Why Economic Decisions Produce Lagged, Counter-Intuitive Effects

Economic decisions never produce immediate effects. Their transmission runs through multiple channels — bond markets, bank refinancing, lending standards — that filter and delay the initial signal in often counter-intuitive ways.

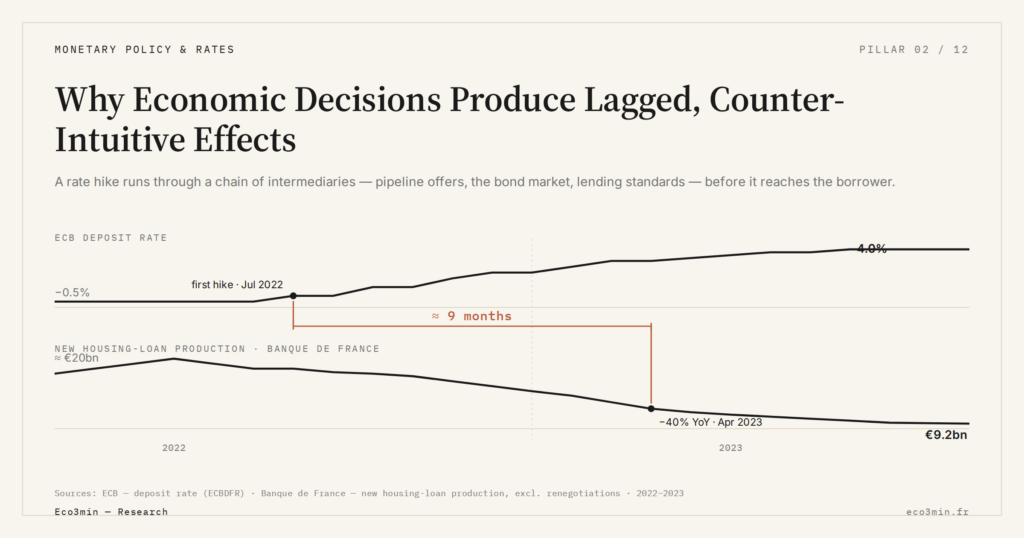

Mortgage lending takes several quarters to react to policy rate hikes. This lag reveals a transmission mechanism that is frequently misread.

TL;DR

A six- to twelve-month lag separates a policy-rate hike from the mortgage-volume contraction it triggers, while bank lending criteria do as much of the tightening as the rate itself.

- The ECB lifted its deposit rate from -0.5% to 4% between July 2022 and September 2023, yet new housing-loan flows only began contracting meaningfully from the second quarter of 2023, roughly nine months later.

- Market rates anticipate central-bank moves: the French 10-year OAT rose from about 0.2% in January 2022 to about 2.8% by October, while the ECB deposit rate had reached only 0.75%, so credit costs climbed before policy formally turned restrictive.

- Lending standards carry part of the tightening: since 2022 France's HCSF caps the debt-service-to-income ratio at 35% and maturities at 25 years, excluding files even when the headline rate is not the binding constraint.

- The average household mortgage rate reached about 4.1% at end-2023 against about 1.1% in early 2022 (Banque de France), while loan volumes fell roughly 40% over the period (broker data), a drop sharper than the rate rise alone explains.

A monetary tightening does not immediately curb credit issuance

When a central bank lifts its policy rates, the impact on the volume of mortgages granted does not show up in the following weeks. In the euro area, between July 2022 and September 2023, the ECB raised its deposit rate from -0.5% to 4%. Yet the flow of new housing loans only began to contract significantly from the second quarter of 2023, nearly nine months after the first hike.

This lag stems from several structural factors. Loan offers issued before the hike remain valid for several weeks. Files already underway continue through the pipeline. Banks, committed to quarterly commercial targets, temporarily maintain their conditions. The transmission logic of monetary policy decisions thus runs through a chain of intermediaries that absorb and delay the initial signal.

The role of market rates in the transmission chain

The policy rate is not directly applied to borrowers. Between the central bank decision and the rate offered to clients sits the bond market. Banks refinance themselves at long maturities, indexed to the 10-year French OAT or Euribor. These market rates often anticipate monetary decisions before they are formally announced.

