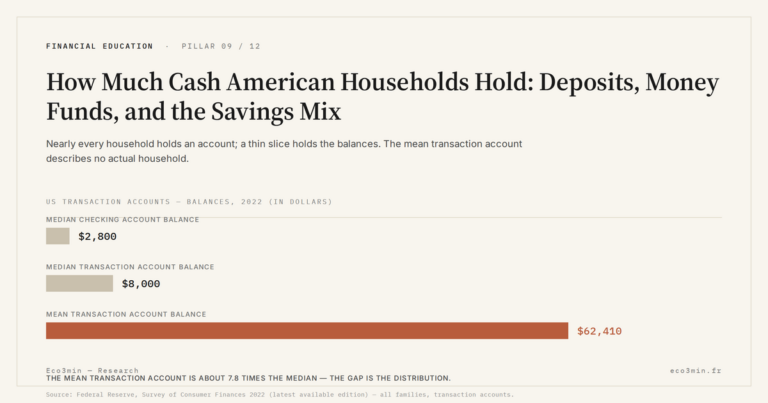

Management Fees: How 1% Erodes Capital Over 20 Years

A 1% annual fee gap looks trivial. Over twenty years it can amount to tens of thousands of euros — without the investor ever seeing it move.

A 1% annual fee gap looks trivial. Over twenty years, it can amount to tens of thousands of euros — without the investor ever seeing it move.

TL;DR

A 1.5-point annual fee gap looks trivial, yet over twenty years it can quietly remove roughly a quarter of final capital — the one cost known in advance.

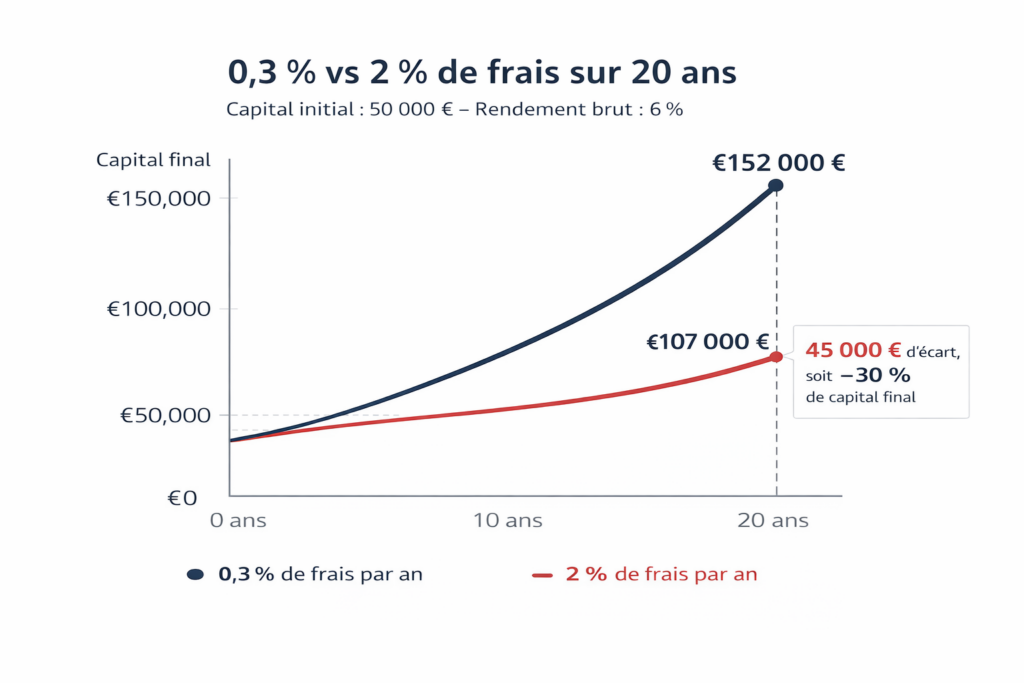

- A €50,000 portfolio compounding at 6% gross reaches about €152,000 over 20 years at 0.3% fees, but only about €107,000 at 2% — a €45,000 gap, near 30% of final capital.

- ESMA puts average European equity-fund fees at 1.7% a year against 0.2% for equivalent index ETFs, a gap it calls systematically underestimated by retail investors (2025).

- Only 23% of fund holders say they know the total fees deducted from their investments (AMF Savings Barometer, 2025).

