Why Employment Stays Calm When the Economy Slows

A solid labor market during a slowdown does not refute the slowdown — it confirms how recent it is. Payrolls move quarters after the rest of the cycle, and the headline rate hides composition shifts that already point the other way.

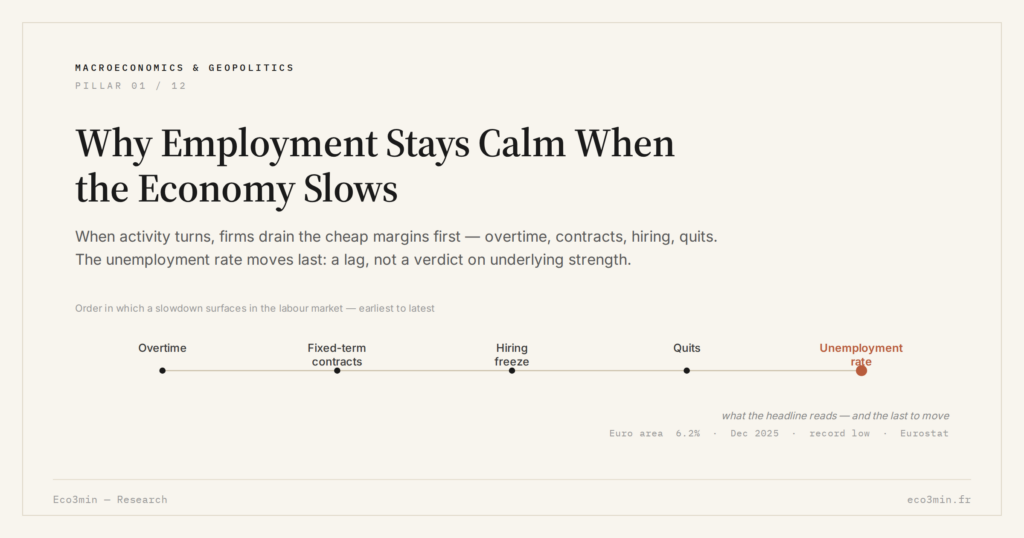

Employment holds up when the economy slows because its adjustment runs several quarters behind the rest of the cycle — a delay, not a verdict on underlying strength.

TL;DR

A firm labor market in a downturn measures the lag between a real-economy turn and its transmission to payrolls, which move several quarters behind activity.

- Eurozone unemployment sat at a historical floor of 6.3% in December 2025 (Eurostat) even as Bloomberg's 2026 growth consensus was cut three times, manufacturing PMIs spent eight months below 50, and the ECB's Q4 2025 Bank Lending Survey flagged tighter credit.

- Earlier levers fire first: eurozone hours worked per employee fell 0.7% year-on-year in Q3 2025 (Eurostat) while employment still rose, and the US JOLTS quits rate dropped to 1.9% in November 2025 (BLS), its lowest outside the pandemic since 2015.

- Composition hollows out the headline: the US full-time employment share fell 0.4 point over the year while involuntary part-time rose 0.6 point (BLS), and eurozone negotiated wages slowed to 3.2% year-on-year in Q4 2025 from 4.5% (ECB), the sharpest deceleration since the series began.

- Part of the calm is genuine labor hoarding: ECB research in late 2025 documented firms holding headcount through margin compression to keep optionality on the recovery, which widens the gap between activity and payroll deterioration.

A labor market still firm while growth decelerates is one of the most reliably misread signals in macro analysis. Markets and commentators routinely treat it as evidence that the slowdown diagnosis is overdone. The reading conflates two clocks. Activity, margins and investment intentions adjust within weeks; payrolls adjust over quarters. A solid unemployment rate does not contradict a slowdown — it confirms that the slowdown is recent enough not to have reached the layoff stage yet.

This pattern returned to the foreground in 2025-2026. Eurozone unemployment sat at 6.3% in December 2025 according to Eurostat, a historical floor. Over the same window, Bloomberg’s consensus growth track for 2026 was revised down three times, manufacturing PMIs spent eight consecutive months below 50, and the ECB’s Bank Lending Survey (Q4 2025) flagged a further tightening of credit conditions. The labor calm reassures markets. Read against the rest of the dashboard, it more plausibly describes the lag between a real-economy turn and its transmission to payrolls.

Why payrolls move last

The mechanics of payroll adjustment in a slowdown are well documented. Firms protect headcount until cheaper levers are exhausted: overtime is cut, temporary contracts are not renewed, hiring freezes spread, then training budgets and capex slip. Only once these margins are drained do separations begin. Each layer of adjustment is invisible in the headline unemployment rate, which captures the final stage of the sequence. Readers can consult our JOLTS layoffs and discharges dataset for the detailed numbers.

The 2025 European data already show several of these earlier layers firing. Hours worked per employee in the eurozone fell 0.7% year-on-year in Q3 2025 according to Eurostat, while total employment kept rising. In the United States, the JOLTS quits rate dropped to 1.9% in November 2025 (BLS), the lowest reading since 2015 outside the pandemic — a sign that workers themselves perceive a less liquid labor market well before that perception shows up in unemployment. The underlying productive cycle integrates these gradients as a predictable sequence rather than a reassuring anomaly.

The headline figure hides the composition

A flat unemployment rate can sit on top of a deteriorating job mix. The most common form of disguised weakness is a shift from full-time to part-time work, often involuntary on the worker’s side. The BLS reported in late 2025 that the share of full-time employment in total US employment had declined 0.4 percentage point over the year, while involuntary part-time work rose by 0.6 percentage point. The headline rate did not move. The composition did. The data behind this: our U-3 vs U-6 vs participation-rate breakdown.

Wage data tell a similar story. Eurozone negotiated wages decelerated to 3.2% year-on-year in Q4 2025 according to the ECB Indicator of Negotiated Wages, against 4.5% a year earlier — the sharpest sequential slowdown since the series began. In real terms, wage gains turned marginal once headline inflation is netted out. This is the typical gap between favorable surface numbers and a deterioration already at work: the rate looks fine, the substance is thinning.

- Employment is a lagging indicator by construction: a calm payroll print reflects a temporal lag, not an absence of slowdown.

- Earlier levers — hours, temporary contracts, hiring freezes, quits — fire several quarters before the unemployment rate moves. The corresponding time series is gathered in our US quits rate dataset.

- Composition matters as much as the headline rate: a shift toward involuntary part-time work can hollow out a labor market without showing up in the official figure.

Labor hoarding: where resilience is partly genuine

The lag explanation does not cover the entire story. A portion of the post-pandemic labor calm reflects a structural shift firms have learned the hard way. Healthcare, construction and parts of the technology sector spent 2021-2023 unable to staff their projects at any reasonable wage. The lesson — letting trained workers go in a downturn means rebuilding the team from scratch when activity rebounds — has changed corporate behavior. ECB research published in late 2025 (Economic Bulletin, Issue 7) documents what economists call labor hoarding: firms holding on to headcount even through margin compression, accepting lower productivity per employee as the price of optionality on the recovery.

The implication for cycle reading is not that the lag has disappeared. It is that the lag now incorporates a deliberate corporate choice on top of the older mechanical sequence. Where labor hoarding is strong, the gap between activity deterioration and payroll deterioration widens. The analytical frameworks governing the business cycle integrate this evolution: the meaning of a steady unemployment rate in 2026 is not exactly what it was in 2008. The diagnostic value of the indicator has thinned, not vanished. By the time payrolls confirm a turning point, the cycle has typically moved several quarters past it.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…