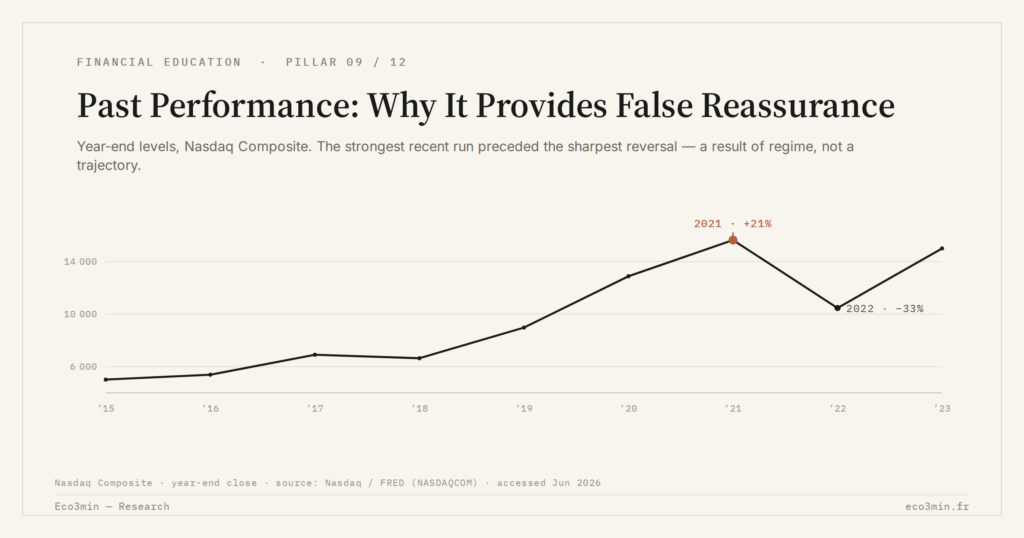

Past Performance: Why It Provides False Reassurance

Past performance reflects a given market regime, not a future trend. This reading bias remains one of the most costly for retail investors.

Past performance often gives an impression of continuity. Yet it mainly reflects a market context that has already passed — a regime of rates, growth and liquidity that can change quickly.

Past performance reflects a given market regime, not a future trend. This reading bias is one of the most costly for investors.

TL;DR

Over twenty years, the average US equity fund investor captured only about 60% of market return (Dalbar, 2025); the gap came from buying after rallies and selling after drawdowns.

- The S&P 500's fivefold rise from 2010 to 2021 reflected near-zero rates and tech-led growth, a regime that reversed in 2022 when the Nasdaq fell roughly 33% after gaining about 21% the year before.

- Extrapolation bias leads retail investors to overestimate by 40% to 60% the odds a recent trend continues (BIS, March 2025), pushing capital in after rallies and out after drawdowns.

- The funds drawing the most subscriptions in a given year underperform their category on average over the next three years (Morningstar, 2025).

A fund that gained 15% last year naturally attracts attention — and capital. Yet past performance is the reflection of a given market regime: a context of rates, growth and volatility that does not necessarily repeat. Extrapolating that result amounts to driving while looking in the rear-view mirror. The bias is one of the most widespread among retail investors, and one of the most costly.

What this question shifts in the analysis: the warning “past performance is not indicative of future results” appears on every regulatory document. It is read, rarely internalised. The human brain is structurally wired to extrapolate recent trends, even when it knows the extrapolation is invalid.

What Past Performance Actually Describes

Every financial return is the product of a specific market regime. Between 2010 and 2021, equity markets benefited from an exceptional combination: rates near zero, large-scale liquidity injection, growth driven by the technology sector. The S&P 500 multiplied fivefold. This result does not describe an intrinsic property of equities — it describes a regime that has since changed. Read alongside: the framework on our financial simulation tools.

According to Morningstar (2025 annual flows report), the equity funds attracting the most subscriptions are systematically those posting the best one- to three-year performance. This “performance chasing” behaviour has a measurable cost: per the same study, the most subscribed funds in any given year underperform their category on average over the following three years.

