Why More Data Does Not Make Markets More Stable

Despite the proliferation of data, algorithmic trading can reinforce volatility through synchronized feedback loops, where similar models react to common signals.

Despite more abundant data, algorithmic trading can reinforce volatility through synchronized feedback loops.

TL;DR

When many algorithms read the same datasets, the market's own reaction becomes a new data point, feeding loops that push an initial move further in the same direction.

- Aggregate estimates at end-2025 attribute more than half of intraday volume in certain liquid asset classes to automated strategies drawing on closely related datasets.

- Because similar models react to similar signals, the market reaction itself is integrated as data, so a modest initial move fuels successive adjustments that reinforce the price direction.

- Short volatility episodes across several developed markets in 2024–2025 produced rapid, concentrated reactions without a major macro catalyst, volatility driven by the speed of circulation rather than a lack of information.

Mass access to information is often seen as a natural factor of market stability. Yet the rise of algorithmic trading shows that the proliferation of data can produce the opposite effect. When decisions align on similar signals, reactions become synchronized. A common confusion is to believe that information neutralizes uncertainty. Analysing feedback loops helps to understand why markets remain unstable despite ever more abundant information.

When information abundance becomes a factor of convergence

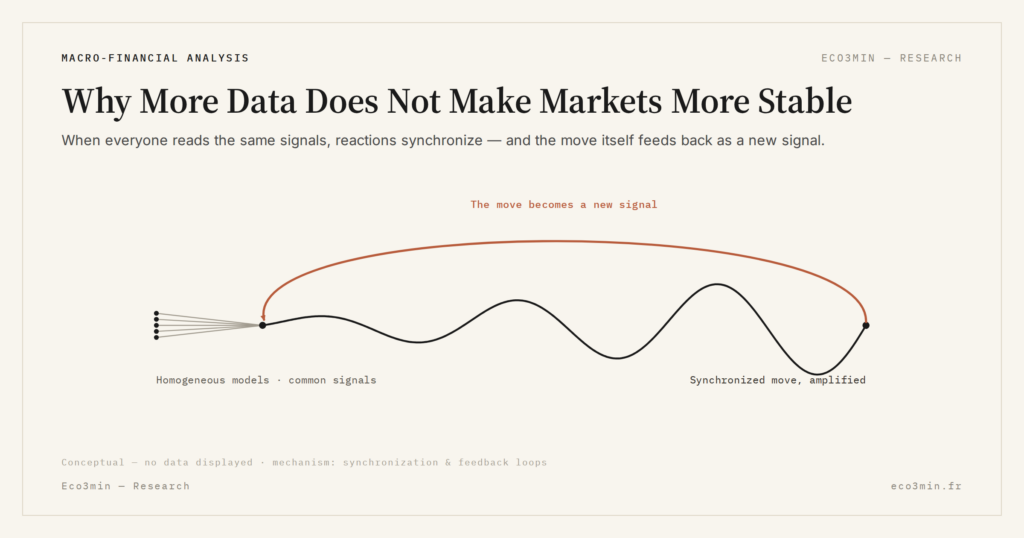

The central mechanism is not data error, but homogeneous use. On liquid markets, a growing share of decisions rests on similar flows: volatility indicators, order-book data, standardized macro signals. As these data become accessible to all, models tend to react in comparable ways.

Aggregate estimates at the end of 2025 suggest that, across certain liquid asset classes, more than half of intraday volumes are triggered by automated strategies using closely related datasets. This informational concentration narrows divergences in reading, but raises the probability of rapid collective movements when signals shift. Fed the same inputs, those models also produce the same output, and that is the systemic cost of model homogeneity in automated trading.

Feedback loops and amplification of moves

Part of the consensus expects more abundant information to improve capital allocation and dampen shocks. This reading assumes that each participant interprets data independently. Yet when similar algorithms simultaneously adjust their positions, the market reaction itself becomes a data point integrated into the models.

This mechanism creates feedback loops: an initial move, however modest, fuels successive adjustments that reinforce the price direction. This suggests that observed volatility does not stem from a lack of information, but from its accelerated circulation in a highly synchronized system. This logic fits within the broader framework analysed in the analysis on the structural transformation of finance by AI, where speed and homogeneity displace risk without eliminating it.

Why this phenomenon is becoming more visible now

In early 2026, the macro context makes these dynamics more perceptible. Real rates remain elevated and liquidity is less abundant than at the start of the decade. In this environment, error margins narrow: synchronized adjustments have more pronounced effects on prices and liquidity.

The short volatility episodes observed between 2024 and 2025 across several developed markets illustrate this point: data that was widely available nonetheless triggered rapid and concentrated reactions, without any major macro catalyst.

What the market reads differently

The central scenario adopted by many participants assumes that continuous improvement of models and diversification of data sources will eventually reduce these effects. This hypothesis rests on the system’s ability to absorb complexity without excessive convergence.

An alternative reading focuses on the very structure of incentives: as long as relative performance is assessed over the short term, models will continue to favour common signals. If this dynamic persists, information abundance could remain compatible with more reactive markets, but not necessarily more stable ones.

What readers really want to understand

The real question is less whether markets have enough data, and more whether this data still allows differentiated risk readings. Behind this question lies a simpler concern: can highly informed markets become more fragile when they all react at the same time?

Observable economic implications

For markets, this dynamic translates into prolonged phases of apparent calm followed by rapid adjustments. For financial firms, it implies heightened attention to intraday liquidity risks and crowding effects. At the macro level, the issue is not the quantity of information, but the diversity of interpretations it still permits.

This mechanism falls more broadly within the transformations tied to financial innovation, where informational efficiency alters the very nature of observed volatility.

Equating abundant information with stability leads to underestimating the synchronization effects and feedback loops specific to algorithmic trading.

Conclusion

More data does not mechanically stabilize financial markets. On the contrary, it can reinforce volatility when decisions become too convergent. This is not the central scenario today, but the risk remains less visible than others — and therefore easier to ignore.

Last updated — 23 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…