Why We Talk About Recession Before It Actually Exists

The word "recession" often dominates economic debate well before any contraction materializes. False alarms outnumber actual downturns, reflecting a structural media bias toward downside risk over stability scenarios.

The word “recession” surfaces in public discourse long before any cycle turn appears in the data — and the gap between narrative frequency and measured contraction is structural, not accidental.

TL;DR

The word "recession" dominated headlines in 2022, 2023 and late 2025 without G7 economies tipping into contraction, a structural gap between narrative frequency and measured data.

- Google Trends shows US "recession" searches peaked in June 2022, yet revised GDP recorded no technical contraction that year and the NBER has dated no US recession since the March-April 2020 episode; downside risk simply draws more media engagement than stability.

- The premature narrative is partly self-fulfilling: in December 2025 the New York Fed's yield-curve indicator put 12-month recession probability near 25%, well below the roughly 40% alert threshold, while over 55% of Americans surveyed believed the economy was already in or entering recession.

“Recession” enters economic debate well before any documented contraction in activity. The term reflects anticipation of risk more than measured reality. Media narratives amplify the projection by transforming a probability into near-narrative certainty. Confusion between possible scenario and accomplished fact fuels premature diagnoses. The dynamic shapes collective perception of the cycle without altering its immediate reality — and it eventually weighs on the expectations of economic agents themselves.

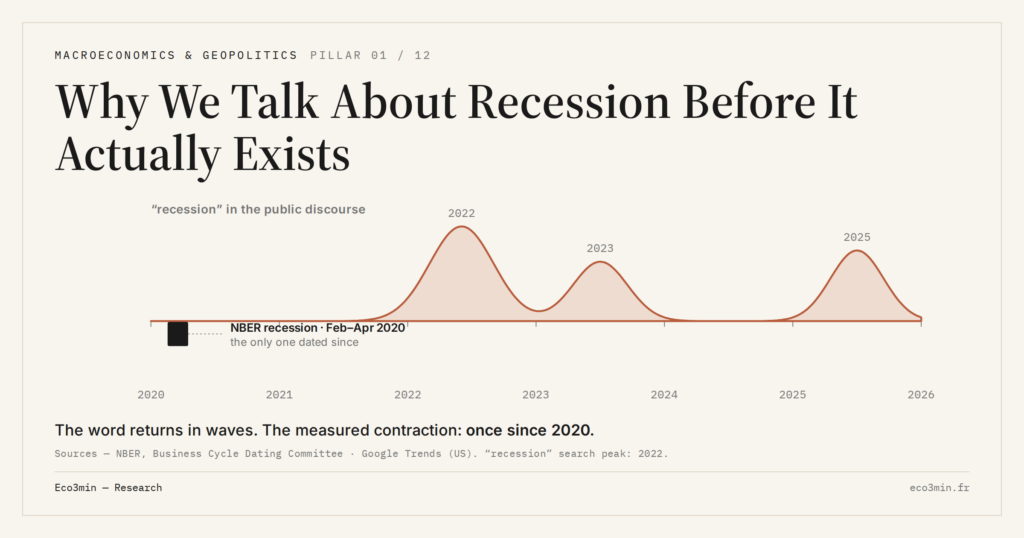

The reflex returns with a regularity that deserves scrutiny. In 2022, then in 2023, then again in late 2025, the word dominated economic headlines without G7 economies tipping into actual contraction. The recurrence of these false alarms erodes the term’s diagnostic value and complicates the reading when a real turning point finally arrives.

When the narrative precedes the facts

Google Trends shows that searches for “recession” in the United States peaked in June 2022 — yet US GDP, after revisions, recorded no technical contraction that year. The NBER, the sole official arbiter of US recessions, has identified no recession since the March-April 2020 episode. The gap between the word’s frequency in public discourse and its materialization in the data is structural.

That gap reflects an asymmetry in media incentives. Downside risks generate more engagement than stability scenarios. A headline announcing recession risk captures more attention than an article describing a moderate slowdown. The real economic cycle, in its progressive construction, does not produce the spectacular breaks the narrative calls for — and the gulf between perception and data is the visible symptom of that mismatch.

The partial self-fulfilling risk

Premature use of the word “recession” is not without consequence. Confidence indices that capture subjective perceptions react to the narrative climate as much as to actual data. When the ambient discourse hammers recession risk, households postpone purchases and businesses freeze investment — feeding the slowdown they were warning about, in a partially self-fulfilling logic. Once an anticipated risk changes behaviour, it becomes an economic fact in its own right — the terrain of the study of economically consequential narratives.

The New York Fed publishes a recession-probability indicator derived from the yield curve. In December 2025, the indicator estimated the probability of recession within 12 months at around 25% — a moderate level, well below the alert threshold typically retained at roughly 40%. General public surveys conducted at the same time showed that more than 55% of Americans believed the economy was “already in recession” or about to enter one. The gap between the technical reading and popular perception measures the magnitude of the narrative bias.

Each phase of the cycle covers a specific configuration that deserves to be named with precision. A slowdown is not a recession. Stagnation is not contraction. Inflating catastrophist vocabulary degrades the quality of diagnosis by reducing a nuanced spectrum of situations to a binary alternative — it works or it does not.

- The word “recession” appears in public discourse well before any measured contraction — false alarms outnumber actual recessions over the past two decades.

- Media coverage amplifies downside risks relative to stability scenarios, producing a permanent narrative bias.

- Premature use of the term can be partially self-fulfilling by weighing on confidence and on the decisions of economic agents.

The symmetric risk of caution deserves attention. Minimizing a real turning point because prior alarms were false leaves observers unprepared. The analytical mechanisms of the business cycle invite a distinction between narrative noise — recurrent and uninformative — and convergent signals across multiple data points, which alone justify a change in diagnosis.

Last updated — 30 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…