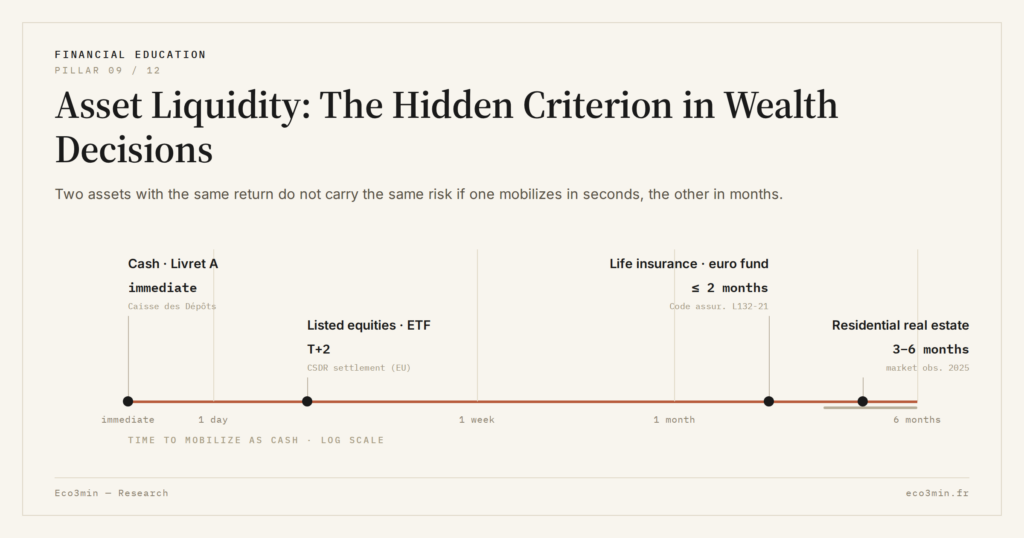

Asset Liquidity: The Hidden Criterion in Wealth Decisions

Two assets with the same historical return do not carry the same risk if one is liquid and the other is not. Liquidity is the property that determines whether wealth can react — and it is almost never priced into the headline return.

Two assets with the same historical return do not carry the same risk if one is liquid and the other is not. Liquidity is the property that determines whether wealth can react — and it is almost never priced into the headline return.

TL;DR

Two assets with identical historical returns carry different risk the moment one sells in seconds and the other in months: liquidity decides whether wealth can react.

- Assets sit on a liquidity scale: the Livret A held €427 billion across 55.5 million holders at end-2025, an MSCI World ETF settles within two business days, and a French property takes three to six months to sell (FNAIM 2025) before notarial delays.

- Illiquidity reshapes real risk three ways: a forced-sale discount estimated at 10% to 20%, deferred valuation where the true price appears only at sale, and an opportunity cost when frozen capital cannot pivot, as when the 10-year OAT moved from 0.2% to over 3% between 2022 and 2024.

- Liquidity is a property of the whole balance sheet, not single assets: wealth that is 90% real estate with three months of precautionary savings sits structurally fragile whatever its nominal value.

- Theoretical and real liquidity diverge under stress: in 2022 several insurers limited withdrawals on euro-fund bond holdings after the rate shock, so the option to sell on paper is not the option to sell quickly without a discount.

Liquidity is the ease with which an asset can be converted to cash without significant loss of value. The criterion is silent in standard performance comparisons: two assets with identical historical returns do not display the same profile if one sells in seconds and the other in months. Liquidity also conditions the capacity to react to an unexpected event or a regime shift. At the scale of the balance sheet, it determines flexibility. Ignoring it means evaluating an asset in a theoretical vacuum free of friction and time constraints — a vacuum that does not exist at the precise moment liquidity matters.

The liquidity scale: from cash to bricks

Wealth assets distribute along a scale that ranges from near-instantaneous to several months. Cash — sight deposits, regulated savings accounts — is liquid by definition. The Livret A, with its 55.5 million holders and outstanding deposits of €427 billion at end-2025 according to Caisse des Dépôts data, offers immediate availability with no penalty and no capital loss.

Listed equities sit one step below. A sell order on an MSCI World ETF executes in seconds on Euronext, with a spread below 0.1% on the most liquid products. Cash settles within two business days. Liquidity is high but not costless — daily volatility is visible, and a forced sale at a cycle trough crystallizes a loss that the listed price already records.

Euro-fund life insurance occupies an intermediate position. Partial withdrawal is technically possible at any time, but the effective payment delay can reach one to two months depending on the insurer, according to data collected by ACPR in its 2024 annual report. The 2022 episode — when several insurers limited withdrawals on bond funds following the rate shock — illustrated how theoretical liquidity and real liquidity can diverge in stress periods.

