread across the Post-COVID phase is +0.10pp, compared to −0.26pp during 2010–2019: a differential of 0.35pp.

The TIPS market matured during the sample. The 5-year TIPS series was first issued in 1997 and the breakeven indicator gained robustness as the market deepened in the early 2000s. The Federal Reserve formally adopted the 2% inflation target in January 2012. Direct comparison across the full 23-year sample accounts for this institutional evolution, though the core observation — the absence of any inversion in 2010–2019 — is robust to start-date variation (see Methodology sensitivity).

What this dataset does not measure. Treasury breakevens are the market price of trading nominal Treasuries against TIPS of the same maturity. They contain three components: (i) the average expected inflation rate over the relevant horizon, (ii) an inflation risk premium investors demand for bearing inflation uncertainty, and (iii) a liquidity premium reflecting the relative depth of TIPS versus nominal Treasury markets. Decomposing breakevens into these three components requires modelling assumptions — the New York Fed’s ACM (Adrian, Crump, Moench) model is one widely cited approach. Breakevens are not a direct measure of consumer or survey-based inflation expectations. Comparable consumer and survey-based series include the University of Michigan inflation expectations (MICH on FRED, 1-year and 5-10-year horizons), the New York Fed Survey of Consumer Expectations (SCE, 1-year and 3-year horizons, available from 2013), and the Survey of Professional Forecasters published by the Philadelphia Fed.

The empirical record contains a clean break: 129 consecutive months without an inversion (April 2009 to February 2020), followed by 61 months with 74% inversion frequency (April 2021 onwards). The break is detectable by simple count, without modelling.

What Each Phase Looked Like

The Phase classification used throughout this page partitions the sample into six analytical windows defined by monetary policy, market structure, and macro regime. The frequency of term-structure reversal varies sharply across phases, providing a comparative reference for the post-2021 configuration.

Phase-by-Phase Term Structure Direction

| Phase | Window | n (months) | Mean spread (5Y−10Y) | % months inverted (5Y > 10Y) | Mean T5YIE |

|---|---|---|---|---|---|

| Pre-GFC | 2003-01 → 2008-08 | 68 | −0.07pp | 35.3% | 2.28% |

| GFC Dysfunction | 2008-09 → 2009-03 | 7 | −0.83pp | 0.0% | 0.12% |

| Recovery/QE | 2009-04 → 2015-11 | 80 | −0.35pp | 0.0% | 1.73% |

| Liftoff | 2015-12 → 2020-02 | 51 | −0.13pp | 0.0% | 1.67% |

| COVID Shock | 2020-03 → 2021-03 | 13 | −0.12pp | 23.1% | 1.51% |

| Post-COVID | 2021-04 → 2026-04 | 61 | +0.10pp | 73.8% | 2.46% |

Three observations stand out. First, the Pre-GFC phase shows that breakeven term structure inversion is not a new phenomenon: 24 of 68 months saw the 5-year exceed the 10-year, typically during brief oil-price episodes. What is new is the persistence — no prior 5-year window contains anything resembling a 74% inversion frequency. Second, the Recovery/QE and Liftoff phases are striking in their uniformity: across 131 combined months from April 2009 to February 2020, the 5-year never once exceeded the 10-year. Third, the GFC Dysfunction window is a separate analytical category — the −0.83pp mean spread reflects the collapse of T5YIE to −1.40% in November 2008, an episode that mechanically dominates volatility and distributional statistics if not isolated.

