The Limits of Regulating Financial AI

Regulation can frame financial AI without eliminating fragilities tied to system speed and complexity. Institutional norms set boundaries that cannot capture every emergent dynamic of automated systems.

Regulation can frame financial AI without eliminating fragilities tied to system speed and complexity.

TL;DR

Financial AI can stay compliant on paper while its real dynamics escape supervision: reaction times now run in milliseconds against quarterly oversight, turning formal compliance into an illusion of mastery.

- Sector estimates put advanced algorithmic components in more than 60% of volumes on certain liquid markets in 2025, a share growing faster than human supervisory capacity.

- Regulation reaches data governance, legal liability and decision traceability, yet emergent cross-model effects (synchronization, weak-signal amplification, rapid error propagation) stem from no identifiable fault and escape classic sanction tools.

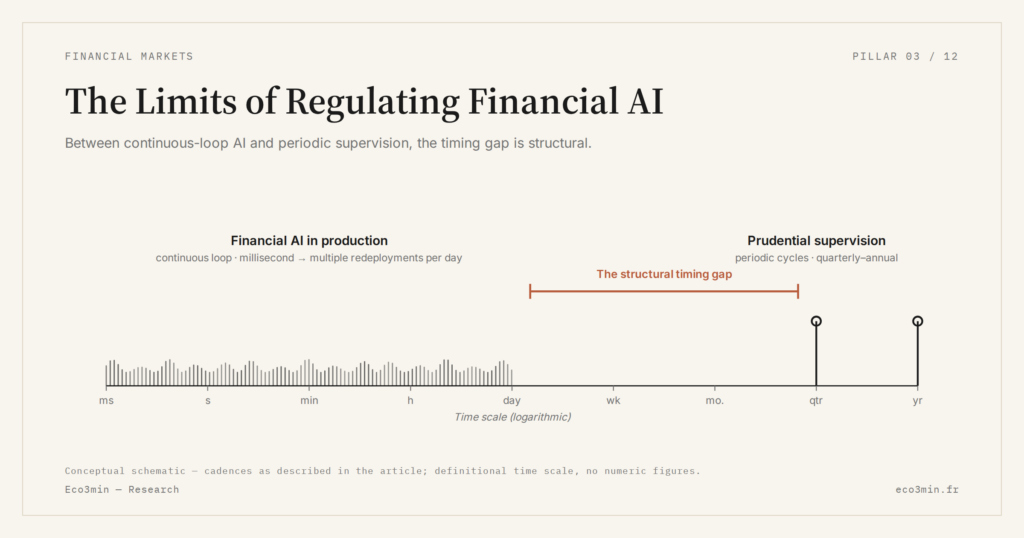

- Since late 2025, generative models embedded in trading, scoring and risk functions pushed reaction times to milliseconds while supervisory cycles stay quarterly or annual.

The rise of financial AI poses an unprecedented challenge to regulators. Institutional frameworks evolve more slowly than the technologies they seek to govern. This asymmetry limits regulatory effectiveness against emerging risks. An excessive expectation consists in believing that norms can neutralize complexity. Understanding these limits helps better situate the actual role of regulation.

A Regulatory Capacity Structurally Behind the Systems

One fact stands out: most regulatory frameworks applicable to financial AI rest on texts designed before the widespread adoption of machine learning models. In Europe, dominant prudential frameworks were conceived for deterministic systems, auditable ex ante. Financial AI, however, operates on adaptive logics, often opaque, whose behaviors emerge over time.

This mismatch creates an operational gap. Compliance obligations primarily target declared processes, not the actual dynamics of models in production. In practice, a system can remain compliant on paper while generating unanticipated systemic effects. This grey zone is what regulation struggles to capture.

This general framework is analyzed more broadly in the reference article on the AI transformation of finance and its structural risks, which lays out the global mechanisms without entering into these specific operational limits.

What Norms Cover… and What They Cannot Capture

Regulation acts effectively along three dimensions: data governance, legal liability and minimal traceability of decisions. These levers reduce certain individual risks, particularly regarding discrimination or legal compliance. They do not, however, address the central question of interaction between systems.

When several models optimized on similar objectives interact, collective behaviors emerge. These emergent effects — synchronization, amplification of weak signals, rapid error propagation — do not stem from an identifiable individual fault. They therefore escape classic sanction or correction tools.

This difficulty also stems from the complexity of governing automated systems, where formal compliance no longer guarantees effective control of production dynamics.

Part of the institutional consensus assumes that strengthening transparency obligations will suffice to contain these risks. This reading rests on the hypothesis that observability mechanically improves control. Yet in complex systems, seeing more does not necessarily mean understanding better.

Why This Limit Becomes More Visible Now

Since late 2025, the rise of generative models integrated into trading, scoring and risk management functions has accelerated market adjustment speed. Reaction times are now measured in milliseconds on certain segments, while supervisory cycles remain quarterly or even annual.

This temporal differential increases the probability of rapid events that are difficult to attribute. Authorities have richer information, but often after the fact. This is not an isolated regulatory failure, but a structural constraint tied to the very pace of automated systems.

What Readers Are Really Asking Behind the Regulation Question

The real question is not whether regulation exists, but whether it is sufficient to prevent collective derailment. Behind this question lies a simple concern: that systems considered well-framed nonetheless produce shocks that are difficult to anticipate, precisely because they comply with established rules.

Key Variables and Signals to Monitor

To assess the actual reach of regulation, certain indicators are more informative than the texts themselves. Among them: the concentration rate of financial AI tool providers, the correlation of automated decisions during stress periods, or the frequency of model adjustments in production.

For order of magnitude, sector estimates suggest that in 2025, more than 60% of volumes on certain liquid markets incorporate an advanced algorithmic component. This proportion is growing faster than human supervisory capacity, which constitutes a structural KPI to monitor.

Equating regulation with effective control. Formal compliance reduces certain legal risks but does not guarantee mastery of the collective dynamics generated by AI.

What Could Invalidate This Reading

One counter-argument deserves attention: rapid advances in continuous auditing or automated supervision could reduce this gap. If control tools evolve at the same pace as the systems they monitor, the current regulatory frontier could shift. This scenario, however, presupposes institutional and technological investment that remains uncertain.

Conversely, excessive regulatory tightening could slow innovation without eliminating systemic risks, by pushing certain practices into less transparent zones. The trajectory will therefore depend as much on political choices as on technical constraints.

A Structural Limit More Than a Regulatory Failure

Financial AI regulation cannot be assessed solely against its normative ambition. Its main limit lies in the gap between the adaptive complexity of systems and the static logic of rules. This is not the central scenario today, but this asymmetry is becoming an increasingly visible source of fragility.

The risk is not that regulation is absent, but that it creates an illusion of mastery. This possibility remains poorly integrated into mainstream readings, which makes it all the more strategic to monitor.

- Regulation frames processes but struggles to capture the emergent effects of financial AI systems.

- The speed gap between supervision and automation constitutes a structural constraint.

- The central question is not the existence of norms, but their ability to keep pace with adaptive dynamics.

To place these limits within a broader reading of financial innovation, the general analytical framework is developed on the dedicated pillar page on financial innovation, which structures long-term transformations without focusing on a single technological lever.

Last updated — 16 June 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…