Inventory Swings and the Business Cycle: How Stockbuilding Amplifies GDP Volatility

Inventory variations can account for the bulk of quarterly GDP changes while saying little about the underlying trend in final demand. The bullwhip effect propagates these adjustments along the supply chain, amplifying business cycle fluctuations beyond what real demand would justify.

A single line in the national accounts can swing the quarterly GDP print while saying almost nothing about the underlying economy. That line is the change in private inventories. When firms misjudge demand, even by a small margin, stocks pile up and trigger involuntary production cuts that go well beyond what real spending would justify. The bullwhip effect then propagates the correction up the supply chain. Read carelessly, an inventory-driven GDP quarter looks like a turning point in final demand. It rarely is.

Inventory variations amplify business cycle phases by triggering involuntary production adjustments that propagate along the supply chain.

TL;DR

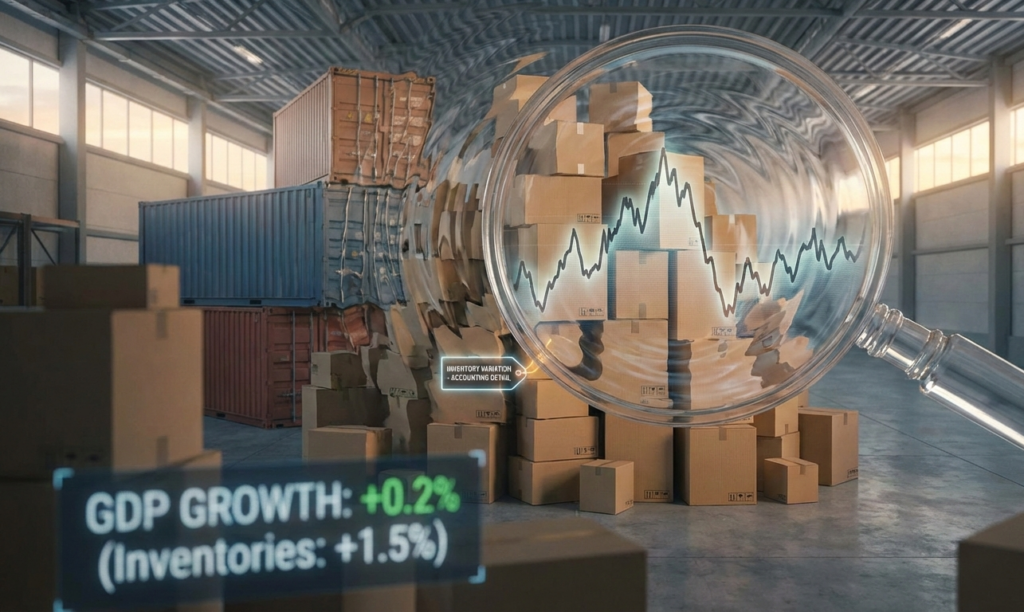

A single national-accounts line, the change in private inventories, added 0.4 point to US GDP in Q3 2025 then subtracted 0.3 the next quarter, a 0.7-point swing unrelated to final demand.

- The bullwhip effect amplifies the move up the chain (a 5% order cut at the retailer becomes 10% at the wholesaler and 15% at the producer); the Banque de France (September 2025) estimated this propagation deepened euro-area manufacturing's contraction by 1.5 to 2 points beyond the actual demand fall.

- After two years of destocking, European industry is expected to restock gradually in 2026, at a pace tied to how clearly firms can read end demand through monthly data whose revisions often arrive after the operational decision is made.

Markets often react to a GDP release without isolating this single line, even though stockbuilding can account for the bulk of the quarterly swing in either direction. Treating the headline figure as a verdict on demand confuses an accounting entry with the cyclical signal one wants to extract.

Involuntary accumulation, brutal correction

The sequence is mechanical. In expansion, firms build stocks in anticipation of growing demand. If demand decelerates faster than expected, inventories accumulate involuntarily. The Bureau of Economic Analysis reported that in Q3 2025 the change in private inventories contributed +0.4 percentage point to US GDP growth, before subtracting −0.3 point in Q4. A 0.7-point swing in two quarters, unrelated to any shift in final demand and its trajectory through the cycle.

The reversal is brutal because order cancellations propagate one stage at a time. Once excess stocks are registered, firms cut orders to suppliers, and industrial production contracts well beyond what the actual demand shortfall would warrant. The structural functioning of the real business cycle integrates this short-term amplifier as distinct from the slower dynamics of investment and productivity.

The bullwhip effect along supply chains

The amplification does not stay inside the individual firm. It travels up the chain, with each upstream link reading the perceived variation more aggressively than the one below. A 5% order cut at the retailer becomes a 10% cut at the wholesaler and a 15% cut at the producer. The Banque de France, in a September 2025 conjunctural note, estimated that this propagation deepened the contraction of euro-area manufacturing output by 1.5 to 2 percentage points beyond what the actual fall in final demand would have produced on its own.

Current estimates lean toward a gradual restocking in 2026, after two years of destocking across European industry. Its speed will depend on the visibility firms have on end demand. That visibility remains constrained by the distortions of monthly data, whose revisions often arrive after the operational decision has already been taken.

- Inventory swings can account for the bulk of a quarterly GDP variation without reflecting the real dynamics of demand.

- The bullwhip effect propagates and amplifies inventory adjustments along supply chains, deepening cyclical fluctuations.

- Isolating the contribution of inventories is essential to distinguish a technical adjustment from a genuine cyclical turn.

This reading framework could lose part of its relevance if real-time inventory management tools, driven by AI and instant demand data, substantially reduced anticipation errors. Several large European and US distributors are investing in such technologies, but adoption remains uneven. The aggregate dynamics of the cycle continue to reflect a largely procyclical stockbuilding behaviour that amplifies both upswings and downswings. Related Q&A: the Kitchin inventory cycle.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…