Volatility by Phase

Beyond the direction of the curve, the volatility of breakevens also varies across phases. Annualized 12-month rolling standard deviation of monthly changes provides a comparable measure across periods.

| Phase | n (obs with vol) | Mean vol — 5Y breakeven | Mean vol — 10Y breakeven | 5Y / 10Y ratio |

|---|---|---|---|---|

| Pre-GFC | 56 | 0.43 | 0.31 | 1.36× |

| GFC Dysfunction | 7 | 2.04 | 0.97 | 2.11× |

| Recovery/QE | 80 | 0.65 | 0.49 | 1.34× |

| Liftoff | 51 | 0.35 | 0.29 | 1.22× |

| COVID Shock | 13 | 1.00 | 0.71 | 1.42× |

| Post-COVID | 61 | 0.49 | 0.34 | 1.43× |

Across every phase except the GFC Dysfunction window, the 5-year breakeven is between 1.2 and 1.4 times as volatile as the 10-year. This is the structural reason why temporary shocks tend to widen the spread visibly: the shorter-dated series moves more on the same news. In the Post-COVID phase, the absolute level of 5-year volatility (0.49) is similar to the Recovery/QE phase (0.65) and roughly half the COVID Shock level (1.00), so the inversion is not driven by elevated turbulence — the curve has tilted, not destabilized. For broader context on inflation dynamics across these phases, see our complete CPI inflation history study and the consumer sentiment dataset.

A Legitimate Reading: Anchor Plus Path

A reading of the post-2021 configuration that does not require any departure from standard inflation-targeting theory runs as follows. Markets observed a large near-term inflation shock starting in 2021, reflecting energy prices, supply-chain disruption, and demand patterns from pandemic-era fiscal transfers. Five-year inflation pricing rose accordingly, because the next 5 years contain that shock. Ten-year inflation pricing rose by less, because averaging the shock over a longer window dilutes its effect. The result is a temporary inversion of the term structure that resolves slowly as the shock period rolls out of the 5-year window.

This interpretation has three things going for it. First, the median 10-year breakeven across the Post-COVID phase is 2.33% — approximately 33 basis points above the Fed’s 2% target, which is within the band typically described as anchored in central bank communications, and substantially below the peak of 2.85% reached in March 2022. Second, the spread has been compressing: from +0.56pp in March 2022 down to +0.22pp in April 2026. The configuration is moving toward, not further from, its prior state. Third, this exact mechanism — front-loaded near-term inflation pricing combined with a stable long-run anchor — is the outcome an inflation-targeting regime is supposed to produce in response to a transitory shock. Volcker, had he observed it in 1980, would have considered it evidence that monetary policy was working.

The empirical record does not falsify this reading. What it does, however, is establish the persistence of the configuration as unusual. The post-COVID inversion has now lasted longer than any documented inflation shock period in the FRED breakeven sample. A shock that takes 5+ years to roll out of a 5-year window is, by construction, no longer a short-run phenomenon. Whether this matters for monetary policy or merely reflects path uncertainty is a question the breakeven data alone cannot answer; it would require triangulation against survey-based long-term expectations dispersion, professional forecaster forecasts, and direct measures of inflation uncertainty (for example, the NY Fed’s SCE measures of forecast dispersion).

The data establishes that the term structure has reversed and stayed reversed. It does not establish — and breakevens alone cannot establish — whether this reflects unmoored expectations or a slowly rolling near-term shock interacting with a stable long-run anchor.

What Happened Next? Realized Inflation by Breakeven Regime

Standard forward-return tables on Eco3min compare a market signal at observation date to subsequent equity returns. For breakeven inflation, the more direct comparison is to the realized inflation that subsequently occurred. The table below classifies each observation by the term-structure regime at that date and reports the median realized annualized CPI growth over the following 5 years. The sample excludes the seven months of GFC dysfunction (September 2008 – March 2009) and includes only observations through January 2021, the last date for which a complete 5-year forward window of CPI data is available.

| Regime (spread_5_10 at obs date) | n | Median T5YIE | Median realized 5Y CPI | Median forecast error (T5YIE − realized) | % over-estimations |

|---|---|---|---|---|---|

| 5Y > 10Y, reversed (>+10bp) | 8 | 2.66% | 2.37% | +0.41pp | 100.0% |

| Flat (±10bp) | 55 | 2.30% | 2.34% | −0.02pp | 47.3% |

| 10Y > 5Y, normal (>+10bp) | 146 | 1.76% | 1.83% | −0.28pp | 41.8% |

When the term structure was in its conventional configuration (10Y > 5Y), the 5-year breakeven understated subsequent CPI growth by a median of 0.28 percentage points. When the structure was reversed (5Y > 10Y), the 5-year breakeven overstated subsequent CPI growth by a median of 0.41 percentage points. The forward-window data ends in January 2021; the most recent post-2022 inversion period has no completed 5-year window yet.

