Why Automation Makes Finance Harder to Supervise

Stacking automated layers improves local efficiency but reduces overall readability, leaving supervisory frameworks behind the complexity they are meant to govern.

The rise of financial automation increases the opacity of decision-making. As models become more interlocked, supervisory capacity progresses more slowly than technical complexity, creating a structural asymmetry in market governance.

TL;DR

More than 60% of operational decisions in the most automated market activities run without direct human intervention (end-2025 estimates), widening the gap between what executes and what supervisors can reconstruct.

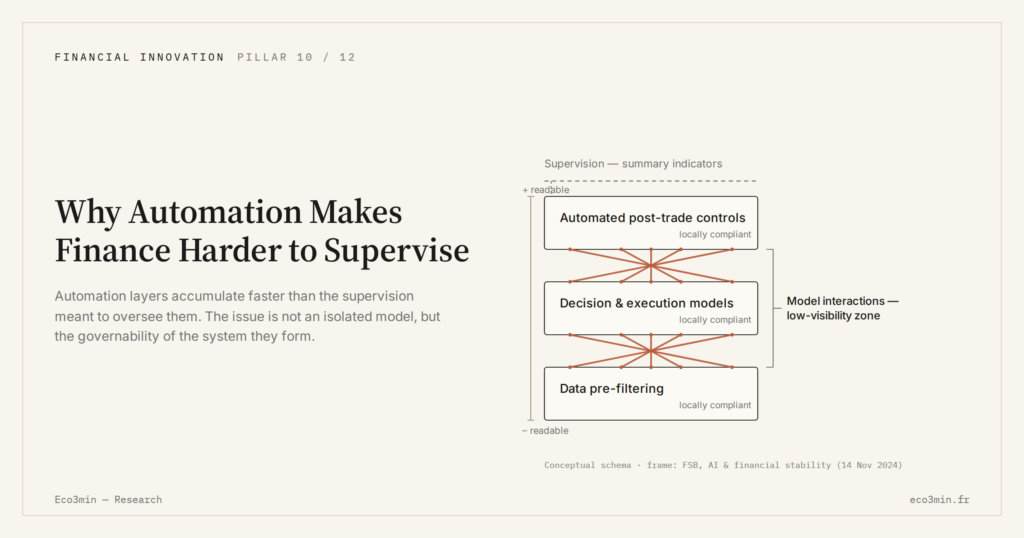

- Since 2024 large institutions have stacked automation layers (data pre-filtering, decision algorithms, automated post-trade controls), each efficient alone but jointly forming a system whose overall logic is hard to reconstruct.

- Systemic risk shifts from isolated failures toward the implicit coordination of interdependent models reacting at once; standardised controls ease local supervision while obscuring those cross-system interactions.

- Model development outpaces the design of supervisory frameworks, and with real rates still elevated in early 2026, cost and speed pressures keep adding technical layers faster than governance can absorb them.

Automated systems improve operational efficiency and execution speed. But their stacking produces interactions that are hard to reconstruct, in which overall understanding recedes despite local sophistication. Equating automation with greater control is a frequent analytical mistake: the issue is not the isolated performance of models, but the governability of the system they form.

A quiet trigger: the layering of model stacks

Since 2024, most large financial institutions have stacked several layers of automation: data pre-filtering models, decision algorithms, then themselves-automated post-trade control systems. Taken in isolation, each layer improves operational efficiency. But their combination creates a system whose overall logic becomes difficult to reconstruct. Stacked this way, those layers are where the practical adoption of AI across the investment process actually happens, far from the demo.

Aggregate estimates available at the end of 2025 suggest that, in the most automated market activities, more than ≈60% of operational decisions are taken without direct human intervention, while supervisory teams have access only to summary indicators. This suggests a growing gap between what is executed and what is actually understandable. Invisible in calm conditions, that gap turns operational continuity as a condition of market functioning into a supervisory question rather than an IT one.

What the dominant consensus assumes

Part of the consensus instead expects automation to improve governance by reducing human error and standardizing control processes. The central scenario adopted by many players assumes that codified rules and automated alerts are enough to offset rising complexity.

The analysis diverges on a precise point: standardization makes local supervision easier, but it reduces the capacity to grasp interactions between systems. When several interdependent models react simultaneously, risk does not arise from an isolated failure but from their implicit coordination. This reading fits within the broader frame of finance’s structural transformation by AI, where automation displaces fragilities into less visible zones.

This rising opacity helps explain why normative frameworks struggle to deliver effective control over financial AI systems, even when processes remain formally compliant.

Why complexity progresses faster than control

The central mechanism comes from an asymmetry of skills and timing. Developing an automated model is often faster than designing a supervisory framework able to test its systemic effects. Controls then focus on process compliance, not on the overall dynamic it generates. Auditing a process while missing the aggregate is precisely the supervisory gap opened by automated decision-making.

At the macro scale, this dynamic is reinforced by an environment of still-elevated real rates in early 2026, which pushes players to continuously optimize costs and execution speed. This suggests that economic pressure favors the addition of new technical layers, without leaving time for full appropriation by governance bodies.

Why this topic is becoming more sensitive now

The monetary tightening underway since 2022 has made liquidity more selective and errors more costly. In this context, the limits of automated control appear more clearly during episodes of localized stress. Rapid adjustments, even when compliant with internal rules, can produce unexpected aggregate effects.

What readers really want to understand

The real question is not whether finance is too automated, but whether it remains governable. Behind this question lies a simple concern: when systems become too complex to be clearly explained, does the capacity to anticipate their failures shrink? Failure here need not be analytical at all: an outage at a shared vendor produces the same result, which is what has turned cyber risk into a systemic concern for finance.

Counter-readings and tipping variables

Some dominant scenarios bet on a gradual strengthening of governance: more frequent algorithmic audits, increased traceability requirements and a stricter separation of functions. That scenario rests on the assumption that regulators and institutions can keep pace with innovation.

Conversely, a liquidity shock, a rapid regulatory change or greater concentration among technology providers could deepen complexity by multiplying interdependencies without improving overall readability.

Observable economic implications

For financial institutions, this complexity translates into a greater dependence on technical teams able to explain automated decisions after the fact. For markets, it implies faster propagation of parameter errors or misread signals. At the macro scale, the issue is not the technology itself, but the system’s capacity to remain intelligible during periods of stress.

This dynamic fits within the broader field of financial innovation, where efficiency gains shift fragility points rather than eliminate them.

Equating automation with stronger control leads to underestimating the interdependence effects between models and the loss of overall readability.

Conclusion

Automation does not make finance uncontrollable by nature, but it deeply alters the conditions of governance. As long as complexity progresses faster than supervisory frameworks, blind spots will persist. This is not the central scenario today, but the risk remains less visible than others — and therefore easier to ignore.

- Stacking models reduces readability without mechanically improving control.

- Supervision focuses more on processes than on systemic interactions.

- Complexity becomes a macro risk when it exceeds governance capacity.

Last updated — 30 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…