Residential real estate sits at the bottom of the scale. The average sale time for a property in France runs three to six months according to FNAIM data (2025), with another two to three months of notarial delay on top. Transaction costs — between 7% and 10% on the buyer side, 3% to 6% on the seller side with an agency — constitute an exit cost without equivalent in financial assets. A property is not “available” in the way a savings account is. It is a frozen asset whose mobilization takes time, costs heavily and depends on the state of the local market at the moment of sale. For the broader picture: our read of the simulators that test financial assumptions.

- Treating all assets as equivalent in risk terms when their liquidity profiles diverge by orders of magnitude — a property and an ETF portfolio with the same historical return do not offer the same reaction capacity.

- Confusing theoretical liquidity (the possibility of selling) with real liquidity (the possibility of selling quickly, without discount, at the desired moment).

What illiquidity does to real risk

Illiquidity changes an asset’s risk profile in three distinct ways.

The first is the risk of forced liquidation. A household facing a major unexpected expense — job loss, divorce, health issue — needs to mobilize resources rapidly. If most wealth is in real estate, the only path is to sell the property on a timeline incompatible with urgency. Sales under time pressure carry a discount estimated at 10% to 20% relative to the normal market price, according to observations from professionals in judicial real estate. That discount is the price of illiquidity, paid only when liquidity is actually needed.

The second is the risk of deferred valuation. An illiquid asset reveals its real value only at the moment of an actual transaction. Between two sales, a property’s value is an estimate — based on comparables, indices or online valuations — but not an observable market price. This opacity creates an anchoring bias: the owner tends to retain the most favorable valuation. The correction materializes only on the day of effective listing, which is why a valuation conditional on the moment of measurement changes the reading of real wealth.

The third is the opportunity cost of immobilization. Capital frozen in an illiquid asset cannot be reallocated to a regime shift. When rates rise and long-dated bonds suddenly offer attractive yields — as between 2022 and 2024, when the 10-year OAT yield moved from 0.2% to over 3% according to Banque de France data — the property owner cannot pivot quickly. The holder of a liquid portfolio can do so in minutes.

Balance-sheet liquidity: the only level that matters

Liquidity is not an attribute of individual assets but a property of the complete balance sheet. A wealth profile can contain illiquid assets without that being a problem, as long as the liquid portion covers predictable needs and reasonably anticipable surprises.

The common rule of thumb sets precautionary savings between three and six months of fixed expenses. The rule is necessary but not sufficient. A household whose wealth is 90% real estate and which holds three months of precautionary savings sits in a structurally fragile position: any unforeseen event beyond that reserve forces a sale of the illiquid asset on unfavorable terms.

The composition of the balance sheet depends on the risk profile, income stability and time horizon. The full picture is drawn in this analysis of bitcoin correlation risk assets. A salaried worker on a permanent contract with stable income can tolerate a higher concentration in illiquid assets than a self-employed worker with variable income — historically, the standard deviation of income shocks is markedly higher in the second case, which raises the empirical value of liquid buffers. A balance sheet close to retirement tends to hold more liquidity than one in the accumulation phase, because the capacity to rebuild capital after a forced sale diminishes with age.

It is this dimension of flexibility that makes liquidity the criterion that separates the three roles of wealth. The primary residence is structurally illiquid. Precautionary savings are by definition entirely liquid. Long-term investment can tolerate reduced liquidity, provided the rest of the balance sheet compensates. Mixing these roles without ranking them produces a balance sheet whose rigidity reveals itself at the worst possible moment.

Liquidity is not one indicator among others. It is the parameter that determines whether wealth can adapt. A rigid balance sheet can look solid in calm periods and crack at the first shock.

A frequent misreading frames illiquidity as a behavioral advantage: the inability to sell on impulse is presented as a form of discipline. The framing conflates discipline with constraint. Discipline is a choice made in the presence of options. Constraint is the absence of options. A resilient balance sheet pairs illiquid assets for long-term stability with liquid assets for the capacity to react to contingencies — in proportions consistent with the household’s profile, not in proportions chosen by accident of inheritance or property purchase.

These trade-offs belong to the wider set of long-term financial decisions that determine the balance between balance-sheet rigidity and flexibility.

- Liquidity changes an asset’s real risk: an illiquid asset exposes the holder to forced-liquidation discount, valuation opacity and opportunity cost of immobilization.

- Liquidity is measured at the scale of the complete balance sheet. Wealth that is 90% illiquid is structurally fragile, whatever the nominal value.

- Illiquidity is constraint, not discipline. A resilient balance sheet pairs long-term stability with reaction capacity.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Series I and EE Savings Bonds: Locked Formulas in a Moving Rate World

US savings bonds lock a rate formula at the moment you buy them, for the life of the…

Where the Livret A’s Money Goes: The Caisse des Dépôts Circuit and Social-Housing Finance

The savings held on Livret A accounts do not sit idle. A regulation-set share is centralised at the…

France’s LEP vs the Livret A: A Means-Tested Higher Rate, Explained

France’s Livret d’épargne populaire is often described as "the Livret A, only better". The description misleads: the LEP…