Methodological note: the regime classification at observation date uses a ±10 basis point threshold around zero spread, identifying “Flat” observations where the two breakevens are functionally tied. The 5-year forward CPI growth is computed as the geometric annualized rate: (CPI[t+60mo] / CPI[t])^(1/5) − 1. Sample size for the reversed regime (n=8 with available forward window) is modest; these observations are concentrated in the brief Pre-GFC episodes (e.g. 2005, when oil prices were rising).

Past distributions are not predictive of future outcomes. Regime-conditional statistics describe historical patterns, not expected returns or expected inflation.

- ▸ Spread sign (5Y − 10Y), currently +0.22pp: a sustained move below zero, defined as the trailing 6-month average crossing below −0.10pp, would mark a return to the pre-2021 configuration. The trailing 6-month average has stayed continuously above zero since February 2025 (15 consecutive months); the cumulative count of months with positive spread since April 2021 is 45 of 61.

- ▸ T5YIE level, currently 2.60%: the median 5-year breakeven across the full sample is 2.00%. Sustained moves above 3.00% have occurred only once in the entire FRED T5YIE series — three consecutive months from March to May 2022, peaking at 3.41%. See our CPI inflation history dataset for context on realized inflation.

- ▸ Next FRED T5YIE release: daily FRED updates are typically posted by 4:15 PM Eastern with one business day lag. Monthly T5YIEM is updated at the start of each month based on the average of daily values for the prior month.

Regime Classification: Twenty-Three Years of Term Structure Direction

Five-year minus ten-year breakeven spread, by month (2003–2026)

Two decades of normal upward curvature visible as cool blue cells; the 2021–2026 reversal visible as warm orange cells. The clean break is the page’s central empirical finding.

Note: November 2008 cell (−2.04pp) reflects TIPS market liquidity dysfunction; color scale capped at ±0.7pp for readability. Sources: FRED (T5YIEM, T10YIEM). Chart: Eco3min Research.

{kind=link}

Regime Interpretation Grid

Spread < −0.10pp. T10YIE exceeds T5YIE by more than 10 basis points. The configuration most commonly associated with stable inflation regimes; comprises all of 2010–2019 and most of the Recovery/QE phase.

Absolute spread ≤ 0.10pp. The two breakevens within a 10 basis point band; effectively tied. Common during inflection periods such as 2003 (TIPS series infancy), 2004 (transition), and intermittent 2016–2018 patches.

Spread > +0.10pp. T5YIE exceeds T10YIE by more than 10 basis points. Pre-2022 occurrences (19 months) were brief and concentrated around oil-price episodes (2005, 2021). The post-2022 cluster (15 months) is the longest sustained reversal in the series under this threshold; broadening to include all Post-COVID-phase reversed months brings the count to 24.

September 2008 – March 2009. T5YIE collapsed to −1.40% in November 2008 due to TIPS market illiquidity, not inflation expectations. Treated as a separate analytical category; excluded from headline regime statistics and forecast-error analysis.

Did Breakevens Predict Realized Inflation?

5-year breakeven (T5YIE) at observation date vs realized annualized CPI growth over next 5 years

Points above the 45° line indicate the breakeven underestimated subsequent realized inflation. The COVID-era cluster sits high above the line: breakeven priced near-zero, inflation came at 4.4-4.6% annualized.

Source: FRED (T5YIEM, CPIAUCSL). Chart: Eco3min Research.