Management fees are expressed as an annual percentage — rarely as a cumulative absolute value. It is this presentation that makes them invisible. A 1% gap per year between two vehicles looks negligible, yet over twenty years it can represent more than 20% of the final capital. Fees act as compound interest in reverse: they erode return exponentially with time. Building this variable into any product comparison means measuring not what is gained, but what is actually kept. For context: Our study of annuity versus lump-sum taxation.

The most underestimated aspect in this area: fees are not a technical subject reserved for insiders. They are the only parameter of an investment known with certainty in advance — unlike yield, volatility, or market conditions. Paradoxically, this is the variable to which savers pay the least attention.

Compound interest running in reverse

The mechanism is symmetrical to that of compound interest, but in reverse. Where compound interest multiplies gains exponentially, fees erode capital the same way. A €50,000 portfolio invested at 6% gross with 0.3% annual fees reaches roughly €152,000 after twenty years. The same portfolio with 2% annual fees reaches only €107,000. The gap: €45,000, or 30% of the final capital — for a fee differential that looks modest in percentage terms. Compressing that differential is the whole commercial proposition behind the fee-based case for algorithmic portfolio management.

According to ESMA’s annual report on costs and performance of financial products (2025 edition), average fees on equity funds in Europe stood at 1.7% per year, against 0.2% for equivalent index ETFs. Over twenty years, this 1.5-point gap reduces final capital by roughly 25%. The report notes that this impact is “systematically underestimated by retail investors”.

Why fees stay invisible

Three factors explain this underestimation. The first is the annual-percentage presentation: 1.5% looks small in absolute terms, but the cumulative effect over long durations is massive. The second is the absence of explicit billing: fees are deducted directly from the fund’s net asset value, with no visible debit line on the investor’s account. The third is the focus on gross return: marketing documents highlight performance before fees, rarely after.

The AMF has tightened transparency requirements on fees since the MiFID II directive, but studies show that the information provided remains underused by savers. According to the AMF Savings Barometer (2025), only 23% of fund holders report knowing the total fees deducted from their investments. This perceived opacity feeds into a broader question on the relationship to time and yield: what is kept after fees matters more than what the market produces before fees.

The financial-industry consensus acknowledges the importance of fees but treats them as one parameter among others — alongside management quality or diversification. The structural reading is different: fees are the only certain and recurring cost. Everything else — yield, volatility, manager alpha — is uncertain. Minimising the only known parameter means maximising the expected outcome under uncertainty. Worth reading alongside: the Eco3min hub of decision-testing tools and simulators.

Comparing two funds purely on past performance without looking at fees. A fund showing 8% gross return with 2% fees produces a 6% net return — identical to an ETF at 6.2% gross with 0.2% fees. Net performance is the only relevant indicator.

What would invalidate this reading is the emergence of a category of active managers able to durably outperform their benchmark net of fees. SPIVA data (S&P Dow Jones Indices, mid-2025) show this category exists but remains statistically marginal — and difficult to identify ex ante. In the absence of a reliable method to spot them in advance, fee minimisation remains the most robust approach. Fees remain the one term the client controls precisely because the manager’s incentives are not the client’s — the core of the divergence of interest between manager and client.

Management fees are the inverted mirror of compound interest: what time builds, fees deconstruct. Several return scenarios remain open, but the effect of fees is certain and cumulative. Building this variable into every vehicle comparison is a prerequisite for everyday financial choices.

- A 1.5-point gap in annual fees reduces final capital by roughly 25% over twenty years — an exponential effect systematically underestimated (ESMA, 2025).

- Fees are the only investment parameter known with certainty in advance — and paradoxically the least monitored by savers.

- Only 23% of fund holders know the total fees deducted (AMF, 2025) — an information deficit with a measurable cost.

Last updated — 30 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Series I and EE Savings Bonds: Locked Formulas in a Moving Rate World

US savings bonds lock a rate formula at the moment you buy them, for the life of the…

Where the Livret A’s Money Goes: The Caisse des Dépôts Circuit and Social-Housing Finance

The savings held on Livret A accounts do not sit idle. A regulation-set share is centralised at the…

France’s LEP vs the Livret A: A Means-Tested Higher Rate, Explained

France’s Livret d’épargne populaire is often described as "the Livret A, only better". The description misleads: the LEP…