How Real Rates Drive International Capital Flows — and Why the Flows Are Asymmetric

Real rate gaps between regions act as the main driver of cross-border capital allocation. Inflows ease local financing conditions gradually; outflows can reverse abruptly. The asymmetry is what makes the mechanism amplifying rather than stabilizing.

Capital moves toward regions where the risk-adjusted real return is most attractive. That arbitrage principle generates flows large enough to amplify imbalances as often as they correct them — and the amplification comes from the asymmetry between how money arrives and how it leaves.

TL;DR

Real-rate gaps between regions steer cross-border capital, but the flows are asymmetric: money arrives gradually as differentials build and leaves abruptly when they close, amplifying imbalances more than correcting them.

- US 10-year TIPS real rates sit near 2% in early 2026, against ≈0.5% in the eurozone and ≈-0.8% in Japan — a 150-280 basis-point spread wide enough to pull capital toward dollar assets.

- TIC data (Q3 2025) put net foreign purchases of US assets near $850 billion over the trailing twelve months, with the inflow lifting the Dollar Index (DXY) ≈8% above its 2015-2019 average.

- Inflows build gradually, outflows snap shut: portfolio flows to emerging markets reversed direction three times since 2020 (IIF, Q4 2025), each turn aligned with tightening real rates in advanced economies.

- An economy's exposure to abrupt reversals tracks its inflation differential, its monetary credibility and the share of foreign-currency debt on its balance sheet.

Reading international capital flows without tracking the real-rate gap between regions misses the variable that actually drives most of the cross-border allocation decisions.

Real rate gaps between economies set the direction of cross-border capital flows. Mechanics of yield arbitrage and its asymmetric reversals.

Every day, central bank reserve managers, sovereign wealth funds and institutional allocators move hundreds of billions of dollars on an implicit calculation: which market offers the highest risk-adjusted real return? The arbitrage looks technical and produces effects that are anything but. When one economy offers higher real rates than its peers, it pulls in capital that strengthens its currency and eases its domestic financing conditions — at the cost of less remunerative regions. The flows are not symmetric in their effects across the cycle, which is why the chronology of historical curve inversions and their effects on equity indices only makes sense once cross-border yield differentials are added to the picture.

The arbitrage mechanism

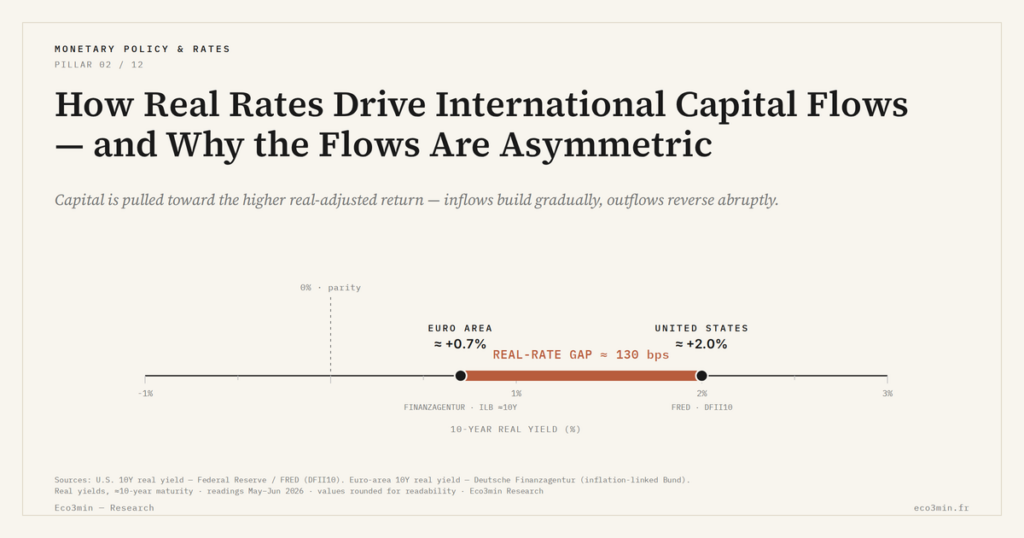

In early 2026, US 10-year real rates trade near 2% on TIPS, against ≈0.5% in the eurozone and ≈-0.8% in Japan, based on each market’s inflation-linked benchmark. A 150 to 280 basis-point gap is more than enough to act as a magnet for capital flows into dollar assets. US Treasury data (TIC, Q3 2025) put net foreign purchases of US assets at ≈$850 billion over the trailing twelve months.

The flow cascades through the rest of the macro picture. Capital inflows support the dollar, with the Dollar Index (DXY) running ≈8% above its 2015-2019 average, which compresses US exporter margins and lowers import costs. The full reach of the arbitrage only becomes visible once the role of real rates as a structuring variable for cross-border decisions is treated alongside their domestic role: real rates do not only shape internal capex tests, they also command the direction of international financial flows.

Inflows are gradual, outflows are not

The destabilizing part of the mechanism is not the direction of the flow at any given moment but its asymmetric profile. Capital attracted by a real-rate differential enters gradually as differentials accumulate — and exits sharply when the gap closes. Emerging economies sit in the most exposed position. According to Institute of International Finance data (IIF, Q4 2025), portfolio flows to emerging markets have reversed direction three times since 2020, each turn aligned with a tightening of real rates in advanced economies. More on this: our breakdown of how monetary policy reaches corporate earnings.

When US real rates rise — as they did between 2022 and 2023 — capital repatriation toward dollar assets puts pressure on emerging currencies, lifts local financing costs and, in the most fragile cases, triggers balance-of-payments stress. The vulnerability is not uniform across economies. It tracks the structural fundamentals — inflation differentials, monetary credibility, foreign-currency debt exposure — that explain why real rates diverge between regions in the first place.

- Real-rate gaps between regions are the principal driver of international capital flows — net foreign purchases of US assets in 2025 directly reflect the dollar’s real-yield advantage.

- Capital flows amplify imbalances more often than they correct them: gradual inflows ease local financial conditions beyond what fundamentals warrant; abrupt outflows reverse those gains faster than they were built.

- The vulnerability of any given economy to flow reversals depends on its inflation differential, its monetary credibility and the share of foreign-currency debt on its balance sheet.

The early-2026 setting — with US real rates well above eurozone and Japanese equivalents — sustains the pull toward dollar assets that only eases as the real-rate gap narrows. That dynamic plays out inside the international financial conditions that structure global yield arbitrage.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…