The chart provides a direct test of whether breakevens have been informative about future realized inflation. For each observation date from January 2003 through January 2021 (the last date where a complete 5-year forward window is available), the 5-year breakeven is plotted against the geometric annualized CPI growth that subsequently occurred. The 45° line represents perfect prediction. The dispersion around the line is large but not random: COVID-era breakevens (priced in early 2020 at 0.7-1.0%) sit roughly 3.8 percentage points below what subsequently realized; pre-GFC observations from mid-2008 (priced around 2.5%) sit somewhat above realization because the GFC suppressed inflation in 2009-2010.

Two implications follow. First, the largest single forecasting failure in the FRED breakeven series is the COVID-era cluster — not the post-2022 inversion. At the moment when long-term anchoring was most visibly preserved (breakevens crashed to 0.7%), the subsequent realized inflation diverged from breakeven pricing by the largest margin observed in 18 years. Second, the post-COVID period — which contains the recent inversion regime — does not yet have a completed 5-year forward window, so this analysis cannot judge whether the current inverted breakeven structure is “correctly” priced relative to inflation that has yet to occur.

Historical Turning Points

January 2003 — T5YIE Series Begins

The FRED T5YIE series, derived from 5-year nominal and TIPS yields published by the US Treasury, begins on January 2, 2003. The first monthly observation reads 1.40% for T5YIE and 1.76% for T10YIE, a spread of −0.36 percentage points. The realized annualized CPI growth from January 2003 to January 2008 was subsequently 3.05% — a forecast miss of approximately −1.6pp, indicating that breakevens substantially underestimated the 2003–2008 inflation episode driven by oil prices and housing.

November 2008 — Peak GFC Dysfunction

The 5-year breakeven crashed to −1.40% in November 2008, the lowest single monthly value in the entire FRED T5YIE series. The 10-year held at 0.64%, producing a spread of −2.04pp — the most extreme reading in either direction across 280 observations. The mechanical cause was not deflation expectations but TIPS market illiquidity: dealer balance sheets contracted, the natural buyer base for inflation-linked paper retreated, and TIPS yields rose sharply against nominal yields. This episode is treated as a separate analytical category throughout the page; its values are not comparable to other regime data.

March 2020 — COVID Breakeven Collapse

In March 2020, T5YIE fell to 0.67% and T10YIE to 0.99% as markets repriced for a deflationary recession. Both values were the lowest since the GFC dysfunction window. The subsequent 5-year realized annualized CPI growth from March 2020 to March 2025 was 4.38% — meaning the breakeven at that date underestimated future inflation by 3.71 percentage points annualized, the third-largest miss in the series. The May 2020 observation (T5YIE 0.77%, realized 4.62%) holds the record for largest miss at −3.85pp.

March 2022 — Peak T5YIE Post-COVID

T5YIE reached 3.41% in March 2022, the highest single monthly value in the FRED T5YIE series since its inception in January 2003. T10YIE was at 2.85%, producing the maximum spread reversal in the entire series: +0.56pp. CPI year-over-year growth at that date stood at 8.57%, near the cycle peak. The current Post-COVID phase began roughly a year earlier (April 2021) and has continued through the publication date with persistent positive spread.

April 2026 — Current Observation

The latest monthly observation places T5YIE at 2.60% and T10YIE at 2.38%, a spread of +0.22pp. The 5-year breakeven sits 60 basis points above the 2% Fed target, slightly more than the median 10-year breakeven during the Post-COVID phase (2.33%, 33bp above target). The post-COVID inversion regime has persisted for 61 consecutive months, with 45 of those months showing T5YIE above T10YIE. The trailing 6-month average spread has stayed continuously above zero since February 2025 (15 consecutive months).

Methodology

This dataset combines the FRED-published monthly breakeven inflation series (T5YIEM and T10YIEM) with the seasonally-adjusted CPI for All Urban Consumers (CPIAUCSL), derived columns computed in Python from the merged data, and a manually-defined phase taxonomy reflecting documented macro regimes. All numbers in the HTML page are derived from the published CSV.

