How Fiscal Policy Interacts With the Real Economic Cycle

Fiscal policy interacts with the real economic cycle through implementation lags, deferred effects and stabilisation mechanisms. Automatic stabilisers act faster than discretionary measures, with major implications for cyclical timing.

Fiscal policy interacts with the real economic cycle through implementation lags, deferred effects and stabilisation mechanisms.

TL;DR

Automatic stabilisers absorb shocks the moment activity slows; discretionary stimulus lands 6 to 18 months later, a lag that can turn a recovery measure into a pro-cyclical impulse.

- Euro-area automatic stabilisers absorb about 40% of cyclical shocks versus roughly 25% in the United States (European Commission, 2025), engaging without any new political decision.

- The US Inflation Reduction Act, adopted in 2022, saw its full effects land in 2024 to 2025 with the economy already above potential, sustaining the inflation the Fed was compressing.

- The euro area shows the mirror image: Stability Pact rules in force since 2024 impose fiscal tightening into fragile growth, a double brake alongside restrictive monetary policy.

Fiscal policy is often presented as an immediate lever on activity. In practice, its effects play out on the timescale of the real cycle, with substantial lags between decision, implementation and economic impact. Automatic stabilisers act fast; discretionary measures arrive late. Fiscal policy can dampen or amplify certain phases of the cycle without creating them. Distinguishing cyclical action from structural dynamics is what separates serious analysis from political commentary on stimulus packages.

This distinction becomes central as fiscal headroom narrows. With public-debt ratios at levels not seen outside wartime in the G7 economies, states’ capacity to play a counter-cyclical role has itself become a variable of the cycle, no longer simply a tool sitting on the shelf.

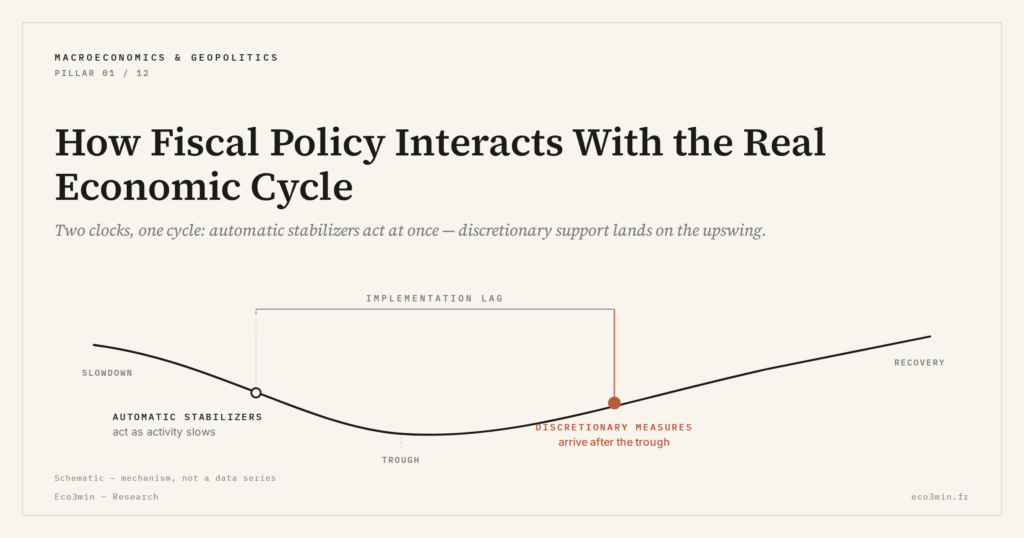

Automatic stabilisers and discretionary measures: two clocks

Automatic stabilisers (unemployment benefits, progressive taxation, indexed social transfers) engage mechanically as soon as activity slows. Their stabilising effect is rapid because no new political decision is required. The European Commission estimated in 2025 that these stabilisers absorbed roughly 40% of cyclical shocks in euro-area economies, well above the level observed in the United States (around 25%).

Discretionary measures (stimulus packages, targeted tax cuts, public investment) carry a structural lag. The average delay between identifying a slowdown and effective implementation of a spending programme is estimated at 6 to 18 months depending on the country (IMF, Fiscal Monitor, October 2025). The implication is that stimulus plans often arrive after the trough of the real economic cycle and its adjustment mechanisms, with the risk of stimulating an economy already in recovery.

The unintended pro-cyclicality risk

The temporal lag creates a pro-cyclicality risk: fiscal stimulus amplifies expansion instead of cushioning the slowdown it was meant to offset. The US Inflation Reduction Act is the textbook case. Adopted in 2022 as a response to the post-Covid shock, its full effects materialised in 2024 to 2025, at a point when the US economy was already running above potential. The impulse contributed to sustaining inflationary pressures that the Fed was simultaneously trying to compress.

The euro area shows the mirror image. The new Stability Pact rules in force since 2024 impose fiscal-adjustment paths on economies whose potential growth remains fragile. This fiscal tightening, combined with restrictive monetary policy, produces a double pro-cyclical brake, a configuration that persistent desynchronisation between major economic zones renders all the more visible. The United States stimulates during expansion; Europe consolidates during weakness. An asymmetry that weighs on the trajectory of the European cycle.

Assuming a stimulus plan acts immediately on growth. Budgetary execution lags (parliamentary votes, public tenders, actual disbursements) create a structural delay of several quarters. Assessing the impact of a fiscal measure at the quarter of its announcement confuses political signal with real economic effect. Timing errors of that kind are also what make published estimates diverge so widely, a dispersion inseparable from the measurement of the fiscal multiplier.

The counter-cyclical role of fiscal policy nevertheless remains irreplaceable in some configurations. During large-scale shocks (deep recession, systemic crisis, pandemic) automatic stabilisers alone are not enough, and discretionary intervention becomes essential despite the lag. The fiscal response to Covid in 2020, despite imperfect targeting, showed that rapid mobilisation of public finances could prevent a collapse of domestic demand. The deeper dynamics of the economic cycle show that the question is not whether fiscal policy intervenes, but when and how, without amplifying the imbalances it is supposed to correct.

Last updated — 22 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…