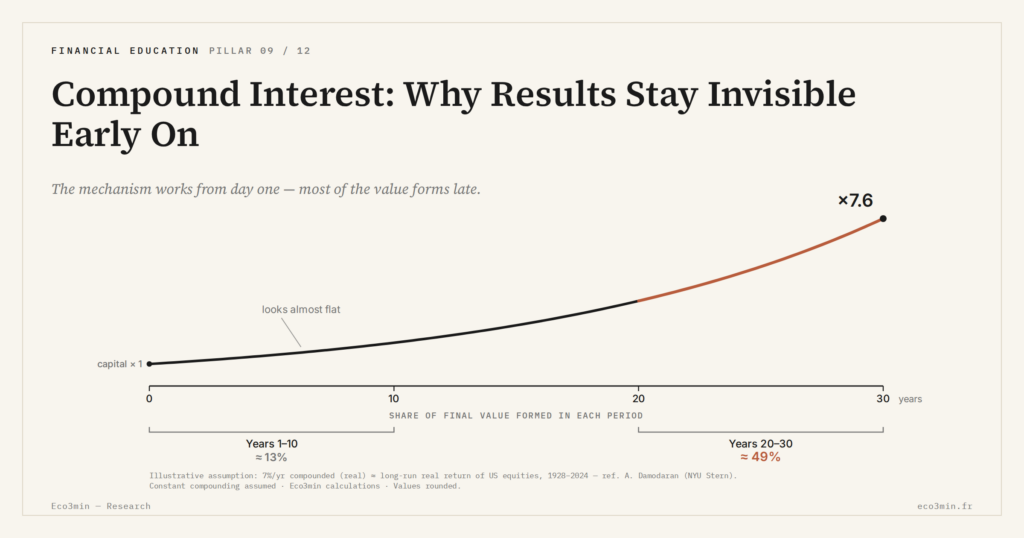

Compound Interest: Why Results Stay Invisible Early On

Compound interest produces real effects from the start, but the bulk of cumulative value concentrates after non-linear thresholds are crossed. The initial invisibility is a reading lag, not an inefficiency.

Explanation of the temporal lags inherent to compound interest and the reasons why its effects appear late.

TL;DR

Compound interest concentrates most of its value late: in many trajectories more than half the cumulative gain forms over the final third of the horizon, leaving early years near-flat.

- Growth follows implicit thresholds rather than a regular progression: until accumulated capital crosses a certain volume, successive increments stay small in absolute terms.

- The share of final value generated after a given horizon is the indicator that reframes early invisibility as an expected feature, not a sign of failure.

- Compound interest produces real effects from the start, but they remain imperceptible for a long time.

- The bulk of cumulative value concentrates after non-linear thresholds are crossed.

- The initial invisibility reflects a reading lag, not economic inefficiency.

The compound interest mechanism rests on a discreet but decisive logic: future growth depends entirely on the base accumulated so far. As long as this base remains limited, the cumulative effect remains mathematically real but economically barely perceptible. This initial invisibility is not an anomaly, but a structural lag between how the mechanism operates and how its results are observed. More context: our deep dive into how households weigh financial decisions through the cycle.

In the early phases, accumulation progresses without apparent break. Variations exist, but they remain absorbed by a base still too narrow to produce a visible differential. It is precisely this silent phase that fuels the impression of short-term inefficiency.

A non-linear mechanism masked by a linear reading

Compound interest does not develop along a regular progression. Its dynamic rests on implicit thresholds: as long as the accumulated capital does not exceed a certain volume, successive increments remain small in absolute value. Only after these thresholds are crossed does growth become perceptible.

Part of the dominant consensus nevertheless continues to reason in terms of periodic returns, as if each period contributed equivalently to the final result. This reading misses the fact that the order of financial decisions often matters more than their nature, once one reasons over a long horizon. This view implicitly assumes that the early years carry the same economic weight as the later ones. Yet in a compounding dynamic, it is the late periods that concentrate most of the cumulative value creation.

This divergence in reading explains why long trajectories first appear disappointing, before becoming suddenly visible. The mechanism works from the start, but its effects remain drowned in a base still too small.