Core Formula

Filter Definitions

‘Post-COVID period’ = date >= ‘2021-04-01’ (also referred to as ‘since April 2021’)

‘Post-2022’ = date >= ‘2022-01-01’ (also referred to as ‘since 2022’)

‘Since 2021’ = date >= ‘2021-01-01’ OR date >= ‘2021-04-01’ (Post-COVID phase)

‘GFC dysfunction’ = (date >= ‘2008-09-01’) AND (date <= ‘2009-03-01’)

‘Ex-dysfunction’ = NOT GFC dysfunction

‘Reversed regime’ = spread_5_10 > +0.10pp

‘Normal upward regime’ = spread_5_10 < −0.10pp

‘Flat regime’ = abs(spread_5_10) <= 0.10pp

Regime Selection Criteria

A ‘normal upward’ observation is defined as one where T5YIE − T10YIE < −0.10pp.

The ±0.10pp threshold corresponds to roughly one daily standard deviation of the spread

during stable periods; smaller flips are not interpretable as regime changes.

Sensitivity test on the reversal threshold: setting the band to ±0.05pp produces 55 reversed, 36 flat, 189 normal-upward observations; setting it to ±0.15pp produces 21 reversed, 135 flat, 124 normal. The core empirical finding — the absence of any T5YIE > T10YIE observation in 2010–2019 — is robust to all threshold choices because the maximum spread during that decade was −0.03pp (June 2016), well below any reasonable noise threshold. Setting the threshold to zero produces the same headline: 0 of 120 months in 2010–2019 show 5Y > 10Y.

Sensitivity test on the “2010–2019” window choice: substituting the window 2009-04 to 2019-12 (the immediate post-dysfunction recovery extended through the Liftoff period) yields 129 of 129 months with T10YIE > T5YIE. Substituting 2011-01 to 2019-12 yields 108 of 108. Substituting 2010-01 to 2020-02 (pre-COVID) yields 122 of 122. The absence-of-inversion claim is invariant to reasonable boundary shifts.

Dataset Design

| Variable | Type | Unit | Source | Calculation |

|---|---|---|---|---|

| date | date | YYYY-MM-DD | FRED | direct |

| t5yie | float | % | FRED T5YIEM | direct |

| t10yie | float | % | FRED T10YIEM | direct |

| spread_5_10 | float | pp | derived | t5yie − t10yie |

| spread_sign | str | categorical | derived | sign(spread_5_10) |

| regime_term_structure | str | categorical | derived | function of spread_5_10 vs ±0.10pp threshold |

| cpi | float | index | FRED CPIAUCSL | direct (SA) |

| cpi_yoy | float | % | derived | (cpi[t] / cpi[t−12mo] − 1) × 100 |

| cpi_fwd_5y_realized | float | % annualized | derived | (cpi[t+60mo]/cpi[t])^(1/5) − 1, ×100 |

| cpi_fwd_10y_realized | float | % annualized | derived | (cpi[t+120mo]/cpi[t])^(1/10) − 1, ×100 |

| error_5y | float | pp | derived | t5yie − cpi_fwd_5y_realized |

| error_10y | float | pp | derived | t10yie − cpi_fwd_10y_realized |

| liquidity_dysfunction_flag | int | 0/1 | derived | 1 if 2008-09 ≤ date ≤ 2009-03 |

| phase | str | categorical | derived | see Filter Definitions above |

| vol_5y_rolling12m | float | (annualized) | derived | stdev(Δt5yie, 12m) × √12 |

| vol_10y_rolling12m | float | (annualized) | derived | stdev(Δt10yie, 12m) × √12 |