In 2022, the French 10-year OAT moved from ≈0.2% in January to ≈2.8% in October, while the ECB had only raised its deposit rate to 0.75% by that date. The bond market had therefore priced in most of the restrictive cycle ahead of its full execution. Paradoxically, this means the cost of mortgage credit started rising before monetary policy officially turned restrictive. Companion analysis: Our account of the transmission of rate cycles to profitability.

What matters more than it looks

The decisive variable is not the policy rate itself, but the speed at which market expectations adjust. An expected hike produces less effect than a surprise hike. Central bank communication — forward guidance, inflation projections — acts on long rates before any concrete action. This mechanism explains why some hiking cycles seem to produce rapid effects while others take quarters to materialise.

The bank lending standards filter

Beyond the cost of refinancing, banks have an additional lever: their lending criteria. In France, the Haut Conseil de stabilité financière (HCSF) has imposed since 2022 a maximum debt-service-to-income ratio of 35% and a maximum maturity of 25 years. As rates rise, these constraints mechanically exclude a growing share of files, even when the headline rate is not the binding factor.

According to Banque de France data, the average rate on mortgages to households reached ≈4.1% at end-2023, against ≈1.1% at the start of 2022. But the drop in the number of loans granted (-40% in volume over the same period, according to brokers) also reflects a qualitative tightening: higher down-payment requirements, more selective screening of profiles.

Attributing the collapse in mortgage credit to the rate level alone ignores the role of lending standards. A household can theoretically borrow at 4% but be turned down for breaching the debt-service-to-income cap — a phenomenon invisible in average-rate statistics.

Why this lag destabilises macro projections

The gap between the monetary decision and its effect on mortgage credit complicates the assessment of ECB policy. When the institution observes a credit contraction at T+3, it does not know whether this stems from its own decision at T or from an autonomous tightening by banks. This uncertainty explains why central banks often hold rates higher for longer than necessary: they wait to see the full effect of measures already taken.

The dominant consensus generally anticipates a mechanical and rapid effect. The observed reality, however, shows a propagation in steps, with sudden accelerations when several constraints stack. In France, the tipping point came in spring 2023, when the rise in refinancing rates coincided with the tightening of HCSF criteria and the end of pre-negotiated commercial offers.

What could invalidate this reading

This analytical frame assumes banks adjust their conditions gradually. Several elements could alter that dynamic. A market-share war between banking institutions would speed up the pass-through of rate cuts (if and when they come). A regulatory intervention — loosening of HCSF criteria, public guarantee — would bypass the normal transmission mechanism. A bank liquidity crisis would produce the opposite effect: a brutal credit freeze independent of the rate level.

Markets mainly watch nominal rates and transaction volumes. But the variable that conditions the actual trajectory remains the spread between refinancing cost and bank margin, rarely commented upon in mainstream analysis.

The underlying concern

What many readers really seek to understand here has less to do with the technical mechanism than with one simple question: when will mortgage credit become accessible again? The answer depends less on the absolute rate level than on the stabilisation of expectations. As long as the bond market prices in uncertainty about the ECB’s trajectory, banks maintain precautionary margins that delay any easing.

Indicator to monitor

The spread between the 10-year OAT and the average mortgage rate is a leading indicator of bank margin. When this spread tightens, banks pass through market moves more quickly. Its value typically oscillates between 100 and 150 basis points. A widening beyond 200 bp signals an autonomous tightening of lending standards, independent of monetary policy.

Monthly housing-loan production, published by the Banque de France with a six-week lag, remains the reference KPI. But its interpretation requires cross-reading volume, average rate and rejection rate — the latter only available indirectly through broker surveys.

- Mortgage credit reacts to rate hikes with a six- to twelve-month lag, the time it takes for outstanding offers to drain and for banks to readjust their pricing grids.

- Market rates (10-year OAT, Euribor) anticipate ECB decisions, which is why the cost of credit can rise before any official hike.

- Lending standards (debt-service ratio, down payment) play a role at least as important as the headline rate level in the contraction of loan volumes.

To explore the broader transmission mechanisms between monetary policy and the real economy, see the analysis of the lagged effects of economic decisions. A wider view of the interactions between financial markets and asset allocation is available on the stocks and ETFs page.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…