Wealth Valuation: Why the Moment of Measurement Matters

Wealth is not a stock — it is an estimate conditional on the cycle, the level of rates and market liquidity. The same assets can swing by 15 to 30% over a complete rate cycle without any change in their intrinsic quality.

Wealth is not a stock — it is an estimate, conditional on the cycle, the level of rates and market liquidity at the moment of measurement.

TL;DR

The same asset carries different prices across a cycle: a complete rate move can shift a household's wealth by 15 to 30% while the assets themselves never change.

- Between two transactions a property has no observable price: estimates for the same home routinely diverge by 10 to 20% (Conseil supérieur du notariat, 2023) before any market move, and the amount actually received after fees and taxes can run 15 to 25% below the book figure.

- Rates act as the amplifier: French borrowing capacity rose more than 45% as mortgage rates fell from roughly 5% to 1.5% (2008-2021), then dropped close to 25% as they passed 4% in 2022, with transactions down 22% (Banque de France; Observatoire Crédit Logement, Q4 2024).

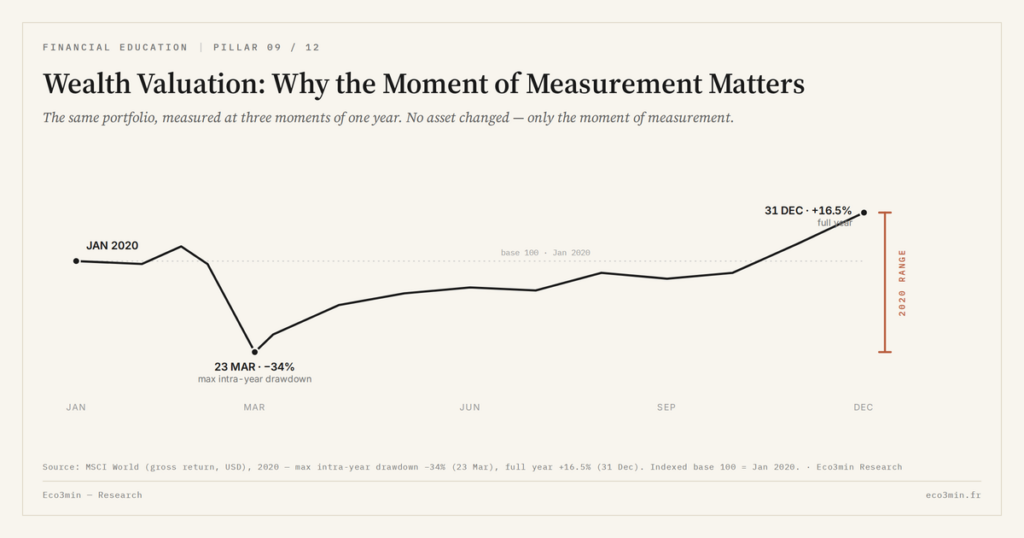

- Listed prices give an impression of constant motion, yet only the liquidation value moves: an MSCI World ETF worth €100,000 in January 2020 was around €66,000 in March and €115,000 by December (MSCI); BlackRock's Investor Pulse 2024 found that March-2020 sellers underperformed holders over the following year.

A residential property valued at €400,000 at the cycle peak can sell for €320,000 eighteen months later without a single brick changing. The asset has not moved. The conditions under which the asset is priced have. Treating a point-in-time estimate as a measure of wealth solidity therefore confuses a photograph with a trajectory. The mistake is not exotic: it sits at the root of most household balance-sheet illusions during turning points. Listed financial assets exhibit the same property with greater visible volatility, but the conditional nature of the figure is the same. The value of a wealth portfolio is never a fact. It is a price the market is willing to pay under specific conditions, and those conditions are themselves part of the measurement. Companion analysis: The decomposition of our set of decision simulators.

Real estate: a latent value, not a market price

Unlike a listed share, a residential property has no observable price between two transactions. Whatever figure appears on a balance sheet is an estimate produced by a notary, an agent or an algorithm. Estimates for the same property routinely diverge by 10 to 20% according to a 2023 study by the Conseil supérieur du notariat — a dispersion that exists before any market movement is added on top.

This produces a systematic anchoring effect during downturns. Owners tend to update slowly, holding onto the most recent peak figure they have seen. Between 2022 and 2024, French prices fell by 5 to 15% depending on the segment according to the Notaires-INSEE indices (Q4 2024). A property valued by its owner at €350,000 based on 2021 comparables typically corresponded to a transactable value between €300,000 and €330,000 — a 10 to 15% gap rarely incorporated into routine balance-sheet thinking, and the gap that explains why so many sellers spend several quarters at an asking price the market no longer recognizes.

Financial assets: transparency and the illusion of constant movement

Listed assets display a real-time price. The transparency creates the opposite bias of real estate: daily volatility gives the impression that wealth itself is in constant motion, when only the liquidation value at a given instant has moved. The distinction looks technical but is decisive.

