Why AI Cuts Visible Costs but Raises the Collective Burden

AI lowers visible financial costs but generates invisible systemic costs at the system level. Private savings on standardized operations coexist with rising coordination, supervision and crisis-management costs.

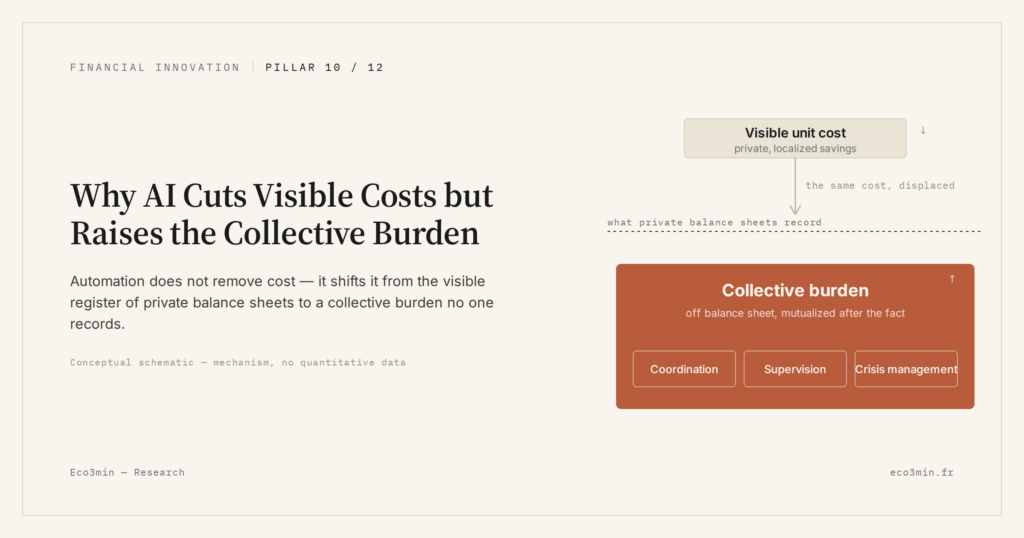

AI lowers visible financial costs but generates invisible systemic costs at the system level.

TL;DR

AI automation has cut unit operating costs by an estimated 20% to 30% in finance's most standardized activities, while shifting less visible coordination and supervision costs onto the whole system.

- Unit savings are real but localized: aggregated end-2025 estimates put operating-cost declines at ≈20% to 30% across finance's most standardized, heavily digitized activities.

- Standardized models and shared-infrastructure dependence synchronize behaviour, trimming some inefficiencies while raising the collective cost of adjustment during stress periods.

- Supervision lags the gains: in 2024–2025, compliance, internal-control and automated-systems monitoring spend grew faster than the savings booked on traditional operating functions.

Financial automation is often associated with a simple promise: doing better at lower cost. In practice, the reduction in unit costs masks the emergence of more diffuse collective burdens that are harder to identify. As processes become industrialized, certain inefficiencies disappear while others arise at the system level. The frequent error consists of confusing private savings with overall efficiency. Examining this gap helps explain why AI can make finance cheaper locally yet more costly structurally. Adjacent reading: Why Automation Makes Finance Harder to Supervise.

Well-identified unit savings…

From a microeconomic perspective, the gains are tangible. Automation in back-office, risk control and execution has significantly reduced processing costs. Aggregated estimates available at end-2025 suggest declines on the order of ≈20% to ≈30% in operating costs across the most standardized activities, particularly on liquid and heavily digitized markets.

This observation feeds an implicit consensus: a more automated finance industry would mechanically be more efficient, and therefore less costly for the system as a whole. This reading assumes that the sum of individual savings automatically translates into collective savings.

… but less visible systemic costs

The analysis diverges on this precise point. Private savings come with costs that are neither borne by the same actors nor immediately observable. The standardization of models, dependence on shared infrastructure and rising volumes processed create congestion effects and collective fragility.

When unit margins decline, incentives shift. Actors compensate through higher volumes, shorter horizons or product complexification. The system becomes denser and faster, but also more costly to maintain, supervise and stabilize. This mechanism fits within a broader dynamic described in the framework analysis on the structural transformation of finance by AI, where efficiency gains shift risk without removing it.

The cost of coordination and supervision

An often underestimated cost concerns coordination. As algorithmic architectures converge, behaviors become more synchronized. This homogeneity reduces certain inefficient gaps, but it raises the collective cost of adjustments during stress periods.

Supervision follows more slowly. In 2024–2025, compliance, internal-control and automated-systems monitoring expenditures grew faster than the savings achieved on traditional operating functions. This additional cost does not cancel private gains, but it weighs on the system as a whole, through stricter regulatory requirements and heavier control infrastructure.

Why this gap is becoming visible now

This issue takes on particular importance in early 2026, against a backdrop of still-elevated real rates and incomplete monetary normalization. Automation models, designed for environments of abundant liquidity, reveal more of their collective costs when funding margins tighten and tolerance for incidents declines.

What the market is reading differently

The central scenario adopted by many actors rests on the assumption that AI will continue to drive overall costs lower through scale effects and improved capital allocation. This reading assumes the system can absorb additional complexity without major friction.

An alternative reading emphasizes that total cost is not measured solely in direct expenses, but also in latent risks, additional capital requirements and potential crisis costs. If this dynamic persists, the system can become cheaper under normal conditions, yet more expensive during stress phases.

Tipping variables to monitor

Several factors could invalidate or attenuate this diagnosis: greater diversification of models, regulation more targeted on systemic effects, or sustained stabilization of financial conditions. Conversely, a liquidity shock, prolonged monetary tightening or excessive concentration of technological infrastructure would amplify the collective cost described here.

Equating the decline in unit costs with a decline in overall cost leads to ignoring the coordination, supervision and crisis-management costs specific to automated systems.

Observable economic implications

For financial firms, this mechanism translates into mounting pressure on control and compliance investments. For markets, it implies phases of highly efficient functioning, but potentially more costly during rapid adjustments. For the economy as a whole, the cost manifests less through visible fees than through heightened fragility during turning points.

- AI-driven savings are first and foremost private and localized.

- Collective costs emerge through coordination, supervision and risk management.

- A system that is cheaper under normal conditions can become more costly during stress periods.

Conclusion

The decline in financial costs linked to AI does not mechanically translate into a reduction in the overall cost of the system. It shifts the burden toward less visible but more systemic dimensions. This is not the central scenario today, but the friction remains poorly integrated into dominant readings — and therefore easier to underestimate.

To place this mechanism in a broader perspective, it fits within the overall logic of financial innovation, where efficiency gains redefine costs as much as fragilities.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…