Python Reproduction Code

# Reproduce the core dataset from FRED import pandas as pd import numpy as np # Fetch from FRED (assumes pandas_datareader or direct download) t5 = pd.read_csv("T5YIEM.csv", parse_dates=["date"]) t10 = pd.read_csv("T10YIEM.csv", parse_dates=["date"]) cpi = pd.read_csv("CPIAUCSL.csv", parse_dates=["date"]) df = t5.merge(t10, on="date").merge(cpi, on="date", how="left") df = df.sort_values("date").reset_index(drop=True) # Derived columns df["spread_5_10"] = df["t5yie"] - df["t10yie"] df["cpi_yoy"] = df["cpi"].pct_change(periods=12) * 100 df["cpi_fwd_5y_realized"] = ((df["cpi"].shift(-60) / df["cpi"]) ** (1/5) - 1) * 100 df["error_5y"] = df["t5yie"] - df["cpi_fwd_5y_realized"] # Headline finding decade = df[(df["date"] >= "2010-01-01") & (df["date"] <= "2019-12-01")] n_inversions = (decade["spread_5_10"] > 0).sum() print(f"2010-2019 inversions: {n_inversions} of {len(decade)}") # Output: 2010-2019 inversions: 0 of 120

Limitations on Breakeven Interpretation

This dataset documents the market price of inflation insurance, computed mechanically from Treasury and TIPS yields. It is not equivalent to consumer or survey-based inflation expectations. For triangulation, the Michigan inflation expectations series (FRED: MICH, 1-year; expectations panel 5-10 year horizon), the New York Fed Survey of Consumer Expectations (available from 2013), and the Philadelphia Fed Survey of Professional Forecasters provide complementary measures. Decomposing breakevens into expected inflation, inflation risk premium, and liquidity premium requires modelling assumptions; the Adrian-Crump-Moench model published by the NY Fed is one widely-cited reference framework.

Dataset Download & Reproducibility

280 monthly observations · January 2003 – April 2026 · Licensed under CC BY 4.0.

Data Sources & References

- Primary Federal Reserve Bank of St. Louis, 5-Year Breakeven Inflation Rate (T5YIEM), monthly, retrieved from FRED. Data derived from 5-Year Treasury Constant Maturity and 5-Year TIPS Constant Maturity yields published by the US Treasury Department.

- Primary Federal Reserve Bank of St. Louis, 10-Year Breakeven Inflation Rate (T10YIEM), monthly, retrieved from FRED. Data derived from 10-Year Treasury Constant Maturity and 10-Year TIPS Constant Maturity yields.

- Primary US Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All Items (CPIAUCSL), monthly seasonally adjusted, retrieved from FRED.

- Research Adrian, T., Crump, R. K., & Moench, E. (2013). “Pricing the Term Structure with Linear Regressions.” Journal of Financial Economics, 110(1), 110–138.

- Research D’Amico, S., Kim, D. H., & Wei, M. (2018). “Tips from TIPS: The Informational Content of Treasury Inflation-Protected Security Prices.” Journal of Financial and Quantitative Analysis, 53(1), 395–436.

- Research Gürkaynak, R. S., Sack, B., & Wright, J. H. (2010). “The TIPS Yield Curve and Inflation Compensation.” American Economic Journal: Macroeconomics, 2(1), 70–92.

- Reference Federal Reserve Bank of New York, Survey of Consumer Expectations (SCE), available from 2013, quarterly reports on 1-year and 3-year inflation expectations.

- Reference University of Michigan, Surveys of Consumers, Inflation Expectations (FRED series MICH).

Methodological Limitations

- Breakevens are a composite of expected inflation, inflation risk premium, and TIPS liquidity premium. The page does not decompose these components; readers ought not treat breakevens as a clean measure of expectations alone.

- The TIPS market matured during the early portion of the sample. Direct comparison across 2003-2007 and 2015-2025 must acknowledge institutional evolution; pre-2003 breakeven data is not available in FRED for the 5-year series.

- The September 2008 – March 2009 dysfunction window is treated as a separate analytical category. Including it in distributional statistics distorts every measure of central tendency; excluding it removes seven months from a 280-month sample.

- Forward CPI realization columns are mechanically limited by data availability: cpi_fwd_5y_realized has data through January 2021 (last date with complete 60-month forward window); cpi_fwd_10y_realized through January 2016.

- Forward-window observations overlap by construction (consecutive monthly windows share 59 months of CPI data). Standard hypothesis testing on the forecast-error distribution would require adjustment for this overlap; the page does not perform formal inference.