An MSCI World ETF portfolio worth €100,000 in January 2020 was worth around €66,000 in March 2020 and €115,000 by December 2020 (MSCI). The investor’s wealth genuinely changed only if a sale occurred in March. For an investor who held, the March figure was a hypothetical liquidation price, not a realized loss. Confusing the two is the most common path to selling at the bottom — a behavioral mistake that the BlackRock Investor Pulse 2024 documented across European retail investors, finding that those who sold during the March 2020 drawdown underperformed those who held by a wide margin over the subsequent year. The visible figure was a paper move. The decision based on it produced a permanent loss.

- Anchoring real estate value on the purchase price or the last cyclical peak without incorporating recent corrections — the gap typically reaches 10 to 20% during downturns.

- Treating the instantaneous quote of a listed portfolio as a stable figure, when it captures only the price the market would pay at that instant.

Interest rates: the silent amplifier behind every valuation

The level of interest rates acts as a valuation amplifier across asset classes, and the channel is the same in each case: rates set the rate at which future cash flows or future housing services are discounted. In real estate, the decline in mortgage rates from roughly 5% to 1.5% between 2008 and 2021 raised average French borrowing capacity by more than 45% at unchanged income (Banque de France, 2024). The same monthly payment financed a much larger asset, and prices followed.

The reverse mechanism started in 2022. Rates moved from 1.5% to over 4%, borrowing capacity dropped by close to 25%, transactions fell 22% and prices corrected accordingly (Observatoire Crédit Logement, Q4 2024). The property had not changed. The rate had, and the price the market was willing to pay shifted with it.

The same logic applies to financial assets through the discount-rate channel. The theoretical value of an equity is the sum of its discounted future cash flows; when the discount rate rises, the present value mechanically falls even if earnings are unchanged. The S&P 500 lost 19% in 2022 (S&P Global) not because companies earned less, but because the rate at which those earnings were valued rose. For a wealth balance sheet, this means valuation can swing by 15 to 30% over a complete rate cycle with no change in the underlying quality of the assets. The cycle does the work — the assets are just along for the ride.

What this conditionality implies for reading wealth

If value is conditional, the figure that anchors a wealth decision is more informatively read as a range than as a single price. Treating it as a point hides the conditionality; treating it as a range integrates it. A residential property estimated at €400,000 in a cycle peak more accurately corresponds to a range that incorporates a 10 to 15% potential correction — a representation closer to what the wealth balance sheet actually contains than a single headline figure.

The gap between book value and liquidation value reinforces the point. The amount actually received after fees and taxes can be 15 to 25% below the estimated value for a residential property and 1 to 5% below for listed assets. The difference is structural: it is the gap between what a balance sheet displays and what is genuinely accessible. The reading of return logics that shift with the cycle rests on this distinction.

The most stable measurement is the trajectory rather than the point. Net wealth — revalued assets minus liabilities — tracked over five to ten years carries far more information than any single snapshot. The trajectory integrates market cycles, debt amortization and saving flows, and it is what separates wealth growing structurally from wealth inflated by a favorable cycle. The effect of this distinction also depends on where the holder sits in the life cycle, since a wealth structure that looks resilient at 35 can look fragile at 65 without a single asset changing.

Wealth value is a conditional estimate, not a fact. Treating it as fixed sets aside three variables — the cycle, the level of rates, market liquidity — that can shift the real balance sheet by 15 to 30% over a few quarters, without any change in the assets themselves.

Wealth recorded at €500,000 is not wealth of €500,000: it is wealth whose liquidation value most likely sits between €420,000 and €520,000 depending on the state of the cycle. The range carries more information than the central figure, and the gap with the central figure is itself a measure of how much of the wealth depends on the regime persisting. These considerations sit inside the broader frame of everyday financial trade-offs that commit wealth over the long term.

- Between two transactions, real estate value is an estimate — dispersion between methods routinely reaches 10 to 20% on the same property.

- Interest rates act as a valuation amplifier across asset classes: a complete rate cycle can shift wealth value by 15 to 30% with no change in the underlying assets.

- The trajectory of net wealth over five to ten years carries more information than any snapshot — only the trajectory distinguishes structural growth from cycle-driven inflation.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Series I and EE Savings Bonds: Locked Formulas in a Moving Rate World

US savings bonds lock a rate formula at the moment you buy them, for the life of the…

Where the Livret A’s Money Goes: The Caisse des Dépôts Circuit and Social-Housing Finance

The savings held on Livret A accounts do not sit idle. A regulation-set share is centralised at the…

France’s LEP vs the Livret A: A Means-Tested Higher Rate, Explained

France’s Livret d’épargne populaire is often described as "the Livret A, only better". The description misleads: the LEP…