Why the early periods weigh less than one might think

From a strictly arithmetic standpoint, the early years play a preparatory role. They build the surface on which future interest will apply. Their direct contribution to the final result is therefore mechanically limited.

Aggregate projections tend to mask this reality by presenting a final outcome without making explicit the temporal distribution of growth. A detailed visualisation of the trajectory shows on the contrary that, in many scenarios, more than half of the cumulative value is generated over the last third of the horizon considered.

This is precisely what a compound interest calculator materialises when used as a trajectory tool rather than a simple final-figure generator. The point is not the amount obtained, but the way it is built over time.

Why this invisibility is more problematic today

Since the normalisation of interest rates and the return of more persistent volatility, short-term comparisons have become more frequent. Gaps between different trajectories appear more rapidly, but the initial phases remain just as hard to read.

In this context, analytical impatience tends to intensify: trajectories still in their build-up phase are judged against immediate results. This gap between the temporality of the mechanism and the temporality of evaluation reinforces the impression that compound interest “does not work” at the start.

What readers are really trying to understand

Behind the question of invisible results lies a more fundamental query: how to interpret a trajectory that progresses without a clear signal over a long period. The issue is not to compare returns, but to understand at what point a cumulative mechanism becomes economically legible.

Put differently, the question is less about the efficiency of the mechanism than about the lead time required for its effects to cross the perception threshold.

Variables that could alter this reading

This analysis rests on the assumption of continuous and stable compounding. Prolonged interruptions, extreme volatility or shifts in monetary regime can move the thresholds at which effects become visible. Likewise, durably unstable inflation blurs the nominal reading of the trajectory and delays the perception of real enrichment.

These elements do not call the mechanism itself into question, but alter the speed at which it becomes observable.

Equating the absence of visible short-term results with an inefficiency of the mechanism. This reading is misleading because it ignores the non-linear thresholds inherent to compound interest.

Useful indicators to objectivise the delayed effect

A relevant indicator is to measure the share of final value generated after a given time horizon. When most of the growth concentrates over late periods, the initial invisibility becomes an expected feature, not a sign of failure.

This approach connects to the educational frameworks developed on the pillar page Financial Education, which aim to correct the reading biases linked to lags, cumulative effects and temporal asymmetries.

This is not the most commented scenario, but this silent phase shapes the entire later trajectory. As long as the analysis remains focused on the short term, the compound interest mechanism will continue to be perceived as disappointing before being understood. Keeping the frame that short is not a neutral choice: it is the observable form of the present bias that discounts distant payoffs.

Last updated — 28 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

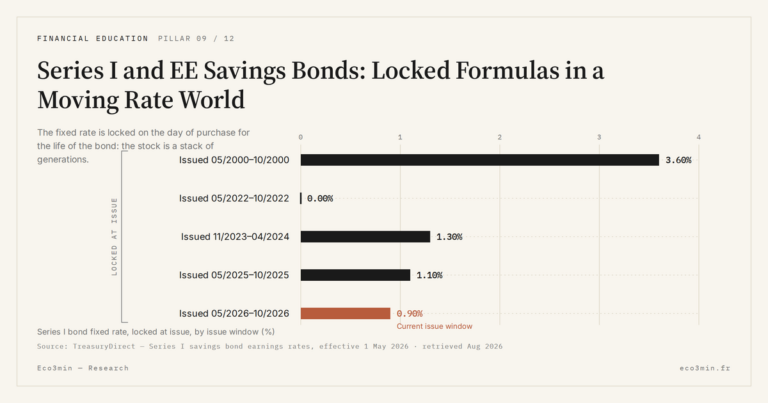

Full pillar →Series I and EE Savings Bonds: Locked Formulas in a Moving Rate World

US savings bonds lock a rate formula at the moment you buy them, for the life of the…

Where the Livret A’s Money Goes: The Caisse des Dépôts Circuit and Social-Housing Finance

The savings held on Livret A accounts do not sit idle. A regulation-set share is centralised at the…

France’s LEP vs the Livret A: A Means-Tested Higher Rate, Explained

France’s Livret d’épargne populaire is often described as "the Livret A, only better". The description misleads: the LEP…