T10YIE vs CPI: The Divergence Between 10-Year Expectations and Realized Inflation as a Real-Time Signal

T10YIE measures what markets expect; CPI measures what has actually materialized. The gap between the two is not an anomaly to be corrected — it is a signal in its own right, whose reading requires distinguishing level, direction, and cycle phase.

TL;DR

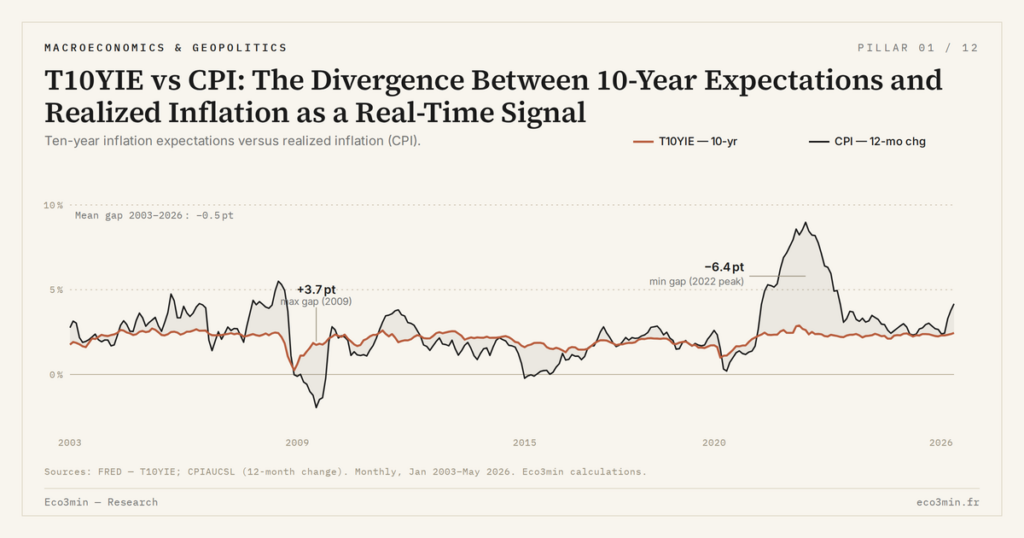

Over 2003-2026 the T10YIE − CPI gap averaged just +0.3 points but swung from -6.1 to +2.2; its sign and direction matter as much as its level.

- A positive gap is the default, holding in roughly 60% of months over 23 years as expectations stay near 2% while trailing CPI cycles between 0% and 9%.

- The sign flip led policy: the gap turned negative in June 2021 (CPI 5.4% vs T10YIE 2.3%), five months before the November 2021 abandonment of 'transitory'.

- Four configurations of level and direction separate a credible disinflation from a de-anchoring test, as in the 2022-2023 exit.

- Since 2024 the gap runs near +0.7 points as trailing CPI decelerates toward 2.4% against a T10YIE around 2.3%.

This article exposes the T10YIE − CPI gap as a near-real-time mismatch indicator between market projection and public statistics. For the broader picture, see T10YIE as the 10-year expectations measure.

1. The nature of the T10YIE − CPI gap: what it actually measures

T10YIE and CPI measure two different things. T10YIE is a market expectation about average inflation anticipated over the coming decade, expressed at daily frequency and reflecting bond arbitrage between nominal Treasuries and TIPS. The US CPI measured by the Bureau of Labor Statistics (FRED series CPIAUCSL) is a statistical index published monthly capturing price changes over the past twelve months — that is, a realized backward-looking average, not a forward projection.

The gap between these two quantities is not a methodological error but an analytical measure in itself. When T10YIE durably exceeds trailing 12-month CPI, markets are pricing an acceleration that the published statistic has not yet captured. When T10YIE is below trailing CPI, markets are pricing a deceleration that monthly data have not yet revealed. This property makes the T10YIE − CPI gap a near-real-time indicator of mismatch between market projection and public statistical reality.

Over 2003-2026, the average gap between T10YIE and trailing 12-month CPI comes in at +0.3 percentage points according to Eco3min calculations on FRED series. This average figure however masks considerable volatility: the historical range goes from -2.5 points (July 2022, when CPI peaked at 9.1% trailing while T10YIE had not exceeded 2.99%) to +2.2 points (May 2020, when trailing CPI had dropped to 0.1% during the COVID shock while T10YIE was already rebounding). This dispersion is the heart of the signal: the gap is never stably zero.

To rigorously interpret this gap, one needs a simple T10YIE definition to frame the gap: T10YIE is not a forecast of future CPI, it is an implicit average projection augmented by an inflation risk premium and netted of a TIPS liquidity premium. The instantaneous T10YIE − CPI gap therefore conflates three distinct pieces of information: difference in nature (prospective vs retrospective), difference in method (market vs statistic), difference in horizon (10-year average vs 12-month trailing).

2. Reading the gap level: positive vs negative, historical ranges

A positive gap — T10YIE above trailing CPI — is the typical state of the US regime: over 23 years of observation, the gap has been positive in roughly 60% of months. This dominance reflects the anchoring mechanism of expectations around the Fed’s 2% target while trailing CPI oscillates by cycle between 0% and 9%. When the economy is in a cyclical disinflation phase — trailing CPI declining but staying positive — the gap widens positively because T10YIE stays close to 2% while CPI converges toward 1% or less.

A negative gap — T10YIE below trailing CPI — typically appears during inflation acceleration phases where the realized statistic exceeds long-term expectations. This was the configuration observed during the 2022 peak: trailing CPI hit 9.1% in June 2022 while T10YIE topped at 2.99%, that is a record negative gap of -6.1 points in June 2022. This type of gap is by construction transitory: either CPI retreats toward the expected level, or T10YIE moves toward realized CPI (de-anchoring signal). Understanding which scenario unfolds links to the self-fulfilling mechanism in expectations.