Extrapolation Bias: Why the Brain Extends the Curve

According to research published by the BIS (Quarterly Review, March 2025), retail investors overestimate by 40% to 60% the probability that a recent trend will continue. This bias is amplified by cognitive availability (recent performance is the most visible) and confirmation bias (investors look for signals that validate their initial choice). Amplification aside, the weighting of probabilities is itself skewed — a distortion that belongs to prospect theory and the weighting of probabilities.

This mechanism explains why investment flows are procyclical: capital enters after rallies and exits after drawdowns. According to Dalbar (QAIB 2025), the average US equity fund investor captured roughly 60% of market return over twenty years — the rest was lost to mistimed entries and exits. This gap connects to the risk-time-liquidity reading framework: without prior framing, past performance replaces analysis with emotion. A companion piece: the history of entering at the top.

What the Current Context Makes More Visible

The shift in the monetary regime that began in 2022 illustrates this mechanism. The Nasdaq lost roughly 33% in 2022, after gaining roughly 21% in 2021. By early 2026, equity markets have partly recovered. Consensus expects further gains, supported by falling rates. Yet that consensus itself rests on extrapolating a recent trend. According to the IMF (October 2025), global growth is expected to slow to 2.8% in 2026 — consistent with rising markets, but also with corrections if earnings expectations disappoint.

The financial industry uses past performance as a marketing tool while displaying the regulatory disclaimer. Savers receive an attraction message and a caution message simultaneously. The outcome is predictable: attraction wins.

Selecting a fund or ETF primarily on the basis of one- to three-year performance. That criterion picks the products that benefited from the recent market regime — not those that are structurally robust. Past performance is a descriptor, not a predictor.

What would invalidate this reading is a demonstration that some managers deliver persistent and identifiable outperformance ex ante across different market regimes. Academic data (SPIVA mid-2025) show that this persistence remains statistically marginal and difficult to distinguish from luck over the horizons observed.

Past performance describes a result in a given context. It promises nothing about the next one. The observation does not lead to inaction — it leads to grounding decisions in structural criteria rather than backward-looking figures, within the framework of everyday savings trade-offs.

- The most subscribed funds in any given year underperform their category on average over the following three years (Morningstar, 2025).

- The average investor captures only about 60% of market return over twenty years, the rest lost to procyclical entries and exits (Dalbar, 2025).

- Extrapolation bias leads investors to overestimate by 40% to 60% the probability that a recent trend will continue (BIS, 2025).

Last updated — 28 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

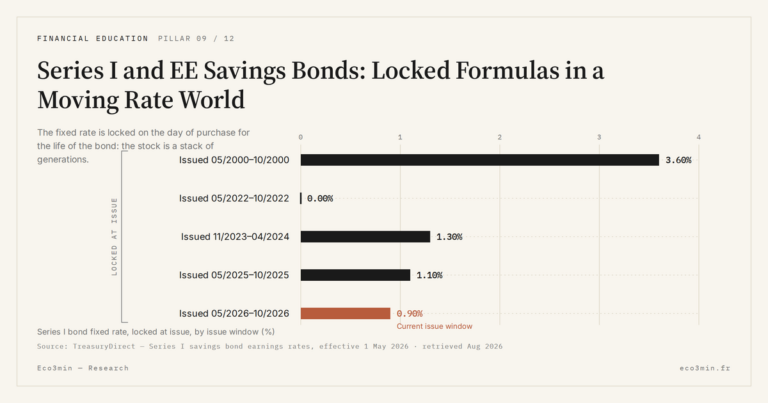

Full pillar →Series I and EE Savings Bonds: Locked Formulas in a Moving Rate World

US savings bonds lock a rate formula at the moment you buy them, for the life of the…

Where the Livret A’s Money Goes: The Caisse des Dépôts Circuit and Social-Housing Finance

The savings held on Livret A accounts do not sit idle. A regulation-set share is centralised at the…

France’s LEP vs the Livret A: A Means-Tested Higher Rate, Explained

France’s Livret d’épargne populaire is often described as "the Livret A, only better". The description misleads: the LEP…