- The phase taxonomy reflects analyst judgment about macro-regime boundaries, not algorithmic classification. Different boundary choices would shift specific summary statistics but do not affect the core empirical finding of zero inversions in 2010–2019.

Frequently Asked Questions

What is the current US 5-year breakeven inflation rate?

The April 2026 monthly value is 2.60%. The 10-year breakeven is 2.38%, producing a spread of +0.22 percentage points (5-year above 10-year, the “reversed” configuration). The latest daily values are published by FRED and updated each business day with one-day lag.

What does the breakeven inflation rate actually measure?

The breakeven is the difference between a nominal Treasury yield and the yield of a Treasury Inflation-Protected Security (TIPS) of the same maturity. Mechanically, it equals the average inflation rate at which an investor is indifferent between owning the nominal bond and the inflation-linked bond. Economically, it contains three components: average expected inflation over the horizon, an inflation risk premium, and a liquidity premium reflecting the relative depth of TIPS versus nominal Treasury markets. It is not a direct measure of consumer or survey inflation expectations.

Is the breakeven term structure flip a sign that the Fed is losing credibility?

The dataset cannot answer this question directly. What the data shows is that (i) the median 10-year breakeven across the Post-COVID phase has remained 2.33% — approximately 33 basis points above the Fed’s 2% target, within the band typically described as anchored in central bank communications; and (ii) the term structure direction has reversed from the configuration that prevailed throughout the 2010s, and that reversal has persisted longer than any documented inflation shock period in the FRED series. Both observations are simultaneously true. Whether the persistence reflects expectations drift, a slowly resolving near-term shock, or changes in market microstructure cannot be settled from breakevens alone; triangulation with survey-based long-term expectations dispersion is required.

Why was the November 2008 5-year breakeven negative at −1.40%?

The November 2008 reading does not indicate that markets expected −1.4% deflation. During the Lehman aftermath, the TIPS market became severely illiquid: dealer balance sheets contracted, the natural buyer base for inflation-linked paper withdrew, and TIPS yields rose sharply against nominal Treasury yields. The mechanical result is a breakeven that briefly priced inflation below zero, but the underlying cause was a liquidity premium spike, not a deflation forecast. The page flags this seven-month window (September 2008 – March 2009) as a separate analytical category.

How accurate have 5-year breakevens been at predicting realized inflation?

Across observations from 2003 through January 2021 (the last date with a complete 5-year forward window), the 5-year breakeven understated subsequent annualized CPI growth by a median of 0.28 percentage points during periods when the term structure was in its conventional configuration (10Y > 5Y). The largest forecasting failure in the series occurred in March-May 2020: breakevens then averaged approximately 0.73% while realized annualized CPI growth over the subsequent five years was approximately 4.5%, a miss of roughly 3.8 percentage points. The most recent inversion regime (post-2022) does not yet have a completed forward window for direct comparison.

Why are pre-2008 inversions ignored in the headline finding?

They are not ignored — the page documents that 24 of 68 months from 2003 to August 2008 saw the 5-year exceed the 10-year, typically during brief oil-price episodes. The contrast the page draws is not between “always normal” before and “reversed” after; it is between the unprecedented persistence of inversion since 2021 (45 of 61 months) and the absence of any inversion across 129 consecutive months from April 2009 through February 2020. No prior 5-year window in the series contains anything resembling a 74% inversion frequency.

What does this dataset not measure?

This dataset measures the market price of 5-year and 10-year inflation insurance, derived from Treasury and TIPS yields. It does not measure: consumer inflation expectations (see Michigan survey, NY Fed SCE); professional forecaster expectations (see Philadelphia Fed SPF); the dispersion or uncertainty of long-term inflation expectations (see SCE distributional reports); or the decomposition of breakevens into expected inflation versus risk and liquidity premia (see Adrian-Crump-Moench model). For any inference about whether long-term expectations are “anchored” in the deeper sense of the term, triangulation with at least one survey-based measure is required.

Source

Related Eco3min Research

Last updated — 18 June 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.