Historical ranges by cycle phase are instructive. In stable expansion (2003-2007), the average gap was +0.5 points. In cyclical deflation (2008-2009), it reached +2.0 points. In post-2008 disinflation (2010-2015), it tightened around +0.3 points. During 2016-2019, it stayed contained between +0.2 and +0.8 points. The 2021-2022 shock sent the gap diving to -6.1 points before a rapid rebound. Since 2024, the gap has oscillated around +0.7 points on average, echoing the trailing CPI deceleration toward 2.4% while T10YIE stays at 2.3%.

This variability by cycle phase implies that the level alone is insufficient. A gap of +1 point does not mean the same thing in 2014 (exit from deflation phase, normalization signal) as in 2025 (exit from inflation phase, contained disinflation signal). This is why the reading requires also examining the direction of variation and the cycle phase in which the observation fits. Background: what each inflation regime implies for assets.

3. Reading the direction of variation: widening vs narrowing

Beyond the level, the direction of variation of the gap is itself an analytical signal. Four main configurations are encountered. First case: a positive gap widening, T10YIE rising while trailing CPI stays flat. This move signals a market expectations drift without immediate confirmation in realized data — typically the precursor signal of an upward inflation turn. The widening gap functions as a leading indicator on macro desks.

Second case: a positive gap narrowing, T10YIE falling while trailing CPI rises. This move signals on the contrary that markets are embedding a rapid return to the Fed target despite a still-elevated statistic — the typical configuration of a credible disinflation phase. This is what was observed in the second half of 2022 and throughout 2023.

Third case: a negative gap deepening, trailing CPI rising faster than T10YIE. This is the most dangerous configuration for the Fed: the statistic exceeds expectations, anchoring is tested, but markets still embed a return to target. If the negative gap persists, it means either that markets are wrong (inflation will actually retreat rapidly) or that they are about to de-anchor (T10YIE will rise to meet CPI). This is precisely the test of the 2022 episode.

Fourth case: a negative gap narrowing, trailing CPI falling faster than T10YIE rises. Successful-exit configuration from an inflation shock, where the statistic retreats to meet the market projection that never truly de-anchored. This was the configuration observed in late 2022 and early 2023, allowing the Fed to qualify the return to anchoring.

4. Reading by cycle phase: shock exit vs tension onset

The third dimension of analysis is the cycle phase in which the gap is observed. The same +0.5 point gap has opposite meanings exiting a deflation phase and starting an inflation phase, because the forces carrying it are different. The distinction is facilitated by simultaneous tracking of derivatives: T10YIE change over 30 and 90 days, core CPI change over 3 and 6 months.

Exiting an inflation shock — typically 2023-2024 — the gap becomes positive again through CPI deceleration faster than the T10YIE decline. This configuration is interpreted as a monetary-policy success: markets anticipated the return to target, and the statistic converges. The theoretical framework for this interpretation is documented in the analysis of the current T10YIE corridor.

Onset of inflation tension — typically late 2020 and 2021 — the gap starts positive and stable, then progressively flips toward negative as CPI accelerates faster than expectations readjust. This transition constitutes the most relevant warning signal: the sign flip of the gap precedes the actual Fed reaction by several quarters. In 2021, the gap became negative in June (CPI 5.4% vs T10YIE 2.3%) — that is, five months before Powell’s November 2021 pivot abandoning the “transitory” qualification.

This property of the gap leading the Fed reaction is one of the operational reasons why systematic tracking of T10YIE − CPI fits the macro reading beyond monthly CPI releases. The breakeven and the monthly statistic are two complementary indicators: neither alone captures the full dynamics, but their instantaneous gap considerably enriches the inflation-cycle reading grid.

A final observation concerns signal stability. Over 2003-2007, 2014-2019, and 2023-2026, the T10YIE − CPI gap oscillated in narrow ranges of +0.2 to +1.0 points, corresponding to macroeconomic phases without major inflation tension. Over 2009-2010, 2021-2022, and briefly 2020, the gap exited this zone with significant amplitude. Exiting the range is therefore, in itself, a signal — gap stability confirms that market and statistic are aligned, while a sharp move signals a regime transition worth examining.

One operational point closes the framework: for the gap to function as a reliable signal, it must be tracked alongside its decomposition into the three components blended in T10YIE — pure expectations, inflation risk premium, TIPS liquidity premium. A widening gap driven by rising pure expectations carries a different policy meaning than the same widening driven by an expanding risk premium. The Federal Reserve Bank of New York ACM decomposition allows this fine-grained reading, though it requires quarterly updates rather than daily. The pragmatic approach for non-specialists is to monitor the raw gap on a daily basis and the decomposed gap quarterly, accepting that the raw signal is useful but imperfect.

- The T10YIE − trailing 12-month CPI gap measures the mismatch between market projection and realized statistic. Historical 2003-2026 mean: +0.3 points. Range: -6.1 to +2.2 points depending on cycle phase.

- The gap level alone is not enough: the same +1 point has opposite meanings exiting a deflation phase (normalization) and exiting an inflation phase (contained disinflation).

- The direction of variation is as informative as the level: a positive gap widening signals an expectations drift; a positive gap narrowing signals credible disinflation.

- The T10YIE − CPI gap typically leads the Fed reaction by several quarters. The sign flip (positive to negative) preceded by five months Powell’s November 2021 pivot on the “transitory” qualification of inflation.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…